Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

CAN THE US SAVE IT’S AUTO SECTOR?<br />

I S S U E 3 6 • S E P T E M B E R 2 0 0 9<br />

The rise of the<br />

collateral manager<br />

The new gold bug<br />

Trading: the impact<br />

of fragmentation<br />

Spotlight on DTCC<br />

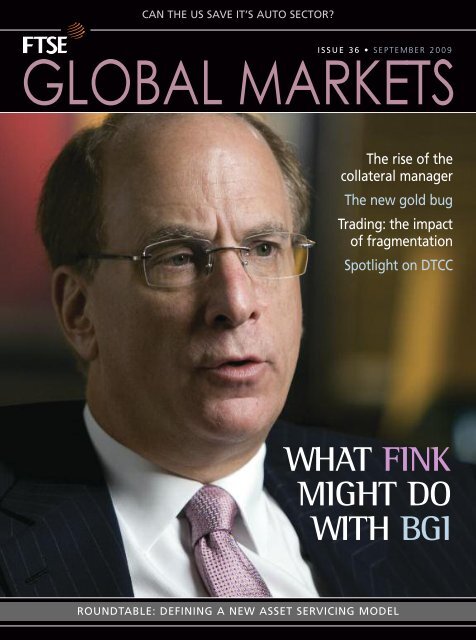

<strong>WHAT</strong> <strong>FINK</strong><br />

<strong>MIGHT</strong> <strong>DO</strong><br />

<strong>WITH</strong> <strong>BGI</strong><br />

ROUNDTABLE: DEFINING A NEW ASSET SERVICING MODEL

BNP Paribas Securities Services<br />

THE CLOSER WE ARE, THE BETTER YOU PERFORM<br />

With our precise understanding of each market’s internal workings,<br />

you maximise your market and investment opportunities.<br />

At BNP Paribas Securities Services, the closer, the better.<br />

securities.bnpparibas.com<br />

BNP Paribas Securities Services is incorporated in France with Limited Liability and authorised by the French Regulators (CECEI and AMF). BNP Paribas Trust Corporation UK<br />

Limited and Investment Fund Services Limited are authorised and regulated by the Financial Services Authority. BNP Paribas Securities Services London Branch is authorised by the<br />

CECEI and supervised by the AMF and subject to limited regulation by the Financial Services Authority. Details on the extent of our regulation by the Financial Services Authority<br />

are available from us on request. BNP Paribas Securities Services is also a member of the London Stock Exchange.

EDITORIAL DIRECTOR:<br />

Francesca Carnevale,<br />

tel: +44 [0]20 7680 5152, mob: 0795 855 5142;<br />

email: francesca@berlinguer.com,<br />

fax: +44 [0]20 7680 5155<br />

SUB EDITOR:<br />

Roy Shipston, tel: +44 [0]20 7680 5154<br />

email: roy.shipston@berlinguer.com<br />

CONTRIBUTING EDITORS:<br />

Art Detman, Neil O’Hara, David Simons.<br />

SPECIAL CORRESPONDENTS:<br />

Rodrigo Amaral (Emerging Markets); Andrew Cavenagh<br />

(Debt); Lynn Strongin Dodds (Securities Services); Vanja<br />

Dragomanovich (Commodities); Mark Faithfull (Real Estate);<br />

Ruth Hughes Liley (Trading Services, Europe); Dawn Kissi<br />

(Trading Services: Americas); John Rumsey (Latin America);<br />

Ian Williams (US/Emerging Markets/Sector Analysis); Paul<br />

Whitfield (Asset Management/Europe).<br />

<strong>FTSE</strong> EDITORIAL BOARD:<br />

Mark Makepeace (CEO); Donald Keith;<br />

Imogen Dillon-Hatcher; Paul Hoff; Andrew Buckley;<br />

Jerry Moskowitz; Andy Harvell; Sandra Steel;<br />

Nigel Henderson.<br />

PUBLISHING & SALES DIRECTOR:<br />

Paul Spendiff, tel +44 [0]20 7680 5153<br />

email: paul.spendiff@berlinguer.com<br />

EUROPEAN SALES MANAGER:<br />

Nicole Taylor, tel +44 [0]20 7680 5156<br />

email: nicole.taylor@berlinguer.com<br />

OVERSEAS REPRESENTATION:<br />

Adil Jilla (Middle East & North Africa)<br />

Faredoon Kuka, Ronni Mystry Associates Pvt (India)<br />

Leddy & Associates (United States), Can Sonmez (Turkey)<br />

PUBLISHED BY:<br />

Berlinguer Ltd, 1st Floor, Rennie House,<br />

57-60 Aldgate High Street, London EC3N 1AL<br />

Tel: +44 [0]20 7680 5151<br />

www.berlinguer.com<br />

ART DIRECTION AND PRODUCTION:<br />

Russell Smith, IntuitiveDesign, 13 North St.,<br />

Tolleshunt D’Arcy, Maldon, Essex CM9 8TF,<br />

email: russell@intuitive-design.co.uk<br />

PRINTED BY:<br />

Headley Brothers Ltd, The Invicta Press,<br />

Queens Road, Ashford, Kent TN24 8HH<br />

DISTRIBUTION:<br />

Air Business Ltd, 4 The Merlin Centre,<br />

Acrewood Way, St Albans, AL4 OJY.<br />

TO SECURE YOUR OWN SUBSCRIPTION:<br />

Please visit: www.berlinguer.com or<br />

Email: subscriptions@berlinguer.com<br />

Subscription price: £399 per annum (8 issues)<br />

<strong>FTSE</strong> Global Markets is published eight times a year. No part of this<br />

publication may be reproduced or used in any form of advertising without<br />

the express permission of Berlinguer Ltd.<br />

[Copyright © Berlinguer Ltd 2009. All rights reserved.]<br />

<strong>FTSE</strong> is a trademark of the London Stock Exchange plc and the<br />

Financial Times Limited and is used by Berlinguer Ltd under licence.<br />

<strong>FTSE</strong> International Limited would like to stress that the contents,<br />

opinions and sentiments expressed in the articles and features contained<br />

in <strong>FTSE</strong> Global Markets do not represent <strong>FTSE</strong> International Limited’s<br />

ideas and opinions. The articles are commissioned independently from<br />

<strong>FTSE</strong> International Limited and represent only the ideas and opinions of<br />

the contributing writers and editors.<br />

All information in this magazine is provided for information purposes only.<br />

