- Page 2 and 3:

South African Health Review 2007 LI

- Page 4:

Foreword The 12th edition of South

- Page 7 and 8:

12 Traditional and Complementary Me

- Page 9 and 10:

Other Funders for the Health System

- Page 11 and 12:

This response raises a number of qu

- Page 13 and 14:

ucts are currently sold without reg

- Page 15 and 16:

The authors conclude that mandatory

- Page 17 and 18:

servicing and inappropriate hospita

- Page 19 and 20:

systems is also critical; worrying

- Page 22 and 23:

Authors: Laetitia Rispel i Geoffrey

- Page 24 and 25:

Stewardship: Protecting the Public

- Page 26 and 27:

Stewardship: Protecting the Public

- Page 28 and 29:

Stewardship: Protecting the Public

- Page 30 and 31:

Stewardship: Protecting the Public

- Page 32 and 33: Stewardship: Protecting the Public

- Page 34 and 35: Stewardship: Protecting the Public

- Page 36: Stewardship: Protecting the Public

- Page 39 and 40: Introduction The importance of the

- Page 41 and 42: diseases such as tuberculosis and t

- Page 43 and 44: 17 of 2002). This Act entirely repl

- Page 45 and 46: (d) and any other matter relating t

- Page 47 and 48: Year Act No. Title Objects 1997 90

- Page 49 and 50: References 1 Department of Health.

- Page 52: Purchasing of Health Care 33Pooling

- Page 55 and 56: Introduction This chapter presents

- Page 57 and 58: Medical schemes are the largest fin

- Page 59 and 60: per person dependent on the public

- Page 61 and 62: An increase in hospital expenditure

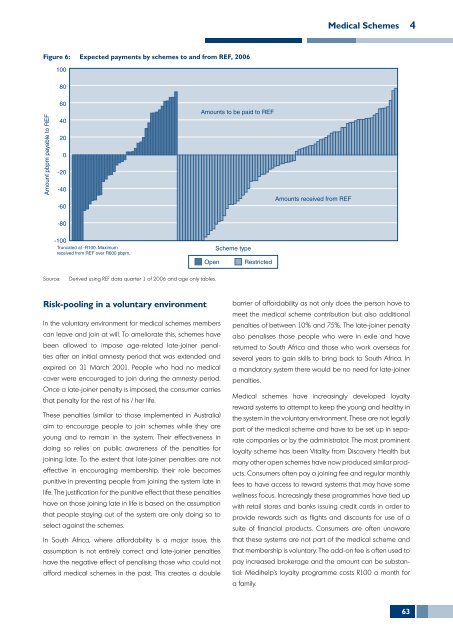

- Page 63 and 64: private pharmacy do so for self-tre

- Page 65 and 66: References 1 McIntyre D, Thiede M,

- Page 67 and 68: Policy and legislative framework In

- Page 69 and 70: Medical schemes and revenue collect

- Page 71 and 72: There is evidence that when faced w

- Page 73 and 74: are thus contributing factors to th

- Page 75 and 76: Figure 2: Historic membership of me

- Page 77 and 78: Solvency of the risk pools has beco

- Page 79 and 80: Figure 4: 100 Proportion of risk be

- Page 81: will retain that benefit for their

- Page 85 and 86: From a benefit design perspective t

- Page 87 and 88: and towards competition based on ef

- Page 89 and 90: 37 Du Preez L. Registrar wants cura

- Page 91 and 92: Introduction There has long been co

- Page 93 and 94: an element of cream-skimming which

- Page 95 and 96: Table 1: Distribution of health car

- Page 97 and 98: isk equalisation mechanism were imp

- Page 99 and 100: once the cost spiral in medical sch

- Page 101 and 102: Revenue collection: Collecting orga

- Page 103 and 104: Current debates A key area of ongoi

- Page 105 and 106: References 1 Gluckman H. The Provis

- Page 108 and 109: Authors: Patrick Matshidze i Lyn Ha

- Page 110 and 111: Health Information Systems in the P

- Page 112 and 113: Health Information Systems in the P

- Page 114 and 115: Health Information Systems in the P

- Page 116 and 117: Health Information Systems in the P

- Page 118 and 119: Health Information Systems in the P

- Page 120 and 121: Health Information Systems in the P

- Page 122 and 123: Authors: Shahieda Adams i Reno Mora

- Page 124 and 125: Health and Health Care in the Workp

- Page 126 and 127: Health and Health Care in the Workp

- Page 128 and 129: Health and Health Care in the Workp

- Page 130 and 131: Health and Health Care in the Workp

- Page 132 and 133:

