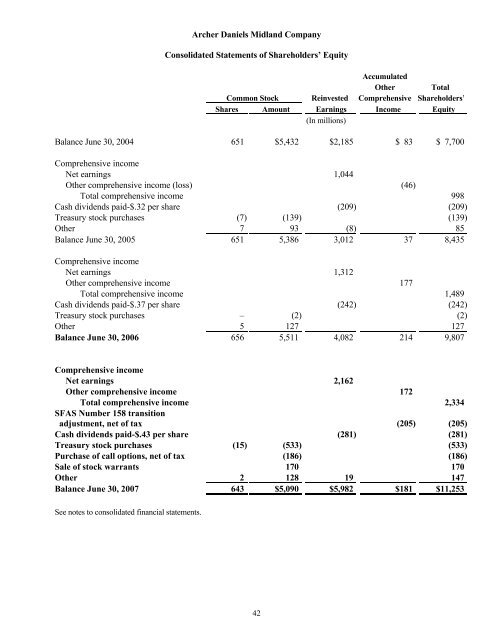

Archer Daniels Midland CompanyConsolidated Statements of Shareholders’ EquityAccumulatedOther TotalCommon Stock Reinvested Comprehensive Shareholders’Shares Amount Earnings Income Equity(In millions)Balance June 30, 2004 651 $5,432 $2,185 $ 83 $ 7,700Comprehensive incomeNet earnings 1,044Other comprehensive income (loss) (46)Total comprehensive income 998Cash dividends paid-$.32 per share (209) (209)Treasury stock purchases (7) (139) (139)Other 7 93 (8) 85Balance June 30, 2005 651 5,386 3,012 37 8,435Comprehensive incomeNet earnings 1,312Other comprehensive income 177Total comprehensive income 1,489Cash dividends paid-$.37 per share (242) (242)Treasury stock purchases – (2) (2)Other 5 127 127Balance June 30, 2006 656 5,511 4,082 214 9,807Comprehensive incomeNet earnings 2,162Other comprehensive income 172Total comprehensive income 2,334SFAS Number 158 transitionadjustment, net of tax (205) (205)Cash dividends paid-$.43 per share (281) (281)Treasury stock purchases (15) (533) (533)Purchase of call options, net of tax (186) (186)Sale of stock warrants 170 170Other 2 128 19 147Balance June 30, 2007 643 $5,090 $5,982 $181 $11,253See notes to consolidated financial statements.42

Archer Daniels Midland CompanyNotes to Consolidated Financial StatementsNote 1.Summary of Significant Accounting PoliciesNature of BusinessThe Company is principally engaged in procuring, transporting, storing, processing, and merchandising agriculturalcommodities and products.Principles of ConsolidationThe consolidated financial statements as of June 30, 2007, and for the three years then ended include the accountsof the Company and its majority-owned subsidiaries. All significant intercompany accounts and transactions havebeen eliminated. Investments in affiliates are carried at cost plus equity in undistributed earnings since acquisition.The Company evaluates its less than majority-owned investments for consolidation pursuant to FinancialAccounting Standards Board (FASB) Interpretation Number 46, Consolidation of Variable Interest Entities, anInterpretation of Accounting Research Bulletin No. 51 (FIN 46). A variable interest entity (VIE) is a corporation,partnership, trust, or any other legal structure used for business purposes that does not have equity investors withvoting rights or has equity investors that do not provide sufficient financial resources for the entity to support itsactivities. FIN 46 requires a VIE to be consolidated by a company if that company is the primary beneficiary of theVIE. The primary beneficiary of a VIE is an entity that is subject to a majority of the risk of loss from the VIE’sactivities or entitled to receive a majority of the entity’s residual returns, or both. As of June 30, 2007, theCompany has $165 million of investments in private equity funds included in investments in affiliates which areconsidered VIEs pursuant to FIN 46. The Company’s residual risk and rewards from these VIEs are proportional tothe Company’s ownership interest and the Company is not the primary beneficiary of any of these VIEs.Therefore, the Company does not consolidate any of these VIEs.Use of EstimatesThe preparation of consolidated financial statements in conformity with generally accepted accounting principlesrequires management to make estimates and assumptions that affect amounts reported in its consolidated financialstatements and accompanying notes. Actual results could differ from those estimates.Cash EquivalentsThe Company considers all non-segregated, highly-liquid investments with a maturity of three months or less at thetime of purchase to be cash equivalents.Segregated Cash and InvestmentsThe Company segregates certain cash and investment balances in accordance with certain regulatory requirements,commodity exchange requirements, and insurance arrangements. These segregated balances represent depositsreceived from customers trading in exchange-traded commodity instruments, securities pledged to commodityexchange clearinghouses, and cash and securities pledged as security under certain insurance arrangements.Segregated cash and investments primarily consist of cash, United States government securities, and money-marketfunds.ReceivablesThe Company records trade accounts receivable at net realizable value. This value includes an appropriateallowance for estimated uncollectible accounts, $69 million and $54 million at June 30, 2007 and 2006,respectively, to reflect any loss anticipated on the trade accounts receivable balances. The Company calculates thisallowance based on its history of write-offs, level of past-due accounts, and its relationships with, and the economicstatus of, its customers.43