Every effort is made to ensure that any and all information given in this<br />

publication is accurate, but not responsibility or liability can be accepted<br />

by <strong>FTSE</strong> International Limited and Berlinguer Ltd, for any errors, or<br />

omissions or for any loss arising from the use of this publication.<br />

All copyright and database rights in the <strong>FTSE</strong> Indices belong to <strong>FTSE</strong><br />

International Limited or Berlinguer Ltd or its licensors. Reproduction of<br />

the data comprising the <strong>FTSE</strong> indices is not permitted. You agree to<br />

comply with any restrictions or conditions imposed upon the use, access,<br />

or storage of the data as may be notified to you by <strong>FTSE</strong> International<br />

Limited, or Berlinguer Ltd and you may be required to enter into a<br />

separate agreement with <strong>FTSE</strong> International Limited and Berlinguer Ltd.<br />

ISSN: 1742-6650<br />

Journalistic code set by the Munich Declaration.<br />

F T S E G L O B A L M A R K E T S • S E P T E M B E R 2 0 0 9<br />

Outlook<br />

IT WAS INEVITABLE that in a protracted recessionary period there would<br />

be a tussle for supremacy between asset owners, fund managers and asset<br />

servicing providers in dictating terms of business. Right now there are<br />

conflicting signs as to who is winning this particular scrap.<br />

In the asset servicing segment, there are signs that providers are playing<br />

hardball. That’s because in the days before Lehman Brothers et al crashed and<br />

burned into crispy cinders, business was about volume and rarely about value.<br />

In a substantive turnaround, asset service providers are now more concerned<br />

about profit than rankings in an assets under custody league table. In<br />

consequence, their business approach has altered significantly. BNP Paribas for<br />

one has taken a blunt view: encouraging prospective clients to either put all their<br />

business through them or think again. Clients are feeling a tight pinch as a<br />

result: hence Paul Nathan, chief operating officer at Omam’s cri de cour in this<br />

issue’s asset servicing roundtable that many a firm’s star has waned in the eyes<br />

of their asset services providers just as rapidly as the net asset values of firms’<br />

investment holdings have shrunk in recent months. It is a common complaint.<br />

Equally, transition managers report that among some asset owners,<br />

particularly sovereign and quasi sovereign wealth funds, the rapidity with<br />

which underperforming asset managers are dispensed with these days means<br />

that oft times transition managers are required to temporarily house large pools<br />

of capital and provide a return to their client, until a new asset manager is<br />

selected. It’s an ill wind, say the ancients, and so some transition teams have<br />

developed some rather innovative structures for these clients to benefit from.<br />

Among these various slings, private equity principals have also been punctured<br />

by flying arrows. Witness the pain of buyout firm Nordwind Capital, which was<br />

prevented from investing in Global Fertility AG, a start up in the German fertility<br />

business, by a group of limited partners including the Harvard and Yale<br />

endowments. With some brio the limited partners pushed back against a deal by<br />

the Munich-based private equity group which had raised a €300m ($423m) debut<br />

fund back in 2004. The deal fell through after Nordwind tried to draw down funds<br />

from its investors. Some had objected to the deal because of its heavy investment<br />

in US clinics did not match Nordwind’s strategy of investing in German, Swiss and<br />

Austrian turnarounds. Others because they did not want to invest in the segment.<br />

In the end Nordwind took the costly but honourable course of backing out of the<br />

deal, so as not to technically put its investors into default.<br />

While market uncertainties continue, this unedifying scrabble looks likely to ebb<br />

and flow. However, underpinning this froth is the damned reality of continued<br />

substantial declines in asset values in key investment institutions. Look what has<br />

happened at two of America’s largest pension pots. CalSTRS is likely to report a<br />

drop in the value of its asset by as much as 25% in the fiscal year ending June 30,<br />

2009, with its market value of assets now worth $118.8bn. That much-vaunted<br />

bellwether, the California Public Employees' Retirement System (CalPERS) has<br />

reported a decline of roughly 23% for its latest fiscal year, the worst return in<br />

decades for the largest public pension fund in the US. The decline is equivalent to<br />

the loss of about $55bn in assets and while returns have improved somewhat since<br />

March, its assets remain buffeted by continued stock market turbulence, moribund<br />

credit markets and shrinking real-estate values. CalPERS is exposed to all those<br />

asset types, a fact which could ultimately impact on the firm’s credit rating.<br />

Francesca Carnevale,<br />

Editorial Director<br />

August 2009<br />

Cover photo: Laurence Fink, chairman and chief executive of global asset gatherer<br />

and manager BlackRock. Photograph kindly supplied by BlackRock, August 2009.<br />

1

2<br />

Contents<br />

COVER STORY<br />

DEPARTMENTS<br />

MARKET LEADER<br />

INDEX REVIEW<br />

IN THE MARKETS<br />

REGIONAL REVIEW<br />

FACE TO FACE<br />

COMMODITY REPORT<br />

SIBOS REPORT<br />

DATA PAGES<br />

THE IMPORTANCE OF BEING <strong>BGI</strong> ..............................................................................Page 67<br />

Laurence Fink, chairman and chief executive of BlackRock, long coveted Barclays Global<br />

Investors and its iShares family of electronically-traded funds. Now he looks to have<br />

secured it. After the deal closes later this year, BlackRock will become the world’s largest<br />

manager of investment assets. Art Detman describes why BlackRock will likely grow and<br />

thrive, and how this acquisition may affect the money-management business.<br />

CAN THE US REALLY SAVE ITS AUTO SECTOR? ..................................Page 6<br />

Ian Williams surveys the status of the US automotive landscape.<br />

TURNING JAPANESE ......................................................................................................Page 12<br />

Simon Denham, managing director, Capital Spreads, takes the bearish long view<br />

ASIAN INDEX DREAMS ................................................................................Page 14<br />

<strong>FTSE</strong> Group’s tie-in with MCX-SX and the implications for Indian investors<br />

FAST AND LOOSE <strong>WITH</strong> PRIVATE EQUITY......................................Page 16<br />