Health and Health Care in the Workp

- Page 134 and 135:

Health and Health Care in the Workp

- Page 136 and 137:

Health and Health Care in the Workp

- Page 138 and 139:

Health and Health Care in the Workp

- Page 140 and 141:

Health and Health Care in the Workp

- Page 142 and 143:

Author: Bettina Taylor i 8 Rationin

- Page 144 and 145:

Rationing of Medicines and Health C

- Page 146 and 147:

Rationing of Medicines and Health C

- Page 148 and 149:

Rationing of Medicines and Health C

- Page 150 and 151:

Rationing of Medicines and Health C

- Page 152 and 153:

Rationing of Medicines and Health C

- Page 154 and 155:

Rationing of Medicines and Health C

- Page 156 and 157:

Rationing of Medicines and Health C

- Page 158 and 159:

Health Care Delivery 139

- Page 160 and 161:

Authors: Haroon Wadee i Farzana Kha

- Page 162 and 163:

Human Resources for Health 9 Table

- Page 164 and 165:

Human Resources for Health 9 Table

- Page 166 and 167:

Human Resources for Health 9 source

- Page 168 and 169:

Human Resources for Health 9 Refere

- Page 170 and 171:

Authors: Shadrack Shuping i Sipho K

- Page 172 and 173:

Public-Private Partnerships 10 Alth

- Page 174 and 175:

Public-Private Partnerships 10 Tabl

- Page 176 and 177:

Public-Private Partnerships 10 Conc

- Page 178 and 179:

Authors: Thulani Matsebula i Michae

- Page 180 and 181:

Private Hospitals 11 Table 1: Priva

- Page 182 and 183:

Private Hospitals 11 Table 3: Distr

- Page 184 and 185:

Private Hospitals 11 Human resource

- Page 186 and 187:

Private Hospitals 11 Figure 3: 16 T

- Page 188 and 189:

Private Hospitals 11 Figure 4: 2 50

- Page 190 and 191:

Private Hospitals 11 Monitoring qua

- Page 192 and 193:

Private Hospitals 11 Recommendation

- Page 194 and 195:

Authors: Nceba Gqaleni i Indres Moo

- Page 196 and 197:

Traditional and Complementary Medic

- Page 198 and 199:

Traditional and Complementary Medic

- Page 200 and 201:

Traditional and Complementary Medic

- Page 202 and 203:

Traditional and Complementary Medic

- Page 204 and 205:

Traditional and Complementary Medic

- Page 206 and 207:

Traditional and Complementary Medic

- Page 208 and 209:

Authors: Myles Mander i Lungile Ntu

- Page 210 and 211:

Economics of the Traditional Medici

- Page 212 and 213:

Economics of the Traditional Medici

- Page 214 and 215:

Economics of the Traditional Medici

- Page 216 and 217:

Economics of the Traditional Medici

- Page 218 and 219:

Economics of the Traditional Medici

- Page 220 and 221:

Authors: Marion Stevens i Edina Sin

- Page 222 and 223:

HIV and AIDS, STI and TB in the Pri

- Page 224 and 225:

HIV and AIDS, STI and TB in the Pri

- Page 226 and 227:

HIV and AIDS, STI and TB in the Pri

- Page 228 and 229:

HIV and AIDS, STI and TB in the Pri

- Page 230 and 231:

HIV and AIDS, STI and TB in the Pri

- Page 232 and 233:

Indicators 213

- Page 234 and 235:

Authors: Candy Day i Andy Gray ii 1

- Page 236 and 237:

Health and Related Indicators 15

- Page 238 and 239:

Health and Related Indicators 15

- Page 240 and 241:

Health and Related Indicators 15 Ta

- Page 242 and 243:

Health and Related Indicators 15 Ta

- Page 244 and 245:

Health and Related Indicators 15 Ta

- Page 246 and 247:

