Financial Responsibility, Personality Traits and Financial Decision ...

Financial Responsibility, Personality Traits and Financial Decision ...

Financial Responsibility, Personality Traits and Financial Decision ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

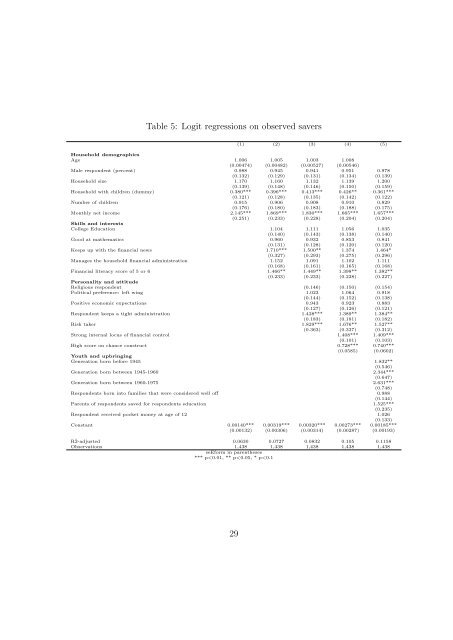

Table 5: Logit regressions on observed savers<br />

(1) (2) (3) (4) (5)<br />

Household demographics<br />

Age 1.006 1.005 1.003 1.008<br />

(0.00474) (0.00482) (0.00527) (0.00546)<br />

Male respondent (percent) 0.988 0.945 0.941 0.951 0.978<br />

(0.132) (0.129) (0.131) (0.134) (0.139)<br />

Household size 1.170 1.160 1.132 1.139 1.200<br />

(0.139) (0.148) (0.146) (0.150) (0.159)<br />

Household with children (dummy) 0.380*** 0.396*** 0.413*** 0.426** 0.361***<br />

(0.121) (0.128) (0.135) (0.142) (0.122)<br />

Number of children 0.915 0.906 0.908 0.910 0.829<br />

(0.176) (0.180) (0.183) (0.188) (0.175)<br />

Monthly net income 2.145*** 1.869*** 1.830*** 1.665*** 1.657***<br />

(0.251) (0.233) (0.228) (0.204) (0.204)<br />

Skills <strong>and</strong> interests<br />

College Education 1.104 1.111 1.056 1.035<br />

(0.140) (0.143) (0.138) (0.140)<br />

Good at mathematics 0.960 0.932 0.853 0.841<br />

(0.131) (0.128) (0.120) (0.120)<br />

Keeps up with the financial news 1.710*** 1.500** 1.374 1.464*<br />

(0.327) (0.293) (0.275) (0.296)<br />

Manages the household financial administration 1.152 1.091 1.102 1.111<br />

(0.168) (0.161) (0.165) (0.168)<br />

<strong>Financial</strong> literacy score of 5 or 6 1.466** 1.449** 1.398** 1.382**<br />

(0.233) (0.233) (0.228) (0.227)<br />

<strong>Personality</strong> <strong>and</strong> attitude<br />

Religious respondent (0.146) (0.150) (0.154)<br />

Political preference: left wing 1.023 1.064 0.918<br />

(0.144) (0.152) (0.138)<br />

Positive economic expectations 0.943 0.923 0.883<br />

(0.127) (0.126) (0.121)<br />

Respondent keeps a tight administration 1.428*** 1.389** 1.384**<br />

(0.183) (0.181) (0.182)<br />

Risk taker 1.829*** 1.676** 1.527**<br />

(0.363) (0.337) (0.312)<br />

Strong internal locus of financial control 1.408*** 1.409***<br />

(0.101) (0.103)<br />

High score on chance construct 0.728*** 0.740***<br />

(0.0585) (0.0602)<br />

Youth <strong>and</strong> upbringing<br />

Generation born before 1945 1.832**<br />

(0.546)<br />

Generation born between 1945-1960 2.344***<br />

(0.647)<br />

Generation born between 1960-1975 2.631***<br />

(0.748)<br />

Respondents born into families that were considered well off 0.988<br />

(0.144)<br />

Parents of respondents saved for respondents education 1.525***<br />

(0.235)<br />

Respondent received pocket money at age of 12 1.026<br />

(0.133)<br />

Constant 0.00140*** 0.00319*** 0.00320*** 0.00273*** 0.00185***<br />

(0.00132) (0.00306) (0.00314) (0.00287) (0.00193)<br />

Rˆ2-adjusted 0.0630 0.0727 0.0832 0.105 0.1158<br />

Observations 1,438 1,438 1,438 1,438 1,438<br />

seEform in parentheses<br />

*** p