BERKSHIRE HATHAWAY

BERKSHIRE HATHAWAY

BERKSHIRE HATHAWAY

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Management’s Discussion (Continued)<br />

Derivative contract liabilities (Continued)<br />

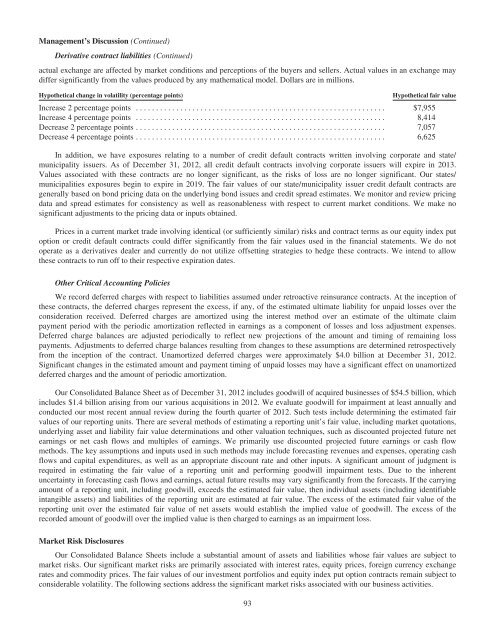

actual exchange are affected by market conditions and perceptions of the buyers and sellers. Actual values in an exchange may<br />

differ significantly from the values produced by any mathematical model. Dollars are in millions.<br />

Hypothetical change in volatility (percentage points) Hypothetical fair value<br />

Increase 2 percentage points .............................................................. $7,955<br />

Increase 4 percentage points .............................................................. 8,414<br />

Decrease 2 percentage points .............................................................. 7,057<br />

Decrease 4 percentage points .............................................................. 6,625<br />

In addition, we have exposures relating to a number of credit default contracts written involving corporate and state/<br />

municipality issuers. As of December 31, 2012, all credit default contracts involving corporate issuers will expire in 2013.<br />

Values associated with these contracts are no longer significant, as the risks of loss are no longer significant. Our states/<br />

municipalities exposures begin to expire in 2019. The fair values of our state/municipality issuer credit default contracts are<br />

generally based on bond pricing data on the underlying bond issues and credit spread estimates. We monitor and review pricing<br />

data and spread estimates for consistency as well as reasonableness with respect to current market conditions. We make no<br />

significant adjustments to the pricing data or inputs obtained.<br />

Prices in a current market trade involving identical (or sufficiently similar) risks and contract terms as our equity index put<br />

option or credit default contracts could differ significantly from the fair values used in the financial statements. We do not<br />

operate as a derivatives dealer and currently do not utilize offsetting strategies to hedge these contracts. We intend to allow<br />

these contracts to run off to their respective expiration dates.<br />

Other Critical Accounting Policies<br />

We record deferred charges with respect to liabilities assumed under retroactive reinsurance contracts. At the inception of<br />

these contracts, the deferred charges represent the excess, if any, of the estimated ultimate liability for unpaid losses over the<br />

consideration received. Deferred charges are amortized using the interest method over an estimate of the ultimate claim<br />

payment period with the periodic amortization reflected in earnings as a component of losses and loss adjustment expenses.<br />

Deferred charge balances are adjusted periodically to reflect new projections of the amount and timing of remaining loss<br />

payments. Adjustments to deferred charge balances resulting from changes to these assumptions are determined retrospectively<br />

from the inception of the contract. Unamortized deferred charges were approximately $4.0 billion at December 31, 2012.<br />

Significant changes in the estimated amount and payment timing of unpaid losses may have a significant effect on unamortized<br />

deferred charges and the amount of periodic amortization.<br />

Our Consolidated Balance Sheet as of December 31, 2012 includes goodwill of acquired businesses of $54.5 billion, which<br />

includes $1.4 billion arising from our various acquisitions in 2012. We evaluate goodwill for impairment at least annually and<br />

conducted our most recent annual review during the fourth quarter of 2012. Such tests include determining the estimated fair<br />

values of our reporting units. There are several methods of estimating a reporting unit’s fair value, including market quotations,<br />

underlying asset and liability fair value determinations and other valuation techniques, such as discounted projected future net<br />

earnings or net cash flows and multiples of earnings. We primarily use discounted projected future earnings or cash flow<br />

methods. The key assumptions and inputs used in such methods may include forecasting revenues and expenses, operating cash<br />

flows and capital expenditures, as well as an appropriate discount rate and other inputs. A significant amount of judgment is<br />

required in estimating the fair value of a reporting unit and performing goodwill impairment tests. Due to the inherent<br />

uncertainty in forecasting cash flows and earnings, actual future results may vary significantly from the forecasts. If the carrying<br />

amount of a reporting unit, including goodwill, exceeds the estimated fair value, then individual assets (including identifiable<br />

intangible assets) and liabilities of the reporting unit are estimated at fair value. The excess of the estimated fair value of the<br />

reporting unit over the estimated fair value of net assets would establish the implied value of goodwill. The excess of the<br />

recorded amount of goodwill over the implied value is then charged to earnings as an impairment loss.<br />

Market Risk Disclosures<br />

Our Consolidated Balance Sheets include a substantial amount of assets and liabilities whose fair values are subject to<br />

market risks. Our significant market risks are primarily associated with interest rates, equity prices, foreign currency exchange<br />

rates and commodity prices. The fair values of our investment portfolios and equity index put option contracts remain subject to<br />

considerable volatility. The following sections address the significant market risks associated with our business activities.<br />

93