Barrier Option Pricing Using Adjusted Transition Probabilities

Barrier Option Pricing Using Adjusted Transition Probabilities

Barrier Option Pricing Using Adjusted Transition Probabilities

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

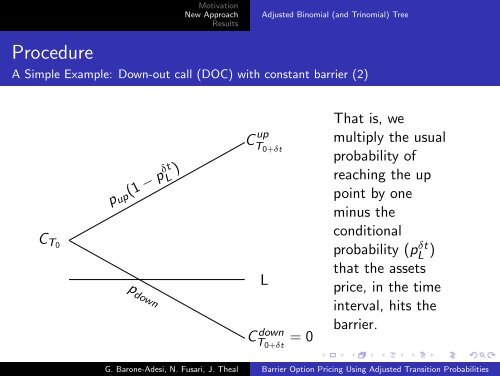

MotivationNew ApproachResults<strong>Adjusted</strong> Binomial (and Trinomial) TreeProcedureA Simple Example: Down-out call (DOC) with constant barrier (2)C T0p up (1 − p δtL )p downC upT 0+δtLC downT 0+δt= 0That is, wemultiply the usualprobability ofreaching the uppoint by oneminus theconditionalprobability (pL δt)that the assetsprice, in the timeinterval, hits thebarrier.G. Barone-Adesi, N. Fusari, J. Theal <strong>Barrier</strong> <strong>Option</strong> <strong>Pricing</strong> <strong>Using</strong> <strong>Adjusted</strong> <strong>Transition</strong> <strong>Probabilities</strong>