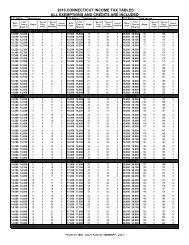

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

CT-1040 Instructions, 2011 Connecticut Resident Income Tax - CT.gov

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Line 4<br />

If claiming qualifying children on federal Schedule EIC, mark<br />

an X in the Yes box and then complete Line 5. Otherwise,<br />

mark an X in the No box and go to Line 6.<br />

Line 5<br />

If claiming qualifying children on federal Schedule EIC,<br />

list the same children (up to three) in the spaces provided.<br />

If claiming more than three qualifying children on federal<br />

Schedule EIC, enter the required information for three<br />

qualifying children in the spaces provided on the schedule and<br />

attach a statement with the required identifying information<br />

for each additional child. Include taxpayer name and social<br />

security number (SSN) on the attachment.<br />

To be eligible to claim the <strong>CT</strong> EITC, a correct and valid SSN<br />

must be provided for each child listed on Line 5, and on an<br />

attached statement, if any.<br />

If a social security number has been applied for by filing<br />

federal Form SS-5 with the Social Security Administration,<br />

but has not been received by the return due date:<br />

1. File Form <strong>CT</strong>-<strong>1040</strong> EXT, to request an extension of time<br />

to file. Form <strong>CT</strong>-<strong>1040</strong> EXT does not extend the time to<br />

pay your income tax. You must pay the amount of tax that<br />

you expect to owe on or before the original due date of the<br />

return (see Form <strong>CT</strong>-<strong>1040</strong> EXT); or<br />

2. File Form <strong>CT</strong>-<strong>1040</strong> on time without claiming the<br />

<strong>CT</strong> EITC (do not attach Schedule <strong>CT</strong>-EITC). After receiving<br />

the SSN, amend the <strong>Connecticut</strong> return using Form<br />

<strong>CT</strong>-<strong>1040</strong>X and attach the completed Schedule <strong>CT</strong>-EITC.<br />

Mark an X in the box confirming each child who was<br />

identified on federal Schedule EIC, box 4a, as a full-time<br />

student.<br />

Mark an X in the box confirming each child who was<br />

identified on federal Schedule EIC, box 4b as disabled.<br />

Line 6<br />

If no <strong>Connecticut</strong> withholding is claimed on Form <strong>CT</strong>-<strong>1040</strong>,<br />

Line 18, and Wages, tips, and other compensation was reported<br />

on forms W-2 or 1099, enter the following information (from<br />

up to three jobs) on Lines 6a, 6b, and 6c:<br />

Column A<br />

Enter the employer’s federal identification number (EIN)<br />

from form W-2 or the payer’s federal identification number<br />

from form 1099.<br />

Column B<br />

Enter the employer’s state identification number from form<br />

W-2 or form 1099.<br />

Column C<br />

Enter wages, tips, and other compensation from form W-2<br />

or form 1099.<br />

Line 7<br />

Business income or loss applies only to federal Form <strong>1040</strong><br />

filers. If income or loss from more than one business is<br />

claimed, enter the following information (for up to three<br />

primary business activities) on Lines 7a, 7b, and 7c:<br />

Column A<br />

Enter the federal employer identification number (EIN) for<br />

the business. If any primary business activity does not have<br />

an EIN, enter your SSN.<br />

Column B<br />

Enter the <strong>Connecticut</strong> tax registration number for the business.<br />

Column C<br />

Enter the amount of business income or loss. Use a minus<br />

sign to show a loss or a negative amount.<br />

Line 8<br />

Enter the federal EIC claimed for tax year <strong>2011</strong> from federal<br />

Form <strong>1040</strong>, Line 64a; Form <strong>1040</strong>A, Line 38a; or Form<br />

<strong>1040</strong>EZ, Line 8a.<br />

<strong>Tax</strong>payers who are spouses in a same sex marriage, filing jointly<br />

for <strong>Connecticut</strong> only, must recalculate their federal return<br />

(including their federal EIC) as if, for federal tax purposes,<br />

they were allowed and elected to file as married filing jointly.<br />

Line 9<br />

For the tax year <strong>2011</strong>, the <strong>CT</strong> EITC is 30% (.30) of the<br />

federal EIC.<br />

Line 11<br />

If your filing status was married filing jointly on your federal<br />

income tax return but you are required to file as married filing<br />

separately on your <strong>Connecticut</strong> Form <strong>CT</strong>-<strong>1040</strong> only, mark<br />

an X in the Yes box and complete Lines 12 through 15. See<br />

<strong>Tax</strong>payer Information, on Page 17.<br />

Otherwise, mark an X in the No box and skip Lines 12<br />

through 15.<br />

Line 16<br />

This is your <strong>Connecticut</strong> Earned <strong>Income</strong> <strong>Tax</strong> Credit. If your<br />

filing status is married filing separately, for <strong>Connecticut</strong> only,<br />

enter the amount from Line 15. Otherwise, enter the amount<br />

from Line 10. Enter the amount from Line 16 on Form<br />

<strong>CT</strong>-<strong>1040</strong>, Line 20a.<br />

Page 34