Health and Related Indicators 15 Ta

- Page 248 and 249:

Health and Related Indicators 15 Th

- Page 250 and 251:

Health and Related Indicators 15 Ta

- Page 252 and 253:

Health and Related Indicators 15 Ta

- Page 254 and 255:

Health and Related Indicators 15 Tu

- Page 256 and 257:

Health and Related Indicators 15 Fi

- Page 258 and 259:

Health and Related Indicators 15 He

- Page 260 and 261:

Health and Related Indicators 15 Ta

- Page 262 and 263:

Health and Related Indicators 15 tr

- Page 264 and 265:

Health and Related Indicators 15 Fi

- Page 266 and 267:

Health and Related Indicators 15 He

- Page 268 and 269:

Health and Related Indicators 15 Fi

- Page 270 and 271:

Health and Related Indicators 15 Ta

- Page 272 and 273:

Health and Related Indicators 15 Ta

- Page 274 and 275:

Health and Related Indicators 15 He

- Page 276 and 277:

Health and Related Indicators 15 He

- Page 278 and 279:

Health and Related Indicators 15 Ta

- Page 280 and 281:

Health and Related Indicators 15 Nu

- Page 282 and 283:

Health and Related Indicators 15 He

- Page 284 and 285:

Health and Related Indicators 15 19

- Page 286 and 287:

Health and Related Indicators 15 He

- Page 288 and 289:

Health and Related Indicators 15 Ta

- Page 290 and 291:

Health and Related Indicators 15 No

- Page 292 and 293:

Health and Related Indicators 15 Ta

- Page 294 and 295:

Health and Related Indicators 15 Be

- Page 296 and 297:

Health and Related Indicators 15 He

- Page 298 and 299:

Health and Related Indicators 15 Fi

- Page 300 and 301:

Health and Related Indicators 15 He

- Page 302 and 303:

Health and Related Indicators 15 De

- Page 304 and 305:

Health and Related Indicators 15 Ma

- Page 306 and 307:

Health and Related Indicators 15 Ea

- Page 308 and 309:

Health and Related Indicators 15 Fr

- Page 310 and 311:

Health and Related Indicators 15 Ga

- Page 312 and 313:

Health and Related Indicators 15 Kw

- Page 314 and 315:

Health and Related Indicators 15 He

- Page 316 and 317:

Health and Related Indicators 15 Li

- Page 318 and 319:

Health and Related Indicators 15 Mp

- Page 320 and 321:

Health and Related Indicators 15 No

- Page 322 and 323:

Health and Related Indicators 15 No

- Page 324 and 325:

Health and Related Indicators 15 We

- Page 326 and 327:

Health and Related Indicators 15

- Page 328 and 329:

Health and Related Indicators 15 Ta

- Page 330 and 331:

Health and Related Indicators 15 Ta

- Page 332 and 333:

Health and Related Indicators 15 He

- Page 334 and 335:

Health and Related Indicators 15 He

- Page 336 and 337:

Health and Related Indicators 15 Pu

- Page 338 and 339:

Health and Related Indicators 15 Ta

- Page 340 and 341:

Health and Related Indicators 15 Di

- Page 342 and 343:

Health and Related Indicators 15 He

- Page 344 and 345:

Health and Related Indicators 15 He

- Page 346 and 347:

Health and Related Indicators 15 In

- Page 348 and 349:

Health and Related Indicators 15 Ta

- Page 350 and 351:

Health and Related Indicators 15 In

- Page 352 and 353:

Health and Related Indicators 15 Ty

- Page 354 and 355:

Health and Related Indicators 15 Ty

- Page 356 and 357:

Health and Related Indicators 15 Ty

- Page 358 and 359:

Health and Related Indicators 15 Ch

- Page 360 and 361:

Health and Related Indicators 15 MD

- Page 362 and 363:

Health and Related Indicators 15 St

- Page 364 and 365:

Glossary AFA AIDS ALP AMA ANC ART A

- Page 366 and 367:

Glossary KZN LFS LIMS LP LPP MAR MC

- Page 368 and 369:

Glossary SAPC SARS SASIM SASSA SEP

- Page 370 and 371:

Index A Acts (Legislation and Bills

- Page 372 and 373:

Index N and O National Health Refer