<strong>Pinewood</strong> <strong>Studios</strong> Ltd<strong>Pinewood</strong> <strong>Studios</strong>: <strong>Business</strong> <strong>Case</strong> <strong>and</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>Assessment</strong>January 201314. Production costs are increasing <strong>and</strong> are being driven by the use of a greater number of sets,more expansive <strong>and</strong> elaborate sets, more intricate props, increased use of digital editing <strong>and</strong>special effects <strong>and</strong> larger production teams. The dem<strong>and</strong> for space, in terms of both the size<strong>and</strong> height of the studios, is also being fuelled by a move away from location filming for highbudget productions <strong>and</strong> a consequent increased dem<strong>and</strong> for sets constructed within major stage<strong>and</strong> studio facilities – which gives rise to an increased dem<strong>and</strong> for ancillary space such asworkshops with increased height <strong>and</strong> production offices.15. Major television productions, such as high-end drama <strong>and</strong> large-scale live entertainment showsare also driving dem<strong>and</strong>. In response to consumer trends, broadcasters are investing in biggerbudget, large-scale <strong>and</strong> high quality TV productions that require extensive studio space <strong>and</strong> topendfacilities such as those provided by <strong>Pinewood</strong>. The total costs for a premium drama seriescan now be similar to those of a large feature film.16. In addition, there are a wide range of other opportunities including video games, music, visualeffects <strong>and</strong> animation that will continue to increase dem<strong>and</strong> for facilities like <strong>Pinewood</strong> with theability to produce audio <strong>and</strong> video game content. While the growth in digital technology haschanged the way people consume entertainment <strong>and</strong> media, detailed discussions with key USStudio Heads of Production <strong>and</strong> other production companies have clearly indicated that the useof new technology, for example computer generated images (CGI) <strong>and</strong> 3D technology, are not atthe expense of real set construction within major stages <strong>and</strong> studio facilities. These sets remaina core element of the film <strong>and</strong> production process, providing actors with a real sense of thescene they are acting in.17. In order to capitalise on these growing markets, studios have to offer a competitive package toattract film <strong>and</strong> TV productions. Fiscal incentives, exchange rates, the availability of skilledlabour, <strong>and</strong> the quality <strong>and</strong> size of the studios <strong>and</strong> ancillary facilities all contribute to thedecision making process. A number of other locations are investing heavily in infrastructure <strong>and</strong>skills to compete with <strong>Pinewood</strong> <strong>and</strong> the other 10 studios 2 that have produced the major featurefilms with production budgets of over $100 million in the last three years.18. To retain its current competitive advantage therefore, <strong>Pinewood</strong> needs to respond to themarket <strong>and</strong> address the underlying lack of space. Specific considerations include the need totake account of stage size (i.e. larger stages), stage height (with significant clearance up to 50 ft),ancillary space (as productions often use as much or more workshop/office space as actualshooting space), backlots (required to build substantial sets), streetscapes <strong>and</strong> the provision offilm studio complexes, that keep up with advancing digital production technology, ensure highspeed connectivity, <strong>and</strong> provide security <strong>and</strong> on-site editing facilities.19. PwC has prepared projections of the potential growth in UK film