Does Tail Dependence Make A Difference In the ... - Boston College

Does Tail Dependence Make A Difference In the ... - Boston College

Does Tail Dependence Make A Difference In the ... - Boston College

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

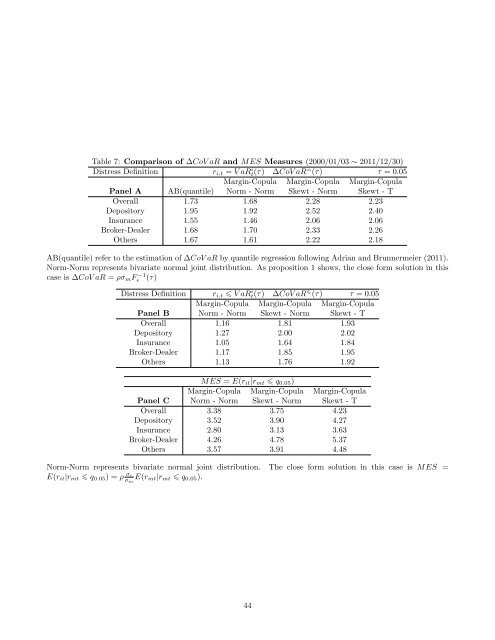

Table 7: Comparison of ∆CoV aR and MES Measures (2000/01/03 ∼ 2011/12/30)<br />

Distress Definition r i,t = V aRt(τ) i ∆CoV aR = (τ) τ = 0.05<br />

Margin-Copula Margin-Copula Margin-Copula<br />

Panel A AB(quantile) Norm - Norm Skewt - Norm Skewt - T<br />

Overall 1.73 1.68 2.28 2.23<br />

Depository 1.95 1.92 2.52 2.40<br />

<strong>In</strong>surance 1.55 1.46 2.06 2.06<br />

Broker-Dealer 1.68 1.70 2.33 2.26<br />

O<strong>the</strong>rs 1.67 1.61 2.22 2.18<br />

AB(quantile) refer to <strong>the</strong> estimation of ∆CoV aR by quantile regression following Adrian and Brunnermeier (2011).<br />

Norm-Norm represents bivariate normal joint distribution. As proposition 1 shows, <strong>the</strong> close form solution in this<br />

case is ∆CoV aR = ρσ m Fɛ<br />

−1 (τ)<br />

Distress Definition r i,t V aRt(τ) i ∆CoV aR (τ) τ = 0.05<br />

Margin-Copula Margin-Copula Margin-Copula<br />

Panel B Norm - Norm Skewt - Norm Skewt - T<br />

Overall 1.16 1.81 1.93<br />

Depository 1.27 2.00 2.02<br />

<strong>In</strong>surance 1.05 1.64 1.84<br />

Broker-Dealer 1.17 1.85 1.95<br />

O<strong>the</strong>rs 1.13 1.76 1.92<br />

MES = E(r it |r mt q 0.05 )<br />

Margin-Copula Margin-Copula Margin-Copula<br />

Panel C Norm - Norm Skewt - Norm Skewt - T<br />

Overall 3.38 3.75 4.23<br />

Depository 3.52 3.90 4.27<br />

<strong>In</strong>surance 2.80 3.13 3.63<br />

Broker-Dealer 4.26 4.78 5.37<br />

O<strong>the</strong>rs 3.57 3.91 4.48<br />

Norm-Norm represents bivariate normal joint distribution. The close form solution in this case is MES =<br />

E(r it |r mt q 0.05 ) = ρ σi<br />

σ m<br />

E(r mt |r mt q 0.05 ).<br />

44