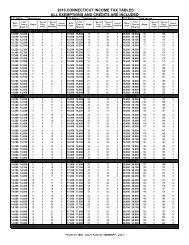

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Relief From Joint Liability<br />

In general, if you and your spouse file a joint income tax<br />

return, you are both responsible for paying the full amount of<br />

tax, interest, and penalties due on your joint return. However,<br />

in very limited, specific cases, relief may be granted if you<br />

believe all or any part of the amount due should be paid<br />

only by your spouse. You may request consideration by<br />

filing Form <strong>CT</strong>-8857, Request for Innocent Spouse Relief<br />

(And Separation of Liability and Equitable Relief). See<br />

Special Notice 99(15), Innocent Spouse Relief, Separation<br />

of Liability, and Equitable Relief.<br />

Title 19 Recipients<br />

Title 19 recipients must file a <strong>Connecticut</strong> income tax return<br />

if the requirements for Who Must File a <strong>Connecticut</strong> <strong>Resident</strong><br />

Return on Page 8 are met.<br />

However, if you do not have funds to pay your <strong>Connecticut</strong><br />

income tax, complete Form <strong>CT</strong>-19IT, Title 19 Status Release,<br />

and attach it to the front of your <strong>Connecticut</strong> income tax<br />

return if the following two conditions apply:<br />

• You were a Title 19 recipient during <strong>2011</strong>; and<br />

• Medicaid assisted in the payment of your long-term care<br />

in a nursing or convalescent home during <strong>2011</strong>.<br />

Completing this form authorizes DRS to verify your Title 19<br />

status for <strong>2011</strong> with the Department of Social Services.<br />

Deceased <strong>Tax</strong>payers<br />

An executor, administrator, or surviving spouse must file a<br />

<strong>Connecticut</strong> income tax return, for that portion of the year<br />

before the taxpayer’s death, for a taxpayer who died during<br />

the year if the requirements for Who Must File a <strong>Connecticut</strong><br />

<strong>Resident</strong> Return are met. The executor, administrator, or<br />

surviving spouse must check the box next to the deceased<br />

taxpayer’s SSN on the front page of the return. The person<br />

filing the return must sign for the deceased taxpayer on the<br />

signature line and indicate the date of death.<br />

Generally, the <strong>Connecticut</strong> and federal filing status must be<br />

the same. A surviving spouse may file jointly for <strong>Connecticut</strong><br />

if the surviving spouse filed a joint federal income tax return.<br />

A surviving spouse in a same sex marriage may file jointly for<br />

<strong>Connecticut</strong> as a surviving spouse although this will not be<br />

their federal filing status. Write “filing as surviving spouse”<br />

in the deceased spouse’s signature line on the return. If both<br />

spouses died in <strong>2011</strong>, their legal representative must file a<br />

final return.<br />

Claiming a Refund for a Deceased <strong>Tax</strong>payer<br />

If you are a surviving spouse filing jointly with your deceased<br />

spouse, you may claim the refund on the jointly-filed return.<br />

If you are a court-appointed representative, file the return and<br />

attach a copy of the certificate that shows your appointment.<br />

All other filers requesting the deceased taxpayer’s refund<br />

must file the return and attach federal Form 1310, Statement<br />

of Person Claiming Refund Due a Deceased <strong>Tax</strong>payer, to the<br />

front of the return.<br />

<strong>Income</strong> received by the estate of the decedent for the portion<br />

of the year after the decedent’s death, and for succeeding<br />

taxable years until the estate is closed, must be reported each<br />

year on Form <strong>CT</strong>-1041, <strong>Connecticut</strong> <strong>Income</strong> <strong>Tax</strong> Return for<br />

Trusts and Estates.<br />

Special Information for Nonresident Aliens<br />

A nonresident alien must file a <strong>Connecticut</strong> income tax<br />

return if he or she meets the requirements of Who Must File<br />

a <strong>Connecticut</strong> <strong>Resident</strong> Return. In determining whether the<br />

gross income test is met, the nonresident alien must take<br />

into account any income not subject to federal income tax<br />

under an income tax treaty between the United States and the<br />

country of which the nonresident alien is a citizen or resident.<br />

<strong>Income</strong> tax treaty provisions are disregarded for <strong>Connecticut</strong><br />

income tax purposes. Any treaty income reported on federal<br />

Form <strong>1040</strong>NR or Form <strong>1040</strong>NR-EZ and not subject to federal<br />

income tax must be added to the nonresident alien’s federal<br />

adjusted gross income. See Form <strong>CT</strong>-<strong>1040</strong>, Schedule 1,<br />

Line 38, or Form <strong>CT</strong>-<strong>1040</strong>NR/PY, Schedule 1, Line 40.<br />

If the nonresident alien does not have and is not eligible<br />

for a Social Security Number (SSN), he or she must obtain<br />

an Individual <strong>Tax</strong>payer Identification Number (ITIN) from<br />

the IRS and enter it in the space provided for an SSN.<br />

DRS no longer processes income tax returns or Form<br />

<strong>CT</strong>-<strong>1040</strong> EXT with “Applied For” or “NRA” entered in the<br />

SSN field. You must have applied for and been issued an ITIN<br />

before you file your income tax return. However, if you have<br />

not received your ITIN by April 15, file your return without the<br />

ITIN, pay the tax due, and attach a copy of the federal Form<br />

W-7. DRS will contact you upon receipt of your return and will<br />

hold your return until you receive your ITIN and you forward<br />

the information to us. If you fail to submit the information<br />

requested, the processing of your return will be delayed.<br />

A married nonresident alien may not file a joint <strong>Connecticut</strong><br />

income tax return unless the nonresident alien is married to<br />

a citizen or resident of the United States and they have made<br />

an election to file a joint federal income tax return and they<br />

do, in fact, file a joint federal income tax return. Any married<br />

individual filing federal Form <strong>1040</strong>NR or federal Form<br />

<strong>1040</strong>NR-EZ is not eligible to file a joint federal income tax<br />

return or a joint <strong>Connecticut</strong> income tax return and must file<br />

a <strong>Connecticut</strong> income tax return as filing separately except<br />

as noted by the following.<br />

A spouse in a same sex marriage who is a nonresident alien<br />

may file a joint <strong>Connecticut</strong> income tax return as long as his<br />

or her spouse is a citizen or resident of the United States.<br />

A spouse filing federal Form <strong>1040</strong>NR or federal Form<br />

<strong>1040</strong>NR-EZ is not eligible to file a joint <strong>Connecticut</strong> income<br />

tax return and must file a <strong>Connecticut</strong> income tax return as<br />

filing separately for <strong>Connecticut</strong> only.<br />

Page 9