Private equity looks set to make a comeback – albeit a slow one. Neil O’Hara reports.<br />

INTEREST RATES MAKE THE RUNNING ............................................Page 24<br />

David Simons on the vagaries of interest rate management in a potentially deflationary arena<br />

RISK MANAGEMENT IN HIGH-FREQUENCY TRADING ........Page 28<br />

Dan Hubscher of Progress Apama looks at real-time risk management<br />

NORTHERN LIGHTS: THE NORDIC WAY FORWARD ..............Page 32<br />

Why Nordic markets are worth another look<br />

NEW APPROACHES TO OLD PROBLEMS ................................................Page 40<br />

Tarek Anwar, Standard Chartered, explains the new business dynamics<br />

THAT DUBAI FACTOR..................................................................................................Page 42<br />

Jeff Singer, CEO of NASDAQ Dubai, on the promise of the near east.<br />

THE GOLD BUG ................................................................................................................Page 70<br />

Vanya Dragomanovich meets Aram Shishmanian, the new CEO of the World Gold Council<br />

NEW APPROACHES TO CASH MANAGEMENT ................................Page 75<br />

Lynn Strongin Dodds reports on new approaches to money market funds<br />

THE RISE OF THE COLLATERAL MANAGER ..........................................Page 78<br />

Neil O’Hara on the rising stars in collateral management following Lehman’s demise<br />

DTCC HARNESSES A NEW WAVE OF BUSINESS ..............................Page 82<br />

David Simons reviews the DTCC’s new wave of business in clearing and settlement<br />

ASIAN DREAMS ................................................................................................................Page 86<br />

Lynn Strongin Dodds on the potential for a cross-Asian clearing and settlement platform<br />

Fidessa Fragmentation Index ......................................................................................Page 90<br />

Market Reports by <strong>FTSE</strong> Research ..............................................................................Page 92<br />

Index Calendar ..............................................................................................................Page 96<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

4<br />

Contents<br />

FEATURES<br />

REAL ESTATE<br />

AIN’T NOTHING GOING <strong>DO</strong>WN BUT THE RENT ....................Page 35<br />

The real estate market is braced for a second wave of bad news as falling occupancy and<br />

rental levels replace the capital value crisis and real economy woes begin to bite. Much<br />

of the shock generated by price falls has been absorbed but now the pressure is on lease<br />

renewals, with tenants failing, downsizing or renegotiating terms as their leases expire.<br />

Direct investment has become a case of tactical chess between buyers and sellers while<br />

diversified vehicles are finding some favour. However, as Mark Faithfull reports, new<br />

breeds of investment platforms and investors are emerging to tackle the risk conundrum<br />

TRADING REPORT<br />

THE RISE OF TRADING SUPERMARKETS..............................................Page 44<br />

The divine right of stock exchanges to “own” the trading in their own country’s stocks is<br />

going to be a thing of the past, according to Steve Grob, director of strategy, Fidessa.<br />

“Fragmentation is on an inexorable rise,” he says. “One of the assumptions in the early<br />

post-MiFID days was that fragmentation would reach a certain level and then stabilise,<br />

but every week we are seeing more fragmentation and no signs yet of consolidation of<br />

venues.” Ruth Hughes Liley reports.<br />

THE VALUE OF AGGRESSIVE PRICING....................................................Page 48<br />

LIQUIDITY ISN’T <strong>WHAT</strong> IT USED TO BE ................................................Page 50<br />

IS CONSOLIDATION THE ONLY ANSWER?..........................................Page 53<br />

Promising and offering lower latency and in some instances even free transactions,<br />

MTFs such as BATS Europe, an offspring of Kansas City-based BATS, Turquoise, a<br />

consortium-backed London-based venue and Nasdaq OMX Europe, all of which<br />

emerged one year ago, are still in business. Yet the talk of the demise of established<br />

exchanges such as the London Stock Exchange (LSE) and Frankfurt’s Deutsche Börse,<br />

has subsided with the all but near collapse of global financial markets. What role will<br />

technology play in determining the winners and the losers in the fragmented trading<br />

landscape? Dawn Kissi reports.<br />

ASSET SERVICING<br />

TOWARDS A NEW ASSET SERVICING MODEL ........................Page 57<br />

According to Luc Leclercq, operations and IT director at Foreign & Colonial: “The<br />

landscape has certainly changed over the last 18 months, due in large part to changes in<br />

the segments of credit, counterparties, clients, regulators, cost, trustees, and control.<br />

Additionally, clients are becoming much more concerned about a relative performance<br />

into an absolute world, given the fact that last year we have seen quite a lot of people<br />

who lost money. The resulting paradigm shift has been quite enormous: moving from a<br />

relative world into an absolute world; from what was understood to be safe to what is<br />

not. Certainly, nothing will be taken at face value any more.” What now then for asset<br />

service providers? Our roundtable discussion gives some important pointers<br />

DEBT REPORT<br />

CORPORATE DEBT: AN OPTIMISTIC OUTLOOK? ....................Page 73<br />

While credit fundamentals remain challenging for companies looking to crawl out from<br />

under the leverage wreckage, a mid-summer string of positive earnings reports has<br />

helped buoy the corporate bond markets, which have achieved a level of normalcy not<br />

seen since the pre-Lehman days. Dave Simons reports from Boston<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

US AUTO SECTOR: CAN IT BE SAVED?<br />

6<br />

Market Leader<br />

Chrysler, Ford and General<br />

Motors, the iconic Big Three<br />

automakers, account for just<br />

over half of all light vehicle<br />

production and slightly less<br />

than half of all light vehicle<br />

sales in the United States. Even<br />

so, they are in dire straits. The<br />

rest of the US auto industry—<br />

which includes Honda, Toyota,<br />

Nissan, Hyundai, BMW, and<br />

other foreign nameplate<br />

producers—have been making<br />

more products that Americans<br />

want to buy and will endure<br />

this recession without<br />

subsidies because they have<br />

more efficient cost structures.<br />

So why is the US government<br />

so intent on ploughing $25bn<br />

into the US auto majors? Ian<br />

Williams reports.<br />

CLUNKING SUBSIDIES<br />

MANY PEOPLE REMEMBER<br />

US president George HW<br />

Bush being sick over the leg of<br />

the Japanese premier Kiichi Miyazawa.<br />

Few, however, recall the occasion.<br />

President Bush was in Tokyo with the<br />

chiefs of the BigThree US automakers to<br />

plead for self-restraint from the<br />

Japanese auto manufacturers, which<br />

were roundly beating Detroit on its<br />

home turf. Robert Monks, of Lens<br />

Governance Advisors, a long-time<br />

scourge of auto executives, sees it as an<br />

iconic incident; the writing on the wall<br />

for potential investors in the Big Three:<br />

“There still isn’t full appreciation of how<br />

the Big Three have been subsidised and<br />

protected by the Federal political<br />

establishment—in both parties.”<br />

Monks points to Congressman John<br />

Dingell, the dean of the House of<br />

Representatives, who, he claims, has<br />

United States Department of Energy Secretary Steven Chu (right) talks with Ford Motor<br />

