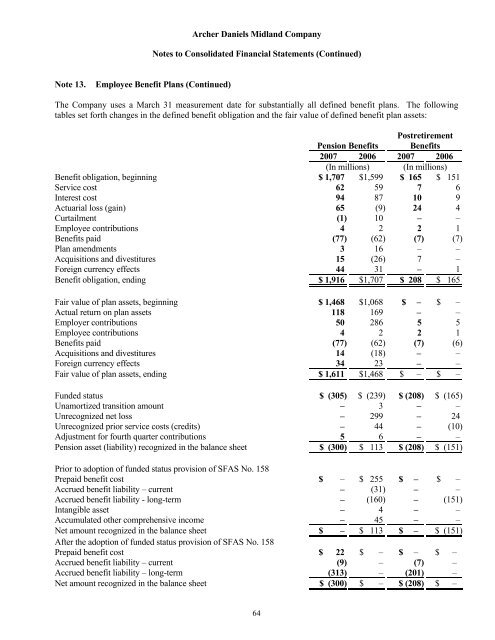

Archer Daniels Midland CompanyNotes to Consolidated Financial Statements (Continued)Note 13.Employee Benefit Plans (Continued)The Company uses a March 31 measurement date for substantially all defined benefit plans. The followingtables set forth changes in the defined benefit obligation and the fair value of defined benefit plan assets:PostretirementPension Benefits Benefits2007 2006 2007 2006(In millions) (In millions)Benefit obligation, beginning $ 1,707 $1,599 $ 165 $ 151Service cost 62 59 7 6Interest cost 94 87 10 9Actuarial loss (gain) 65 (9) 24 4Curtailment (1) 10 – –Employee contributions 4 2 2 1Benefits paid (77) (62) (7) (7)Plan amendments 3 16 – –Acquisitions and divestitures 15 (26) 7 –Foreign currency effects 44 31 – 1Benefit obligation, ending $ 1,916 $1,707 $ 208 $ 165Fair value of plan assets, beginning $ 1,468 $1,068 $ – $ –Actual return on plan assets 118 169 – –Employer contributions 50 286 5 5Employee contributions 4 2 2 1Benefits paid (77) (62) (7) (6)Acquisitions and divestitures 14 (18) – –Foreign currency effects 34 23 – –Fair value of plan assets, ending $ 1,611 $1,468 $ – $ –Funded status $ (305) $ (239) $ (208) $ (165)Unamortized transition amount – 3 – –Unrecognized net loss – 299 – 24Unrecognized prior service costs (credits) – 44 – (10)Adjustment for fourth quarter contributions 5 6 – –Pension asset (liability) recognized in the balance sheet $ (300) $ 113 $ (208) $ (151)Prior to adoption of funded status provision of SFAS No. 158Prepaid benefit cost $ – $ 255 $ – $ –Accrued benefit liability – current – (31) – –Accrued benefit liability - long-term – (160) – (151)Intangible asset – 4 – –Accumulated other comprehensive income – 45 – –Net amount recognized in the balance sheet $ – $ 113 $ – $ (151)After the adoption of funded status provision of SFAS No. 158Prepaid benefit cost $ 22 $ – $ – $ –Accrued benefit liability – current (9) – (7) –Accrued benefit liability – long-term (313) – (201) –Net amount recognized in the balance sheet $ (300) $ – $ (208) $ –64

Archer Daniels Midland CompanyNotes to Consolidated Financial Statements (Continued)Note 13.Employee Benefit Plans (Continued)Included in accumulated other comprehensive income for pension benefits at June 30, 2007, are the followingamounts that have not yet been recognized in net periodic pension cost: Unrecognized transition obligation of $3million, unrecognized prior service costs of $41 million and unrecognized actuarial losses of $336 million. Thetransition obligation, prior service cost, and actuarial loss included in accumulated other comprehensive income andexpected to be recognized in net periodic pension cost during the fiscal year ended June 30, 2008, is ($1) million,$6 million, and $17 million, respectively.Included in accumulated other comprehensive income for postretirement benefits at June 30, 2007, are thefollowing amounts that have not yet been recognized in net periodic pension cost: unrecognized prior servicecredits of $9 million and unrecognized actuarial losses of $47 million. The prior service credit and actuarial lossincluded in accumulated other comprehensive income and expected to be recognized in net periodic pension costduring the fiscal year ended June 30, 2008, is $1 million, and $2 million, respectively.The following table sets forth the principal assumptions used in developing the benefit obligation and the netperiodic pension expense:Pension BenefitsPostretirement Benefits2007 2006 2007 2006Discount rate 5.6% 5.5% 6.0% 6.0%Expected return on plan assets 7.2% 7.3% N/A N/ARate of compensation increase 4.1% 3.7% N/A N/AThe projected benefit obligation, accumulated benefit obligation, and fair value of plan assets for the pensionplans with projected benefit obligations in excess of plan assets were $1.7 billion, $1.5 billion, and $1.4 billion,respectively, as of June 30, 2007, and $1.3 billion, $1.1 billion, and $1.1 billion, respectively, as ofJune 30, 2006. The projected benefit obligation, accumulated benefit obligation, and fair value of plan assets forthe pension plans with accumulated benefit obligations in excess of plan assets were $491 million, $481 million,and $284 million, respectively, as of June 30, 2007, and $213 million, $198 million, and $25 million,respectively, as of June 30, 2006. The accumulated benefit obligation for all pension plans as of June 30, 2007and 2006, was $1.7 billion and $1.5 billion, respectively.For postretirement benefit measurement purposes, a 9.1% annual rate of increase in the per capita cost ofcovered health care benefits was assumed for 2007. The rate was assumed to decrease gradually to 5.0% for2016 and remain at that level thereafter.Assumed health care cost trend rates have a significant impact on the amounts reported for the health care plans.A 1% change in assumed health care cost trend rates would have the following effect:1% Increase 1% Decrease(In millions)Effect on combined service and interest cost components $ 2 $ (2)Effect on accumulated postretirement benefit obligations $ 20 $ (18)65