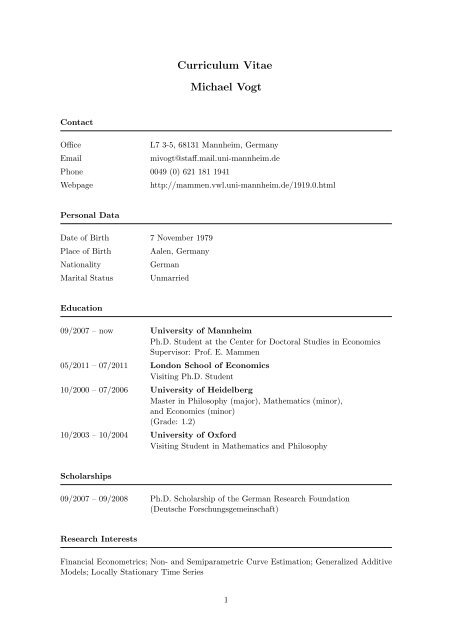

Curriculum Vitae Michael Vogt

Curriculum Vitae Michael Vogt

Curriculum Vitae Michael Vogt

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Contact<br />

<strong>Curriculum</strong> <strong>Vitae</strong><br />

<strong>Michael</strong> <strong>Vogt</strong><br />

Office L7 3-5, 68131 Mannheim, Germany<br />

Email mivogt@staff.mail.uni-mannheim.de<br />

Phone 0049 (0) 621 181 1941<br />

Webpage http://mammen.vwl.uni-mannheim.de/1919.0.html<br />

Personal Data<br />

Date of Birth 7 November 1979<br />

Place of Birth Aalen, Germany<br />

Nationality German<br />

Marital Status Unmarried<br />

Education<br />

09/2007 – now University of Mannheim<br />

Ph.D. Student at the Center for Doctoral Studies in Economics<br />

Supervisor: Prof. E. Mammen<br />

05/2011 – 07/2011 London School of Economics<br />

Visiting Ph.D. Student<br />

10/2000 – 07/2006 University of Heidelberg<br />

Master in Philosophy (major), Mathematics (minor),<br />

and Economics (minor)<br />

(Grade: 1.2)<br />

10/2003 – 10/2004 University of Oxford<br />

Visiting Student in Mathematics and Philosophy<br />

Scholarships<br />

09/2007 – 09/2008 Ph.D. Scholarship of the German Research Foundation<br />

(Deutsche Forschungsgemeinschaft)<br />

Research Interests<br />

Financial Econometrics; Non- and Semiparametric Curve Estimation; Generalized Additive<br />

Models; Locally Stationary Time Series<br />

1

Working Papers / Work in Progress<br />

03/2011 Locally Stationary Multiplicative Volatility Modelling<br />

joint with Christopher Walsh<br />

07/2011 Nonparametric Regression for Locally Stationary Time Series<br />

08/2011 Structural Breaks and Nonlinearities in Realized Volatility<br />

joint with Enno Mammen and Matthias Fengler<br />

Seminar and Conference Presentations<br />

08/2010 European Meeting of Statisticians, University of Piraeus<br />

Locally Stationary Multiplicative Volatility Modelling<br />

11/2010 Econometrics Seminar, University of St. Gallen<br />

Structural Breaks and Nonlinearities in Realized Volatility<br />

05/2011 Econometrics Seminar, London School of Economics<br />

Nonparametric Regression for Locally Stationary Time Series<br />

06/2011 Workshop of the DFG Research Group FOR916, Mannheim<br />

Nonparametric Regression for Locally Stationary Time Series<br />

together with various seminar presentations at the University of Mannheim<br />

Teaching<br />

Fall 2008 Econometrics I<br />

Lecture for Ph.D. Students<br />

Spring 2010 Introduction to Econometrics<br />

Exercise for Bachelor Students<br />

Fall 2010 Mathematical Econometrics and Statistics<br />

Exercise for Bachelor/Master Students<br />

Spring 2011 Introduction to Econometrics<br />

Exercise for Bachelor Students<br />

Work Experience<br />

07/1999 – 07/2000 Community Service at the German Red Cross<br />

09/2006 – 03/2007 Internship at the Carl Zeiss AG, Inhouse Consulting<br />

Additional Skills<br />

Languages German (native), English (fluent), French (sound)<br />

Programming R, C, MATLAB<br />

2