Company chief executive officer Alan Mulally during a news conference in Dearborn, Michigan,<br />

on Tuesday, 23rd June 2009. Chu announced the Energy Department will lend $5.9bn to Ford<br />

and provide about $2.1bn in loans to Nissan Motor Company and Tesla Motors Inc., making<br />

the three automakers the first beneficiaries of a $25bn fund to develop fuel-efficient vehicles.<br />

Photograph by Paul Sancya for Associated Press, supplied by PA Photos, August 2009.<br />

helped at every stage to perpetuate US<br />

automakers’ inefficiencies, “whether it<br />

was stalling fuel efficiency measures or<br />

emission reduction rules”. Monks adds:<br />

“For years, almost the only people who<br />

bought American cars were the<br />

government and rental agencies—<br />

which were owned by the makers.Then<br />

they had to sell the car-hire companies<br />

and so people rented Toyotas. In the<br />

end they were destroyed by incest, as<br />

their ultra-cosy relationship with<br />

government protected their<br />

inefficiency. Talk about unions, legacy<br />

costs? It was just a fig leaf to cover bad<br />

managing and bad engineering.”<br />

It was far easier to hire lobbyists in<br />

Washington than to engineer lower<br />

emissions or more fuel efficiency. For<br />

decades, industry lobbyists<br />

successfully resisted stiffer Corporate<br />

Average Fuel Economy (CAFE)<br />

standards for sedans and managed a<br />

complete runaround them anyway by<br />

getting tax breaks and complete<br />

exemptions for the SUV (Sport Utility<br />

Vehicles)—which are essentially<br />

heavy, lumbering trucks disguised as<br />

passenger vehicles. Detroit made<br />

much more money on the latter until<br />

rising oil prices brought them down to<br />

earth with a thump as heavy as the<br />

lead which, incidentally, they had also<br />

resisted removing from fuel.<br />

Consequently, in 2008 the Big Three<br />

fell below 50% market share for the<br />

first time in living memory, to 47.4%,<br />

losing primacy to imports and foreign<br />

transplants. Moreover, for the first<br />

time in almost a decade,“light truck”<br />

sales last year fell below the sales of<br />

higher miles per gallon (mpg) sedans,<br />

on which the US industry had all but<br />

given up. The credit crunch caused US<br />

sales to drop from 15 million vehicles<br />

a year to 9.5 million as the financial<br />

crisis dried up liquidity for consumers<br />

and companies alike.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

US AUTO SECTOR: CAN IT BE SAVED?<br />

8<br />

Market Leader<br />

As July drew to a close,Washington had<br />

to add another $2bn to the oversubscribed<br />

billion dollar“Cash for Clunkers”scheme<br />

that had offered $4,500 for Americans<br />

trading in their old gas-guzzlers for more<br />

efficient models. It was small beer in<br />

proportion to the $80bn industry rescue<br />

package, though perhaps symbolic that<br />

the scheme appears to benefit the<br />

environment more than Detroit.<br />

As consumers traded in old, mostly<br />

US-made gas-guzzlers for new efficient<br />

cars, foreign companies (notably<br />

Hyundai) were major beneficiaries of<br />

the programme along with Ford, which<br />

recorded its first increase in sales in two<br />

years. Hyundai this July reported record<br />

quarterly profits.<br />

Long-time industry consultant<br />

Professor Barry Bluestone at Boston’s<br />

Northeastern University last year<br />

pointed out the stark realities in a<br />

memo to Representative Barney Frank,<br />

a key legislator in the Federal rescue<br />

programme for the industry. Using the<br />

oft-cited but, in Detroit, much-ignored<br />

market to make his case, he invokes the<br />

second-hand value of comparable 2003<br />

model cars. “In late 2008, the Toyota<br />

Camry V6 had a Vehix.com value of<br />

$11,150 while a comparably-powered<br />

Honda Accord V6 is slightly higher at<br />

$11,225. In contrast, the trade-in values<br />

of the Chevrolet Impala V6 was only<br />

$6,850; the Chrysler Stratus $6,200, and<br />

the Ford Taurus $5,000.”<br />

Bluestone cites similar devastating<br />

figures from Consumer Reports for<br />

2008 that show Big Three brands came<br />

in below 50 on the 0-100 satisfaction<br />

scale while the equivalent “import<br />

brand” models, as Detroit labels even<br />

US-built vehicles by foreign companies,<br />

won scores of 70s and even 80s. He<br />

concludes: “Automakers that provide<br />

their customers with quality that lasts,<br />

with a satisfying driving experience and<br />

a vehicle that meets their driving<br />

expectations, will make a profit and will<br />

not need Federal support.”<br />

Bluestone recalls other missed<br />

opportunities. Around the time that<br />

