Stochastic Volatility and Seasonality in ... - Interconti, Limited

Stochastic Volatility and Seasonality in ... - Interconti, Limited

Stochastic Volatility and Seasonality in ... - Interconti, Limited

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

0.80<br />

0.70<br />

0.60<br />

Implied volatilities<br />

0.50<br />

0.40<br />

0.30<br />

0.20<br />

0.10<br />

0.00<br />

Jan-84 Jan-88 Jan-92 Jan-96 Jan-2000<br />

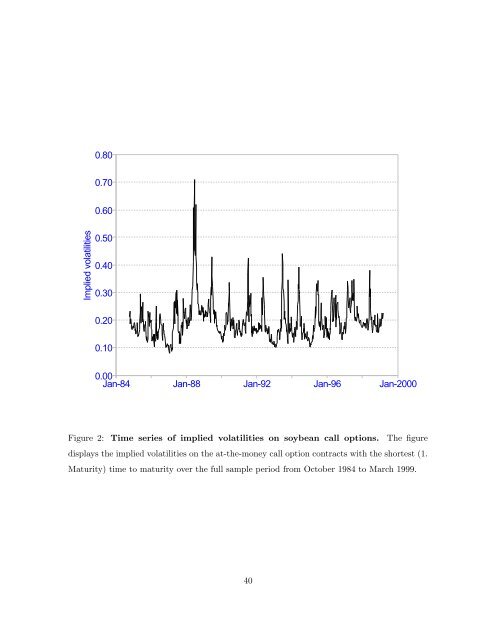

Figure 2: Time series of implied volatilities on soybean call options. The figure<br />

displays the implied volatilities on the at-the-money call option contracts with the shortest (1.<br />

Maturity) time to maturity over the full sample period from October 1984 to March 1999.<br />

40

![Definitions & Concepts... [PDF] - Cycles Research Institute](https://img.yumpu.com/26387731/1/190x245/definitions-concepts-pdf-cycles-research-institute.jpg?quality=85)