Lecture 9 - Lehrstuhl für Controlling - Technische Universität München

Lecture 9 - Lehrstuhl für Controlling - Technische Universität München

Lecture 9 - Lehrstuhl für Controlling - Technische Universität München

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Technische</strong> <strong>Universität</strong> <strong>München</strong><br />

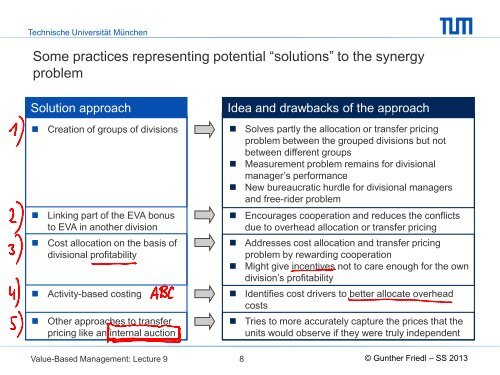

Some practices representing potential “solutions” to the synergy<br />

problem<br />

Solution approach<br />

• Creation of groups of divisions<br />

• Linking part of the EVA bonus<br />

to EVA in another division<br />

• Cost allocation on the basis of<br />

divisional profitability<br />

• Activity-based costing<br />

• Other approaches to transfer<br />

pricing like an internal auction<br />

Idea and drawbacks of the approach<br />

• Solves partly the allocation or transfer pricing<br />

problem between the grouped divisions but not<br />

between different groups<br />

• Measurement problem remains for divisional<br />

manager’s performance<br />

• New bureaucratic hurdle for divisional managers<br />

and free-rider problem<br />

• Encourages cooperation and reduces the conflicts<br />

due to overhead allocation or transfer pricing<br />

• Addresses cost allocation and transfer pricing<br />

problem by rewarding cooperation<br />

• Might give incentives not to care enough for the own<br />

division’s profitability<br />

• Identifies cost drivers to better allocate overhead<br />

costs<br />

• Tries to more accurately capture the prices that the<br />

units would observe if they were truly independent<br />

Value-Based Management: <strong>Lecture</strong> 9<br />

8<br />

© Gunther Friedl – SS 2013