production expenditure underthree scenarios – inflation only case, base case <strong>and</strong> 17% market share case. These expenditureprojections have been used to derive estimates of the future amount of stage <strong>and</strong> ancillarystudio space required to accommodate the projected growth within the UK. As shown in TableES1 below in 2013 PwC project that £395 million of UK film production expenditure will relate to<strong>Pinewood</strong> Studio based productions.2WB Leavesden; Longcross; Universal; Raleigh Manhattan Beach; Sony Pictures; WB Burbank; Raleigh Playa Vista; Raleigh Baton Rouge; <strong>and</strong>Canadian Motion Picture Parkiv

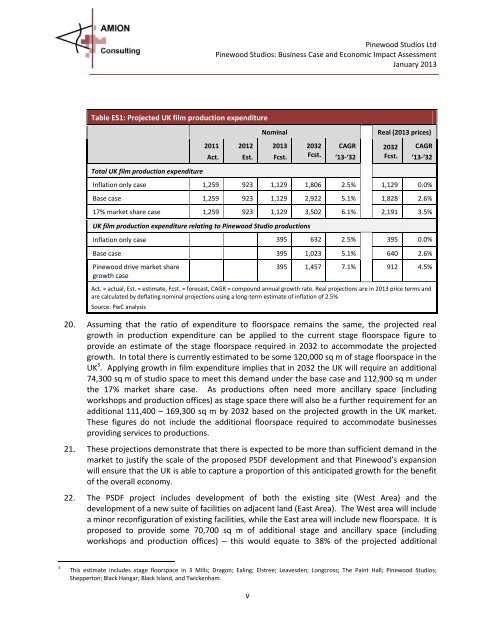

<strong>Pinewood</strong> <strong>Studios</strong> Ltd<strong>Pinewood</strong> <strong>Studios</strong>: <strong>Business</strong> <strong>Case</strong> <strong>and</strong> <strong>Economic</strong> <strong>Impact</strong> <strong>Assessment</strong>January 2013Table ES1: Projected UK film production expenditureTotal UK film production expenditure2011Act.2012Est.Nominal2013Fcst.2032Fcst.CAGR‘13-‘32Real (2013 prices)2032Fcst.CAGR‘13-‘32Inflation only case 1,259 923 1,129 1,806 2.5% 1,129 0.0%Base case 1,259 923 1,129 2,922 5.1% 1,828 2.6%17% market share case 1,259 923 1,129 3,502 6.1% 2,191 3.5%UK film production expenditure relating to <strong>Pinewood</strong> Studio productionsInflation only case 395 632 2.5% 395 0.0%Base case 395 1,023 5.1% 640 2.6%<strong>Pinewood</strong> drive market sharegrowth case395 1,457 7.1% 912 4.5%Act. = actual, Est. = estimate, Fcst. = forecast, CAGR = compound annual growth rate. Real projections are in 2013 price terms <strong>and</strong>are calculated by deflating nominal projections using a long-term estimate of inflation of 2.5%Source: PwC analysis20. Assuming that the ratio of expenditure to floorspace remains the same, the projected realgrowth in production expenditure can be applied to the current stage floorspace figure toprovide an estimate of the stage floorspace required in 2032 to accommodate the projectedgrowth. In total there is currently estimated to be some 120,000 sq m of stage floorspace in theUK 3 . Applying growth in film expenditure implies that in 2032 the UK will require an additional74,300 sq m of studio space to meet this dem<strong>and</strong> under the base case <strong>and</strong> 112,900 sq m underthe 17% market share case. As productions often need more ancillary space (includingworkshops <strong>and</strong> production offices) as stage space there will also be a further requirement for anadditional 111,400 – 169,300 sq m by 2032 based on the projected growth in the UK market.These figures do not include the additional floorspace required to accommodate businessesproviding services to productions.21. These projections demonstrate that there is expected to be more than sufficient dem<strong>and</strong> in themarket to justify the scale of the proposed PSDF development <strong>and</strong> that <strong>Pinewood</strong>’s expansionwill ensure that the UK is able to capture a proportion of this anticipated growth for the benefitof the overall economy.22. The PSDF project includes development of both the existing site (West Area) <strong>and</strong> thedevelopment of a new suite of facilities on adjacent l<strong>and</strong> (East Area). The West area will includea minor reconfiguration of existing facilities, while the East area will include new floorspace. It isproposed to provide some 70,700 sq m of additional stage <strong>and</strong> ancillary space (includingworkshops <strong>and</strong> production offices) – this would equate to 38% of the projected additional3This estimate includes stage floorspace in 3 Mills; Dragon; Ealing; Elstree; Leavesden; Longcross; The Paint Hall; <strong>Pinewood</strong> <strong>Studios</strong>;Shepperton; Black Hangar; Black Isl<strong>and</strong>, <strong>and</strong> Twickenham.v