Bush Senior was recycling his dinner<br />

menu in Japan, General Motors had<br />

tried to move forward with the Saturn,<br />

using the techniques that were<br />

propelling Japanese success. However,<br />

the good efforts came to little.<br />

No one now pretends that what’s<br />

good for General Motors is good for<br />

America. The contumely that greeted<br />

the Big Three executives in<br />

Washington when they turned up last<br />

year (cap in hand and on executive<br />

jets) marked the end of an era.<br />

Political shift<br />

There has also been a political shift. As<br />

the Republican Party has become<br />

more intensely ideological, Detroit,<br />

with unions and workers“pampered”<br />

with health insurance, lay-off pay and<br />

pensions, looked dangerously<br />

“socialist” (an almost insulting jibe in<br />

US political circles) compared with the<br />

foreign transplants that had taken<br />

root in the Republican-voting<br />

Southern states with laws hostile to<br />

unionisation. That allowed the<br />

discussion to become obsessed and<br />

obscured by Monks’ “fig leaf,” the<br />

costs of union labour. In fact, there<br />

already was a convergence between<br />

labour costs in the old United Auto<br />

Workers (UAW) plants and the<br />

transplants, which suggests that it was<br />

not so much the cost of labour but,<br />

according to some analysts, the low<br />

quality of management and design<br />

that wasted the skills of the workforce.<br />

In fact, Professor Bluestone points out<br />

that many of the “import brand”<br />

transplants have had very successful<br />

union working agreements, and cites<br />

the Modern Operating Agreement of<br />

the Mazda plant in Michigan, theToyota<br />

plant in California—and, significantly,<br />

the Ford plant in Cleveland, significant<br />

because, of all the US companies, Ford<br />

has weathered the crisis best.<br />

In the face of Republican<br />

indifference and taxpayer revolt in the<br />

aftermath of banking bailouts, Detroit<br />

had to suffer tough love from<br />

Washington legislators who had<br />

previously been the political<br />

equivalent of a pushover. Congress<br />

forced it to commit to all the steps<br />

that it had helped them avert for all<br />

those decades.<br />

Washington acted quickly, allowing<br />

accelerated bankruptcy proceedings,<br />

helping shed many liabilities while<br />

backing-up corporate guarantees on<br />

vehicles, thus stopping even more<br />

precipitous erosion of the consumer<br />

base. Additionally, the industry had<br />

accelerated its long-procrastinated<br />

reforms with mandated cuts in staff,<br />

plants, marques, dealerships<br />

remuneration, an end to dividends,<br />

and with directives to invest in newer,<br />

more efficient models.<br />

Notably missing from the dole queue<br />

was Ford, which, Jack Plunkett of the<br />

annual Plunkett’s Automobile Industry<br />

Almanac points out, had “brought in a<br />

brilliant outsider”, former Boeing<br />

Commercial president Allan Mulally, to<br />

be president and chief executive officer,<br />

and so was in the right position to meet<br />

the crisis, amassing huge amounts of<br />

cash, creating efficiencies across the<br />

board, standardising designs and<br />

components across the product range.<br />

It had negotiated new union<br />

contracts, which reduced the labour<br />

force and cut wages and benefits for<br />

new employees. It cut its 97 marques to<br />

a manageable 20 or less. As a result,<br />

Ford could refuse offers of government<br />

money but did ask for a line of credit<br />

guarantee to maintain sales. In contrast<br />

with its beleaguered compatriot firms,<br />

it recorded a second-quarter $2.3bn<br />

net profit. However, even if Ford was<br />

prepared to bounce off the rocks that<br />

almost crushed GM and Chrysler, it is<br />

still in a hard place: the faltering global<br />

and US economy.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

The financial information<br />

you need when you need<br />

it. Because there’s no<br />

pause button in business.<br />

Considering the current economic environment, staying on top of your business and managing your risk has never<br />

been more important. At Northern Trust, we offer one global, seamless technology platform designed to provide<br />

consistent, accurate and timely information — enabling you to be as efficient as possible. That’s why we were<br />

named one of the Top 100 Technology Innovators.* For more information, visit northerntrust.com/pausebutton<br />

or call Tim Theriault at 1-866-803-5857.<br />

Asset Servicing | Asset Management | Wealth Management<br />

© 2009 Northern Trust Corporation, 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the United States.<br />

