Non-parametric estimation of a time varying GARCH model

Non-parametric estimation of a time varying GARCH model

Non-parametric estimation of a time varying GARCH model

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

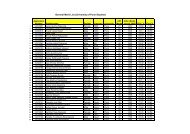

34<br />

Table 4: Aggregated mean squared errors <strong>of</strong> the out <strong>of</strong> sample volatility forecasts<br />

Series tv<strong>GARCH</strong> tv<strong>GARCH</strong> tvARCH (1) tvARCH (2) <strong>GARCH</strong> E<strong>GARCH</strong> GJR FI<strong>GARCH</strong><br />

(d = 3) (d = 1)<br />

INR/USD 0.1975 0.2093 0.2148 0.2159 0.2104 0.2132 0.2105 0.2060<br />

INR/EURO 12.7829 12.0691 12.7828 12.7831 12.2632 12.5052 12.3108 12.1515<br />

CNY/USD 0.0053 0.0056 0.0054 0.0050 0.0051 − 0.0052 0.0051<br />

CNY/EURO 0.4956 0.4827 0.4733 0.5365 0.4609 0.4825 0.4649 0.4525<br />

BRL/USD 0.5638 0.5235 0.5505 0.5769 0.5225 0.5804 0.5469 0.5208<br />

BRL/EURO 0.6297 0.5962 0.6325 0.6290 0.6796 0.6889 0.6312 0.6610<br />

RUB/EURO 0.2928 0.2835 0.2994 0.3245 0.3002 0.3049 0.2992 0.3004<br />

RND/EURO 0.3176 0.2579 0.2664 0.3097 0.3470 0.2883 0.3253 0.3036<br />

S & P 500 1.5806 1.4883 1.6848 1.6141 1.4323 1.2191 1.2502 1.4648<br />

Dow Jones 2.4202 2.0835 2.2603 2.0234 1.8905 1.6448 1.6792 1.9229<br />

BSE 3.9336 3.7315 3.9902 4.1654 3.9710 4.6607 4.0103 3.9286<br />

NSE 4.0292 3.8433 3.9642 4.1683 3.9634 5.1846 4.0816 3.9559