Kennzahlen im Portfolio und Asset Management - Lehrstuhl für ...

Kennzahlen im Portfolio und Asset Management - Lehrstuhl für ...

Kennzahlen im Portfolio und Asset Management - Lehrstuhl für ...

Sie wollen auch ein ePaper? Erhöhen Sie die Reichweite Ihrer Titel.

YUMPU macht aus Druck-PDFs automatisch weboptimierte ePaper, die Google liebt.

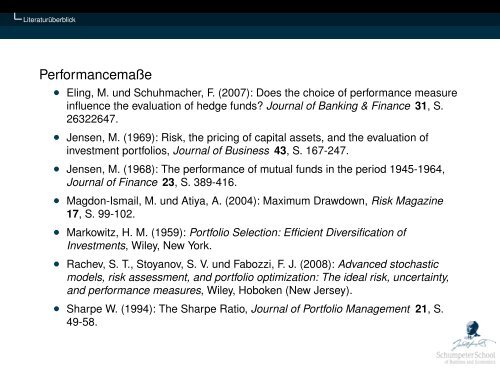

Literaturüberblick<br />

Performancemaße<br />

• Eling, M. <strong>und</strong> Schuhmacher, F. (2007): Does the choice of performance measure<br />

influence the evaluation of hedge f<strong>und</strong>s? Journal of Banking & Finance 31, S.<br />

26322647.<br />

• Jensen, M. (1969): Risk, the pricing of capital assets, and the evaluation of<br />

investment portfolios, Journal of Business 43, S. 167-247.<br />

• Jensen, M. (1968): The performance of mutual f<strong>und</strong>s in the period 1945-1964,<br />

Journal of Finance 23, S. 389-416.<br />

• Magdon-Ismail, M. <strong>und</strong> Atiya, A. (2004): Max<strong>im</strong>um Drawdown, Risk Magazine<br />

17, S. 99-102.<br />

• Markowitz, H. M. (1959): <strong>Portfolio</strong> Selection: Efficient Diversification of<br />

Investments, Wiley, New York.<br />

• Rachev, S. T., Stoyanov, S. V. <strong>und</strong> Fabozzi, F. J. (2008): Advanced stochastic<br />

models, risk assessment, and portfolio opt<strong>im</strong>ization: The ideal risk, uncertainty,<br />

and performance measures, Wiley, Hoboken (New Jersey).<br />

• Sharpe W. (1994): The Sharpe Ratio, Journal of <strong>Portfolio</strong> <strong>Management</strong> 21, S.<br />

49-58.