*Information Week

US AUTO SECTOR: CAN IT BE SAVED?<br />

10<br />

Market Leader<br />

Plunkett commiserates that the<br />

“global auto industry has been<br />

evolving out of control, with massive<br />

overcapacity, but in the European<br />

Union and US it hasn’t really evolved<br />

to take advantage of the market.<br />

Toyota has been able to give the<br />

customers an SUV with low petrol<br />

consumption as the US carried on<br />

making the big Chevrolet Tahoe and<br />

Hummer, while Hyundai’s quality is<br />

outstanding.”He concludes that “even<br />

if the financial crisis had not<br />

happened, there was still an auto crisis<br />

in the making”.<br />

So is there any light at the end of<br />

this very gloomy tunnel for US<br />

automakers in a world with global<br />

overcapacity, a credit squeeze, rising<br />

unemployment—and more efficient<br />

competition at home and abroad?<br />

Actually, there is. Professor John Paul<br />

MacDuffie and his colleagues at the<br />

International Motor Vehicle Program<br />

(IMVP) argue that demand will return<br />

to near-complete levels in the<br />

developed world and in particular in<br />

the US, and even without “Cash for<br />

Clunkers” four million more cars a<br />

year hit the scrapheap than are being<br />

sold, so upwards is the only way.<br />

The $64,000 question is: how many<br />

of those vehicles will Detroit make?<br />

The answer is, almost inevitably, many<br />

fewer. Slimmed down as they will be,<br />

with fewer models, many fewer dealers<br />

and without the credit to offer the cutthroat<br />

incentives and discounts they<br />

have used to maintain sales, there are<br />

few grounds for great expectations. It<br />

will take time for them to tool up to<br />

build their new, efficient models with<br />

their new, cheaper workforce.<br />

Indeed, their fire sale of overseas<br />

assets may be assisting yet another<br />

rival just over the horizon. Chinese<br />

companies are hovering around and<br />

make little secret that they want the<br />

technology as much as the physical<br />

assets. Ironically, GM is very<br />

successful in China, but Plunkett<br />

points out: “The Chinese are<br />

developing some impressive<br />

technologies, and as soon as<br />

American consumers decide they trust<br />

the quality and like the styling of<br />

Chinese models (which is based on<br />

US cars anyway) they will buy.”<br />

There is only a narrow window of<br />

opportunity for the US companies to<br />

turn themselves around before<br />

taxpayer indulgence attenuates, the<br />

market revives and their rivals move<br />

into the vacuum the Big Three’s nearcollapse<br />

created. The one step<br />

Congress could take that would<br />

allow—or rather force—the US<br />

industry to compete, Plunkett<br />

suggests, is what Big Three executives<br />

also seem to favour: that is to<br />

incrementally increase fuel prices to<br />

developed world levels to force<br />

efficiencies and confirm a market for<br />

the low-emission, high efficiency<br />

vehicles they are now committed to<br />

build as a condition for the Federal<br />

aid. He points out: “The CAFE fleet<br />

standards are just absurd, an evadable<br />

abyss of regulation. The intelligent<br />

way to control fuel use is price: I wish<br />

Congress were that smart.”<br />

Massive savings<br />

Sadly, Capitol Hill, which only<br />

occasionally exhibits courage, is<br />

unlikely to increase the cost of fuel in<br />

the face of combined consumer and<br />

oil company resistance which may<br />

thwart the industry’s belatedly<br />

adopted reforms. Detroit’s reforms<br />

were predicted to offer massive<br />

savings (in 2010). Already, for<br />

example, GM’s hourly manufacturing<br />

costs have dropped from $18.4bn in<br />

2003 to an estimated $8.1bn in 2008,<br />

somewhere around 10% of the cost<br />

per car.<br />

The IMVP echoes Bluestone that all<br />

three US automakers now have some<br />

sites that are “true knowledge-driven<br />

workplaces, delivering world-class<br />

performance on safety, quality, cost,<br />

and other indicators,” while Ford’s<br />

resilience and those Modern<br />

Operating Agreement plants shows<br />

what can be done. The question is<br />

whether those examples can be<br />

replicated at GM and Chrysler and<br />

whether managerial conservatism and<br />

the credit squeeze will allow<br />

investment in new, and sellable,<br />

technologies.<br />

The dangers are that they only learn<br />

half the model. While Toyota, for<br />

example, is keeping redundant<br />

workers on the books of its California<br />

truck plant to maintain their skill base<br />

for the upturn, Detroit’s rush to shed<br />

workers on the older union contracts<br />

to hire novices may be pithing its<br />

technological abilities. Professor<br />

James Jacobs of Macomb College in<br />

Michigan points out: “Any future of<br />

the auto industry rests upon highlyskilled<br />

workers willing to be flexible.<br />

But will such workers be attracted to<br />

the auto industry when wages are<br />

being lowered? Currently, nursing<br />

assistants get $9 to $50 per hour, while<br />

starting wages in auto-unionised jobs<br />

are not much more at $14 to $50.”<br />

Similar traditional short-termism<br />

may inhibit the industry’s preparation<br />

for an upturn. Indeed, the crisis effect<br />

on industry liquidity has already<br />

postponed the launch of several fuelefficient<br />

vehicles such as GM’sVolt and<br />

Cruze, while US carmakers have been<br />

reluctant to adapt clean-diesel<br />

engines, which account for half of<br />

sales in Europe. In the end, there is a<br />

real-time experiment. The transplant<br />

companies have shown there is<br />

nothing inherently untenable about<br />

making desirable and profitable<br />

vehicles in the US, even in unionised<br />

plants. In the wake of the crisis,<br />

Detroit’s management has no more<br />

excuses left. It would be a bold investor<br />

though who bought stock in them.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

IN ONLINE TRADING<br />

EVERY SECOND COUNTS<br />

SWITCH YOUR ONLINE TRADING BUSINESS INTO TOP GEAR<br />

SAXO BANK OFFERS:<br />

Award-winning technology<br />

Real-time and multi-asset risk<br />

management<br />

Tier-1 liquidity<br />

Competitive pricing<br />

Automated settlement<br />

Post-trade service<br />

SPEED OF EXECUTION, LIQUIDITY, RISK-MANAGEMENT, MULTI-ASSET<br />

With our state-of-the-art institutional trading g solution hundreds of financial institutions around the globe g turn market<br />

