CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

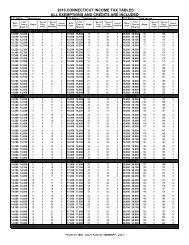

Sample Use <strong>Tax</strong> Table<br />

Total Purchases<br />

Total Purchases<br />

Subject to Use <strong>Tax</strong> Due at: Subject to Use <strong>Tax</strong> Due at:<br />

Use <strong>Tax</strong> 6% 6.35% 7% Use <strong>Tax</strong> 6% 6.35% 7%<br />

$25 $1.50 $1.59 ─<br />

50 3.00 3.18 ─<br />

75 4.50 4.76 ─<br />

100 6.00 6.35 ─<br />

150 9.00 9.53 ─<br />

200 12.00 12.70 ─<br />

250 15.00 15.88 ─<br />

300 18.00 19.05 ─<br />

350 21.00 22.23 ─<br />

400 24.00 25.40 ─<br />

450 27.00 28.58 ─<br />

500 30.00 31.75 ─<br />

550 33.00 34.93 ─<br />

600 36.00 38.10 ─<br />

650 39.00 41.28 ─<br />

700 42.00 44.45 ─<br />

750 45.00 47.63 ─<br />

800 48.00 50.80 ─<br />

850 51.00 53.98 ─<br />

900 54.00 57.15 ─<br />

1,000 60.00 63.50 ─<br />

1,100 66.00 69.85 77.00<br />

1,200 72.00 76.20 84.00<br />

1,300 78.00 82.55 91.00<br />

1,400 84.00 88.90 98.00<br />

1,500 90.00 95.25 105.00<br />

1,600 96.00 101.60 112.00<br />

1,700 102.00 107.95 119.00<br />

1,800 108.00 114.30 126.00<br />

1,900 114.00 120.65 133.00<br />

$2,000 $120.00 $127.00 $140.00<br />

2,100 126.00 133.35 147.00<br />

2,200 132.00 139.70 154.00<br />

2,300 138.00 146.05 161.00<br />

2,400 144.00 152.40 168.00<br />

2,500 150.00 158.75 175.00<br />

2,600 156.00 165.10 182.00<br />

2,700 162.00 171.45 189.00<br />

2,800 168.00 177.80 196.00<br />

2,900 174.00 184.15 203.00<br />

3,000 180.00 190.50 210.00<br />

3,100 186.00 196.85 217.00<br />

3,200 192.00 203.20 224.00<br />

3,300 198.00 209.55 231.00<br />

3,400 204.00 215.90 238.00<br />

3,500 210.00 222.25 245.00<br />

3,600 216.00 228.60 252.00<br />

3,700 222.00 234.95 259.00<br />

3,800 228.00 241.30 266.00<br />

3,900 234.00 247.65 273.00<br />

4,000 240.00 254.00 280.00<br />

4,100 246.00 260.35 287.00<br />

4,200 252.00 266.70 294.00<br />

4,300 258.00 273.05 301.00<br />

4,400 264.00 279.40 308.00<br />

4,500 270.00 285.75 315.00<br />

4,600 276.00 292.10 322.00<br />

4,700 282.00 298.45 329.00<br />

4,800 288.00 304.80 336.00<br />

4,900 294.00 311.15 343.00<br />

5,000 300.00 317.50 350.00<br />

Schedule <strong>CT</strong>-EITC - <strong>Connecticut</strong> Earned <strong>Income</strong> <strong>Tax</strong> Credit<br />

Who qualifies?<br />

To qualify for the <strong>Connecticut</strong> earned income tax credit<br />

(<strong>CT</strong> EITC) you must:<br />

1. Have claimed and been allowed the <strong>2011</strong> federal earned<br />

income credit (EIC); and<br />

2. Be a resident of the State of <strong>Connecticut</strong>.<br />

Part-year residents and nonresidents do not qualify for the<br />

<strong>CT</strong> EITC.<br />

How to Claim the <strong>Connecticut</strong> Earned <strong>Income</strong><br />

<strong>Tax</strong> Credit<br />

Complete Schedule <strong>CT</strong>-EITC, <strong>Connecticut</strong> Earned <strong>Income</strong><br />

<strong>Tax</strong> Credit, using the information from your federal return,<br />

worksheets, and, if applicable, federal EIC line instructions.<br />

Attach Schedule <strong>CT</strong>-EITC to the back of Form <strong>CT</strong>-<strong>1040</strong>.<br />

Schedule <strong>CT</strong>-EITC - Line instructions<br />

Line 1<br />

You must have claimed the <strong>2011</strong> federal earned income credit<br />

to claim the <strong>CT</strong> EITC.<br />

Line 2<br />

You cannot claim the <strong>CT</strong> EITC if your investment income is<br />

more than $3,150. Investment income is the total amount of:<br />

• <strong>Tax</strong>able interest (federal Form <strong>1040</strong> or <strong>1040</strong>A, Line 8a);<br />

• <strong>Tax</strong>-exempt interest (federal Form <strong>1040</strong> or <strong>1040</strong>A, Line 8b);<br />

• Ordinary dividends income (federal Form <strong>1040</strong> or <strong>1040</strong>A,<br />

Line 9a); and<br />

• Capital gain net income from federal Form <strong>1040</strong>A,<br />

Line 10, or Form <strong>1040</strong>, Line 13 (if more than zero).<br />

For additional information on what qualifies as investment<br />

income, see federal Publication 596, Earned <strong>Income</strong> Credit.<br />

Line 3<br />

File Schedule <strong>CT</strong>-EITC with Form <strong>CT</strong>-<strong>1040</strong>. If Form <strong>CT</strong>-<strong>1040</strong><br />

was already filed, you must file a <strong>2011</strong> Form <strong>CT</strong>-<strong>1040</strong>X to<br />

claim the credit.<br />

Schedule <strong>CT</strong>-EITC cannot be filed by itself. Schedule<br />

<strong>CT</strong>-EITC must be attached to a completed Form <strong>CT</strong>-<strong>1040</strong> or<br />

Form <strong>CT</strong>-<strong>1040</strong>X.<br />

Page 33