Survey, Search & Seizure Income Tax Act, 1961

Survey, Search & Seizure Income Tax Act, 1961

Survey, Search & Seizure Income Tax Act, 1961

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

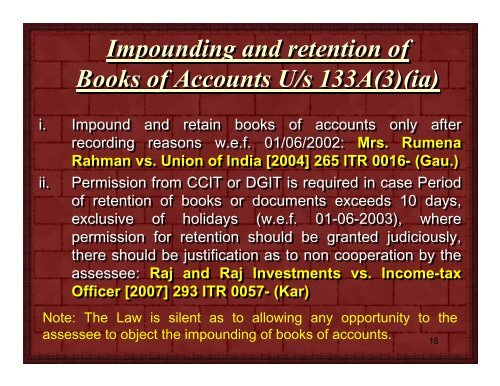

Impounding and retention of<br />

Books of Accounts U/s 133A(3)(ia)<br />

i. Impound and retain books of accounts only after<br />

recording reasons w.e.f. 01/06/2002: Mrs. Rumena<br />

Rahman vs. Union of India [2004] 265 ITR 0016- (Gau.)<br />

ii.<br />

Permission from CCIT or DGIT is required in case Period<br />

of retention of books or documents exceeds 10 days,<br />

exclusive of holidays (w.e.f. 01-06-2003), where<br />

permission for retention should be granted judiciously,<br />

there should be justification as to non cooperation by the<br />

assessee: Raj and Raj Investments vs. <strong>Income</strong>-tax<br />

Officer [2007] 293 ITR 0057- (Kar)<br />

Note: The Law is silent as to allowing any opportunity to the<br />

assessee to object the impounding of books of accounts.<br />

16