opportunities opportunities into innto<br />

profit.<br />

Saxo Bank’ Bank’s s advanced<br />

trading trading<br />

technology<br />

provides<br />

superior speed<br />

of execution, deep Tier-1<br />

liquidity, liquiddity,<br />

competitive pricing, pric priccing<br />

cing, broad br oad product pr oduct coverage on FX, FX FXX<br />

X, FX Options, Options Options, CFDs, CFDs CFDs, Futures, Futur Futures<br />

es, Stocks s and ETFs coupled with real-time r real-time<br />

eal time cross- cr oss<br />

product,<br />

risk mmanagement.<br />

anagement.<br />

Our award-winning<br />

trading solution supported by<br />

automated<br />

settlement,<br />

post-trade services<br />

and advanced reporting<br />

systems syste ems<br />

allows our institutional instittutional<br />

clients clients to focus on what what really<br />

matters – growing<br />

their online institutional insstitutional<br />

trading business.<br />

Contact our global offices for more<br />

information. informmation.<br />

VVisit<br />

isit www www.saxobank.com<br />

.saxobank.c com<br />

Andy Schleck,<br />

Team Saxo Bank

AVOIDING THE WORST EFFECTS OF DEFLATION<br />

12<br />

Index Review<br />

The summer is drawing to a close and markets have continued to<br />

be reasonably friendly with the <strong>FTSE</strong> nestling comfortably<br />

around 4700 and the various economic data releases giving hope<br />

that the worst of the current downturn might now be over. The<br />

fact that the German and French economies grew in the second<br />

quarter came as something of a surprise to the markets, though<br />

this might have more to do with the very high levels of personal<br />

state aid available in both nations than with an actual<br />

turnaround in the economy. Simon Denham, managing director<br />

of spread betting firm Capital Spreads, calls the odds.<br />

IN THE UNITED Kingdom the vast<br />

sums added via banking support,<br />

quantitative easing and general<br />

state spending seem to be holding<br />

back the worst (for the time being) but<br />

it must be admitted that the general<br />

outlook once the purse strings start to<br />

be tightened is rather harder to<br />

estimate. Economists seem to fall into<br />

two camps, with the apocalyptic<br />

grabbing the headlines and the more<br />

generally neutral bringing up the rear;<br />

after all, middle of the road forecasts<br />

do not make for good copy. Inflation<br />

in the US and Europe, or rather<br />

deflation, is causing considerable<br />

concerns, especially as the massive<br />

increase in money supply would<br />

normally have been expected to have<br />

the opposite effect—especially across<br />

the Atlantic. One wonders what the<br />

CPI number in the States (currently<br />

-2.1%) would have been had the Fed<br />

not spent the trillion plus dollars on<br />

its various policy initiatives over the<br />

last year.<br />

Europe meanwhile (when<br />

compared to the UK and US) has, in<br />

the main, kept its powder dry. The<br />

economies are not so heavily<br />

weighted towards the service sector<br />

and levels of personal debt are way<br />

below those prevalent in the Anglo<br />

Saxon economies. Their capacity to<br />

maintain domestic demand levels<br />

without state aid has therefore been<br />

that much greater. If growth in the<br />

West flags once again eyes will be<br />

turned rather more aggressively on<br />

the Northern European Bloc to open<br />

the floodgates to aid expansion.<br />

Above everything is the fear of the<br />

“ghost at the feast”. Japan’s lost<br />

decade (actually nearer two decades<br />

now) is a spectre that nobody wants to<br />

contemplate, though for high inflation,<br />

high personal expenditure, nations<br />

such as the UK it has always seemed<br />

most unlikely. Even with the vast sums<br />

being expended, the sad fact is that the<br />

money supply data is still falling (M4<br />

growth in the UK is now dipping<br />

sharply) as banks retrench into their<br />

domestic economies.<br />

Japan has shown that even extreme<br />

levels of state funding can have little<br />

impact once the effects of deflation<br />

become endemic. Japan’s public debt<br />

is now 200% of GDP but nobody<br />

seriously expects hyper-inflation to<br />

rear its head in the land of the rising<br />

sun. In fact the deflationary aspect of<br />

Japan’s economy means the real value<br />

of its debt keeps increasing year on<br />

year. In Europe we have become used<br />

to governments inflating their way out<br />

of a poor debt situation (if inflation is<br />

5% then the absolute value of<br />

Simon Denham, managing director of spread<br />

betting firm, Capital Spreads, October 2008.<br />

TURNING JAPANESE?<br />

£1,000,000 debt is just £950,000 next<br />

year, £902,500 the next, etc). Imagine<br />

the effect of consumer confidence and<br />

expenditure if personal debts<br />

(mortgages, credit cards, etc) were<br />

greater in terms of salary and income<br />

next year even though they had not<br />

increased at all. Actually we do not<br />

need to imagine as we have the case<br />

study of the effect in Japan to show us.<br />

The weak pound means inflation<br />

has continued in positive territory in<br />

the UK but the recent strength of<br />

sterling means that this effect is being<br />

whittled away. By mid-October, if the<br />

pound remains where it is now,<br />

inflationary impulses will have largely<br />

worked its way through the system.<br />

Compounding this export growth has<br />

been in fact export contraction and the<br />

trade balance has fallen as import<br />

levels have reduced even further.<br />

If entrenched deflation takes a hand,<br />

investors will experience the Japanese<br />

effect of waning stock valuations.<br />

However, if inflation spirals out of<br />

control, rates will have to be hiked and<br />

money and bonds may well regain<br />

their attraction over equities. A<br />

continuation of the current equity rally<br />

will rely on reasonable, noninflationary<br />

growth, but this is a rather<br />

narrow path to tread. As ever ladies<br />

and gentlemen, place your bets.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

The Depository Trust & Clearing<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

nancial companies can now join DTCC’s<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

NEW YORK, March 4, 2009<br />

<br />

<br />

<br />

<br />

<br />

<br />

To find out more about non-U.S. membership in FICC,<br />

contact us by phone at +1.212.855.1207 or by email at pkelly@dtcc.com<br />

Miss This<br />

Story?<br />

Well, Don’t Miss the Opportunity!<br />

The Logical Solutions Provider<br />

www.dtcc.com

<strong>FTSE</strong> GROUP TIE UP <strong>WITH</strong> MCX-SX<br />

14<br />

Index Review<br />

Index provider <strong>FTSE</strong> Group is developing and refining its<br />

approaches to emerging markets investing through innovative<br />

agreements with established and emerging stock exchanges and<br />

trading venues in a move to create both investible products and<br />

investment benchmarks in selected countries. Following on from its<br />

extensive agreements and ventures with the JSE in South Africa,<br />

<strong>FTSE</strong> Group has tied up with India’s MCX Stock Exchange (MCX-SX),<br />

to create new investment products for investors in the Indian subcontinent,<br />

which are based around indices and investment<br />

benchmarks and which will be listed and traded on the Indian<br />

exchange. <strong>FTSE</strong> will also extend co-operation to MCX-SX parent<br />

