NZ Report / Proposal Template - State Services Commission

NZ Report / Proposal Template - State Services Commission

NZ Report / Proposal Template - State Services Commission

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

strict fixed price contract, financial risk is substantially borne by the provider (although<br />

provisions relating to contract variations can result in sharing of financial risk). In contrast,<br />

under a CWA as adopted by the Department, it is not until the project has been completed<br />

and the final costs accounted for, that the client has certainty over the total amount<br />

payable for the project.<br />

5.16 Although not accepted by the Department at the time of preparing the report that<br />

went to Cabinet in December 2005, the TOCs were at an advanced stage. The draft<br />

TOCs indicated that costs had increased to $381 million and $218 million for Spring Hill<br />

and Otago respectively.<br />

5.17 The December 05 report to Cabinet included a description of the factors leading to<br />

the cost increases compared to the Budget 05 estimates. In brief, the contributing factors<br />

were grouped under the headings of market influences, regulatory and consent changes<br />

and omissions from earlier estimates (items seen by the Department as not previously<br />

included rather than items inadvertently overlooked). While the increases and underlying<br />

causes are site-specific, in the case of escalation, there is considerable overlap between<br />

the two sites and this issue is considered first.<br />

5.18 From the Crown’s perspective, it has a keen interest in achieving project<br />

completion on time, within budget and to specification. In normal fixed price contracts,<br />

price is established up front as part of the tender process (although actual price outturn is<br />

often the subject of contract variations). The way in which CWA has been used by the<br />

Department means that there is no price information arising from the selection process.<br />

Development of the TOC (and related QRA and gain/pain share arrangements) is,<br />

therefore, of critical importance, particularly from a fiscal management perspective.<br />

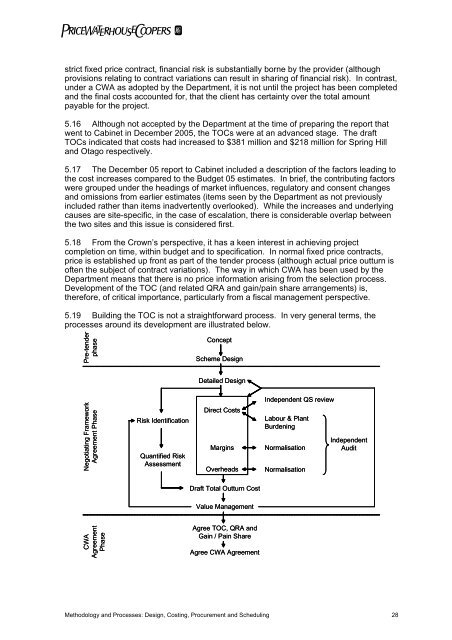

5.19 Building the TOC is not a straightforward process. In very general terms, the<br />

processes around its development are illustrated below.<br />

er<br />

Pre-tend<br />

phase<br />

Concept<br />

Scheme Design<br />

Detailed Design<br />

Negotiating Framework<br />

Agreement Phase<br />

Risk Identification<br />

Quantified Risk<br />

Assessment<br />

Direct Costs<br />

Margins<br />

Overheads<br />

Independent QS review<br />

Labour & Plant<br />

Burdening<br />

Independent<br />

Normalisation<br />

Audit<br />

Normalisation<br />

Draft Total Outturn Cost<br />

Value Management<br />

CWA<br />

Agreement<br />

Phase<br />

Agree TOC, QRA and<br />

Gain / Pain Share<br />

Agree CWA Agreement<br />

Methodology and Processes: Design, Costing, Procurement and Scheduling 28