What have we learnt <strong>from</strong> his<strong>to</strong>ry?What have we learnt<strong>from</strong> his<strong>to</strong>ry?They say “…you never know where you’re going until you know whereyou’ve come <strong>from</strong>…”. Everybody seems <strong>to</strong> know that, yet it is difficult <strong>to</strong>see that <strong>the</strong> oil tanker market may have learnt much <strong>from</strong> his<strong>to</strong>ry.Text: Jakub Walenkiewicz, DNVThere is an undeniable parallel between<strong>to</strong>day’s scenario and <strong>the</strong> problems tha<strong>to</strong>ccurred back in <strong>the</strong> 1970s, and thisgreatly troubles ship owners. Issues suchas freight rates below operational costs,plummeting asset values and weak demandall paint a gloomy picture of <strong>the</strong> future. Sowhat went wrong?Back in <strong>the</strong> 1970s, <strong>the</strong> Suez Canal closurecombined with rapid growth in UScrude imports initiated growth of 300% in<strong>the</strong> oil tanker fleet in just five years (almostentirely due <strong>to</strong> VLCCs and ULCCs). However,<strong>the</strong>se market conditions did not lastlong as <strong>the</strong> Canal was re-opened in 1975and, coincidently, US imports started <strong>to</strong>decline at <strong>the</strong> same time, leaving vast <strong>to</strong>nnagewithout employment. Consequently,<strong>the</strong> fleet shrank drastically and 28 yearspassed before it reached <strong>the</strong> same volumeas in 1976.In 20<strong>02</strong>, <strong>the</strong> fleet development pickedup momentum again. The shippingboom pushed <strong>the</strong> tanker order book <strong>to</strong>nearly 180 million DWT and subsequently›› Jakub Walenkiewicz, Senior Market Analystaccelerated <strong>the</strong> fleet’s growth <strong>to</strong> over 8%per annum. This time, <strong>the</strong> sentiment wasmainly fuelled by globalisation and <strong>the</strong>rapid expansion of developing economiessuch as <strong>the</strong> BRIC countries. There werealso more pragmatic reasons, such as <strong>the</strong>necessity of replacing single-hull <strong>to</strong>nnage.Interestingly enough, even <strong>the</strong> almost fivefoldincrease in <strong>the</strong> oil price did not manage<strong>to</strong> affect <strong>the</strong> growing demand for oil.When <strong>the</strong> market crashed in 2008, itbecame clear that <strong>the</strong> fundamentals werenot as strong as predicted. Oil consumptionis still increasing by around 1% p.a.and is currently at 89.2 mbd (IEA) p.a.Had <strong>the</strong> average trend prior <strong>to</strong> <strong>the</strong> recessioncontinued, consumption would bealmost 3 mbd higher <strong>to</strong>day! Increasinglyavailable natural gas, which is a cleanersource of energy, has begun <strong>to</strong> replace oil.In addition, <strong>the</strong> environmental pressuresand declining consumption in <strong>the</strong> developedcountries have decreased seaborneoil transportation. It is worth mentioningthat high oil prices support increasedproduction <strong>from</strong> deep-sea fields as wellas <strong>from</strong> unconventional sources (tigh<strong>to</strong>il, shale oil). In both cases, <strong>the</strong> US hasabundant reserves. In addition, <strong>the</strong> US iscatered for by Canada, with its constantlygrowing production <strong>from</strong> oil sands. All<strong>the</strong>se aspects have a negative influenceon oil shipments, particularly <strong>to</strong> <strong>the</strong> US,which is still <strong>the</strong> world’s largest consumer.His<strong>to</strong>ry is once more repeating itself.30 | Tanker UPDATE NO. 2 <strong>2011</strong>

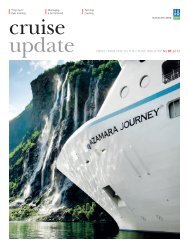

What have we learnt <strong>from</strong> his<strong>to</strong>ry?450Oil tankers – fleet developmentBased upon DWT. Source: IHS Fairplay400DWT [mill <strong>to</strong>nnes]35030<strong>02</strong>5<strong>02</strong>0015010<strong>02</strong>8 YEARS!!500197019751980198519901995200<strong>02</strong>0052010Small Handy Panamax Aframax Suezmax VLCCIt is not all bad news though. Emergingeconomies are increasingly hungrier foroil. Refinery capacity is gradually diminishingin Europe and <strong>No</strong>rth America whileincreasing in <strong>the</strong> Middle and Far East, creatingopportunities for product tankers in<strong>the</strong> future (<strong>to</strong>nne-mile effect).The current fleet is capable of transportingforecast volumes over <strong>the</strong> next fewyears. According <strong>to</strong> IHS Fairplay, <strong>the</strong> currentfleet contains over 3,300 ships, corresponding<strong>to</strong> 4<strong>02</strong> million DWT (crude andproduct tankers over 10k DWT). Yet ano<strong>the</strong>r418 ships (72 million DWT) remain in<strong>the</strong> order book. Scrapping will not be able<strong>to</strong> extinguish <strong>the</strong> <strong>to</strong>nnage increase substantially,as <strong>the</strong> fleet is very young and offerslimited replacement opportunities.The question is, what will happennow? On one hand, we still have stronglong-term fundamentals with incrementaldemand for oil. On <strong>the</strong> o<strong>the</strong>r, <strong>the</strong>re is asubstantial oversupply of ships and weakshort-term forecast for seaborne transport.Are we facing yet ano<strong>the</strong>r collapse in <strong>the</strong>oil tanker market? Perhaps not as bad as<strong>the</strong> one in <strong>the</strong> 1980s, but <strong>the</strong> coming yearswill definitely be challenging. The philosopherGeorge Santayana said: “Those whocannot remember <strong>the</strong> past are condemned<strong>to</strong> repeat it”. Do we remember? Tanker <strong>update</strong> NO. 2 <strong>2011</strong> | 31