Annual Report 2016

Annual Report 2016 - Federal Audit Oversight Authority FAOA

Annual Report 2016 - Federal Audit Oversight Authority FAOA

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

50<br />

Appendix | FAOA <strong>2016</strong><br />

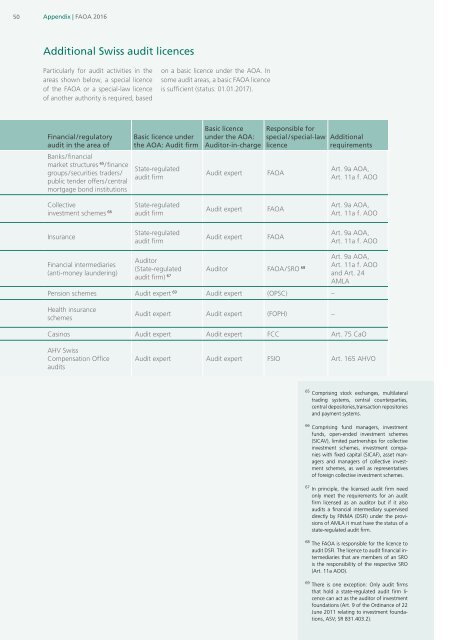

Additional Swiss audit licences<br />

Particularly for audit activities in the<br />

areas shown below, a special licence<br />

of the FAOA or a special-law licence<br />

of another authority is required, based<br />

on a basic licence under the AOA. In<br />

some audit areas, a basic FAOA licence<br />

is sufficient (status: 01.01.2017).<br />

Financial/regulatory<br />

audit in the area of<br />

Banks/financial<br />

market structures 65 /finance<br />

groups/securities traders/<br />

public tender offers/central<br />

mortgage bond institutions<br />

Basic licence under<br />

the AOA: Audit firm<br />

State-regulated<br />

audit firm<br />

Basic licence<br />

under the AOA:<br />

Auditor-in-charge<br />

Audit expert<br />

Responsible for<br />

special / special-law<br />

licence<br />

FAOA<br />

Additional<br />

requirements<br />

Art. 9a AOA,<br />

Art. 11a f. AOO<br />

Collective<br />

investment schemes 66<br />

State-regulated<br />

audit firm<br />

Audit expert<br />

FAOA<br />

Art. 9a AOA,<br />

Art. 11a f. AOO<br />

Insurance<br />

State-regulated<br />

audit firm<br />

Audit expert<br />

FAOA<br />

Art. 9a AOA,<br />

Art. 11a f. AOO<br />

Financial intermediaries<br />

(anti-money laundering)<br />

Art. 9a AOA,<br />

Auditor<br />

Art. 11a f. AOO<br />

(State-regulated Auditor FAOA/SRO 68 and Art. 24<br />

audit firm) 67 AMLA<br />

Pension schemes Audit expert 69 Audit expert (OPSC) –<br />

Health insurance<br />

schemes<br />

Audit expert Audit expert (FOPH) –<br />

Casinos Audit expert Audit expert FCC Art. 75 CaO<br />

AHV Swiss<br />

Compensation Office<br />

audits<br />

Audit expert Audit expert FSIO Art. 165 AHVO<br />

65 Comprising stock exchanges, multilateral<br />

trading systems, central counterparties,<br />

central depositories,transaction repositories<br />

and payment systems.<br />

66 Comprising fund managers, investment<br />

funds, open-ended investment schemes<br />

(SICAV), limited partnerships for collective<br />

investment schemes, investment companies<br />

with fixed capital (SICAF), asset managers<br />

and managers of collective investment<br />

schemes, as well as representatives<br />

of foreign collective investment schemes.<br />

67 In principle, the licensed audit firm need<br />

only meet the requirements for an audit<br />

firm licensed as an auditor but if it also<br />

audits a financial intermediary supervised<br />

directly by FINMA (DSFI) under the provisions<br />

of AMLA it must have the status of a<br />

state-regulated audit firm.<br />

68 The FAOA is responsible for the licence to<br />

audit DSFI. The licence to audit financial intermediaries<br />

that are members of an SRO<br />

is the responsibility of the respective SRO<br />

(Art. 11a AOO).<br />

69 There is one exception: Only audit firms<br />

that hold a state-regulated audit firm licence<br />

can act as the auditor of investment<br />

foundations (Art. 9 of the Ordinance of 22<br />

June 2011 relating to investment foundations,<br />

ASV; SR 831.403.2).