Carbon 2009 Emission trading coming home - UNEP Finance Initiative

Carbon 2009 Emission trading coming home - UNEP Finance Initiative

Carbon 2009 Emission trading coming home - UNEP Finance Initiative

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>Carbon</strong> <strong>2009</strong><br />

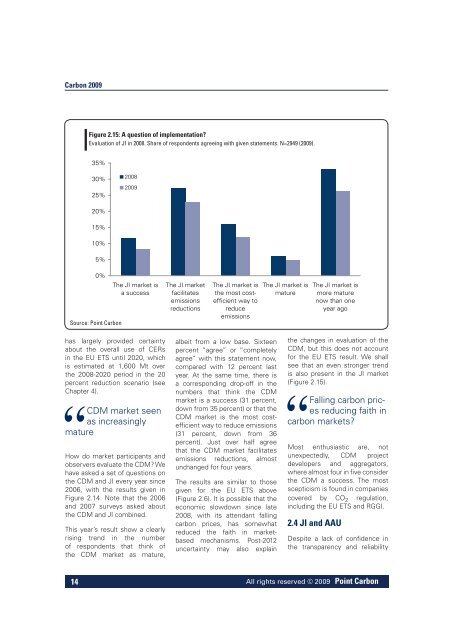

Figure 2.15: A question of implementation?<br />

Evaluation of JI in 2008. Share of respondents agreeing with given statements. N=2949 (<strong>2009</strong>).<br />

35%<br />

30%<br />

25%<br />

2008<br />

<strong>2009</strong><br />

20%<br />

15%<br />

10%<br />

5%<br />

0%<br />

Source: Point <strong>Carbon</strong><br />

The JI market is<br />

a success<br />

The JI market<br />

facilitates<br />

emissions<br />

reductions<br />

The JI market is<br />

the most costefficient<br />

way to<br />

reduce<br />

emissions<br />

The JI market is<br />

mature<br />

The JI market is<br />

more mature<br />

now than one<br />

year ago<br />

has largely provided certainty<br />

about the overall use of CERs<br />

in the EU ETS until 2020, which<br />

is estimated at 1,600 Mt over<br />

the 2008-2020 period in the 20<br />

percent reduction scenario (see<br />

Chapter 4).<br />

CDM market seen<br />

as increasingly<br />

mature<br />

How do market participants and<br />

observers evaluate the CDM? We<br />

have asked a set of questions on<br />

the CDM and JI every year since<br />

2006, with the results given in<br />

Figure 2.14. Note that the 2006<br />

and 2007 surveys asked about<br />

the CDM and JI combined.<br />

This year’s result show a clearly<br />

rising trend in the number<br />

of respondents that think of<br />

the CDM market as mature,<br />

albeit from a low base. Sixteen<br />

percent “agree” or “completely<br />

agree” with this statement now,<br />

compared with 12 percent last<br />

year. At the same time, there is<br />

a corresponding drop-off in the<br />

numbers that think the CDM<br />

market is a success (31 percent,<br />

down from 35 percent) or that the<br />

CDM market is the most costefficient<br />

way to reduce emissions<br />

(31 percent, down from 36<br />

percent). Just over half agree<br />

that the CDM market facilitates<br />

emissions reductions, almost<br />

unchanged for four years.<br />

The results are similar to those<br />

given for the EU ETS above<br />

(Figure 2.6). It is possible that the<br />

economic slowdown since late<br />

2008, with its attendant falling<br />

carbon prices, has somewhat<br />

reduced the faith in marketbased<br />

mechanisms. Post-2012<br />

uncertainty may also explain<br />

the changes in evaluation of the<br />

CDM, but this does not account<br />

for the EU ETS result. We shall<br />

see that an even stronger trend<br />

is also present in the JI market<br />

(Figure 2.15).<br />

Falling carbon prices<br />

reducing faith in<br />

carbon markets?<br />

Most enthusiastic are, not<br />

unexpectedly, CDM project<br />

developers and aggregators,<br />

where almost four in five consider<br />

the CDM a success. The most<br />

scepticism is found in companies<br />

covered by CO 2 regulation,<br />

including the EU ETS and RGGI.<br />

2.4 JI and AAU<br />

Despite a lack of confidence in<br />

the transparency and reliability<br />

14<br />

All rights reserved © <strong>2009</strong> Point <strong>Carbon</strong>