Bridging the accountability gap - Audit Commission

Bridging the accountability gap - Audit Commission

Bridging the accountability gap - Audit Commission

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

50<br />

Governing partnerships | Governing partnerships for better <strong>accountability</strong><br />

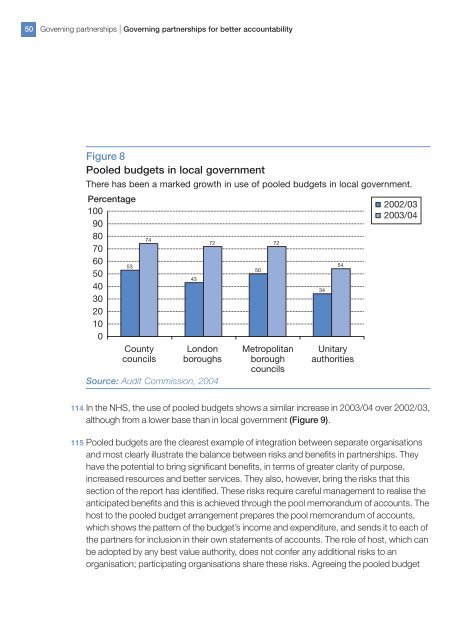

Figure 8<br />

Pooled budgets in local government<br />

There has been a marked growth in use of pooled budgets in local government.<br />

Percentage<br />

100<br />

90<br />

80<br />

74<br />

70<br />

60<br />

53<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

County<br />

councils<br />

Source: <strong>Audit</strong> <strong>Commission</strong>, 2004<br />

43<br />

London<br />

boroughs<br />

72 72<br />

50<br />

Metropolitan<br />

borough<br />

councils<br />

34<br />

54<br />

Unitary<br />

authorities<br />

2002/03<br />

2003/04<br />

114 In <strong>the</strong> NHS, <strong>the</strong> use of pooled budgets shows a similar increase in 2003/04 over 2002/03,<br />

although from a lower base than in local government (Figure 9).<br />

115 Pooled budgets are <strong>the</strong> clearest example of integration between separate organisations<br />

and most clearly illustrate <strong>the</strong> balance between risks and benefits in partnerships. They<br />

have <strong>the</strong> potential to bring significant benefits, in terms of greater clarity of purpose,<br />

increased resources and better services. They also, however, bring <strong>the</strong> risks that this<br />

section of <strong>the</strong> report has identified. These risks require careful management to realise <strong>the</strong><br />

anticipated benefits and this is achieved through <strong>the</strong> pool memorandum of accounts. The<br />

host to <strong>the</strong> pooled budget arrangement prepares <strong>the</strong> pool memorandum of accounts,<br />

which shows <strong>the</strong> pattern of <strong>the</strong> budget’s income and expenditure, and sends it to each of<br />

<strong>the</strong> partners for inclusion in <strong>the</strong>ir own statements of accounts. The role of host, which can<br />

be adopted by any best value authority, does not confer any additional risks to an<br />

organisation; participating organisations share <strong>the</strong>se risks. Agreeing <strong>the</strong> pooled budget