Financial Technologies Group’s exchange network in India,<br />

Singapore and Bahrain, and facilitate creation of international<br />

investment products to be listed on the MCX Stock Exchange.<br />

DEEPENING THE<br />

INVESTMENT MIX<br />

UP TO NOW, the Bombay Stock<br />

Exchange’s (BSE’s) Sensex and<br />

the National Stock Exchange<br />

(NSE) Nifty indices have dominated<br />

the Indian domestic equity markets.<br />

Global index provider <strong>FTSE</strong> Group<br />

instead chose to work with MCX-SX,<br />

a relatively new six-year-old exchange<br />

active in currency trading. Under the<br />

terms of the agreement, MCX-SX and<br />

<strong>FTSE</strong> will work together to create new<br />

domestic index products for India, as<br />

well as bring a set of international<br />

<strong>FTSE</strong> indices to MCX-SX, which will<br />

facilitate the creation of international<br />

investment products, including index<br />

futures, exchange traded funds and<br />

cash-based products, to be listed on<br />

the MCX-SX in India, after<br />

completion of regulatory compliances.<br />

By combining <strong>FTSE</strong>’s indexing<br />

heritage with MCX-SX’s deep local<br />

knowledge, both organisations are<br />

confident. “We can add value to<br />

international and domestic investors<br />

seeking to capture the investment<br />

opportunities in India’s markets,” says<br />

Donald Keith, <strong>FTSE</strong> Group’s deputy<br />

chief executive. “Our interest in India<br />

goes back some years, though we<br />

realised that to gain meaningful access<br />

and build a position in the market we<br />

needed a partner. MCX-SX think there<br />

is room to compete with both the BSE<br />

and NSE and I think they are right.<br />

India is still relatively underdeveloped<br />

from an index point of view.” The<br />

venture will begin market research to<br />

conduct a wide market consultation<br />

over the requirements for a new<br />

domestic index, says Keith, “and we<br />

hope to have something ready for<br />

investors by the end of this year”.<br />

According to Joseph Massey,<br />

managing director and chief executive<br />

officer of MCX-SX, the partners will<br />

“jointly design and introduce a range<br />

of indices which will meet the needs of<br />

the market participants. These indices<br />

will allow the market participants to<br />

take a view on global growth, manage<br />

sectoral as well as global risks. We are<br />

delighted to be working with <strong>FTSE</strong> on<br />

this important development. Through<br />

our deep domain knowledge of Indian<br />

financial markets and <strong>FTSE</strong>’s expertise<br />

Donald Keith, deputy chief executive, <strong>FTSE</strong><br />

Group. Photograph kindly supplied by <strong>FTSE</strong><br />

Group, August 2009.<br />

in creating global indices, we aim to<br />

help Indian investors make informed<br />

decisions through efficient and global<br />

benchmarked products.”<br />

The venture’s goal is to bring a broad<br />

range of domestic and international<br />

index products to the Indian financial<br />

services sector, which can then be used<br />

as performance benchmarks and as a<br />

basis for financial products such as<br />

institutional and retail funds, exchange<br />

traded funds, and derivative contracts.<br />

Going forward, <strong>FTSE</strong> and MCX-SX will<br />

agree to create a set of <strong>FTSE</strong> global<br />

indices which will be licensed to become<br />

the basis for futures contracts on MCX-<br />

SX in India subject to regulatory<br />

clearances. The partnership will also<br />

create a new jointly developed index<br />

series which will offer domestic as well<br />

as global investors new opportunities to<br />

“track, analyse and invest in India’s<br />

dynamic financial markets,”says Keith.<br />

MCX-SX already provides a highliquidity<br />

platform for hedging against<br />

the effects of unfavourable fluctuations<br />

in foreign exchange rates. Banks,<br />

importers, exporters and corporates can<br />

hedge on MCX-SX at low entry and exit<br />

costs. The exchange is now awaiting<br />

regulatory approval to commence equity<br />

trading. According to Keith:“MCX-SX is<br />

the right partner. The exchange has a<br />

long-term strategy, good technology<br />

and is poised for better growth. Today’s<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

co-operation announcement<br />

marks an important step towards<br />

establishing <strong>FTSE</strong> in India, the<br />

world’s fastest-growing market,<br />

after China.”<br />

MCX-SX is a subsidiary of Multi<br />

Commodity Exchange of India Ltd<br />

(MCX), part of the Financial<br />

Technologies Group owned by<br />

Jignesh Shah, and operates under<br />

the regulatory framework of the<br />

Securities and Exchange Board of<br />

India (SEBI) and Reserve Bank of<br />

India (RBI). MCX-SX was<br />

inaugurated on 6th October 2008<br />

and went live the next day.<br />

According to Keith, MCX ranked<br />

among the world top 10<br />

commodity futures exchange in<br />

2007 and ranks number one in<br />

silver, number two in natural gas,<br />

and three in gold, crude oil and<br />

copper futures trading globally.<br />

MCX has helped redefine the<br />

Indian commodity market and is<br />

among the fastest growing<br />

exchanges in the world, boasting<br />

strategic alliances with NYMEX, the<br />

London Metals Exchange,<br />

TOCOM, NYSE Euronext, CCX,<br />

SHFE, and others.<br />

As a 51% stakeholder in MCX-<br />

SX, MCX will add value to the<br />

business of MCX-SX by bringing in<br />

the actual users of commodities to<br />

hedge their currency exposure on<br />

MCX-SX’s nationwide electronic<br />

trading platform. For its part,<br />

Financial Technologies Group is the<br />

promoter of nine other commodity<br />

and financial exchanges—six in<br />

India including Multi Commodity<br />

Exchange of India and three outside<br />

India, including the Dubai Gold<br />

and Commodities Exchange, The<br />

Singapore Mercantile Exchange<br />

and the Global Board of Trade,<br />

Mauritius and Bourse Africa.<br />

The venture builds on <strong>FTSE</strong>’s<br />

experience in partnering with<br />

F T S E G L O B A L M A R K E T S • S E P T E M B E R 2 0 0 9<br />

stock exchanges globally to<br />

design and calculate a range of<br />

domestic, as well as global,<br />

indices.These exchanges include<br />

Singapore, Malaysia, Thailand,<br />

Johannesburg, Italy and<br />

London. Equally, the index<br />

provider is keen to get a foothold<br />

into the relatively prosperous<br />

Indian market. According to last<br />

year’s International Monetary<br />

Fund (IMF) economic outlook,<br />

the Indian economy, though<br />

stymied by the global financial<br />

crisis, is still expected to put in<br />

growth by some 6.9% this year,<br />

though it is still down on the<br />

peak of 9.3% registered in 2007.<br />

“There are limits, however, on<br />

how much Indian investors can<br />

invest overseas. That is why part<br />

of the plan is to bring a range of<br />

products to the Indian market,<br />

listed in India and based on<br />

<strong>FTSE</strong> Indices created globally,<br />

thereby precluding Indian<br />

investors of the need to go<br />

overseas,”explains Keith.<br />

<strong>FTSE</strong> is also expanding its<br />

products and partnerships in the<br />

wider Australasian region to<br />

include the <strong>FTSE</strong> Australia Index<br />

Series—designed to address<br />

Australia’s unique tax application.<br />

Other recent initiatives include a<br />

new <strong>FTSE</strong> Currency Forward Rate<br />

Bias Index Series as well as the<br />

<strong>FTSE</strong> Environmental Markets<br />

Classification System and the<br />

extension to the <strong>FTSE</strong><br />

Environmental Opportunities<br />

Index Series. However, the Asian<br />

continent remains key for <strong>FTSE</strong><br />

Group, acknowledges Keith, who<br />

points to a number of new index<br />

based initiatives, with the Bursa<br />

Malaysia and the Singapore Stock<br />

Exchange which have involved<br />

upgrades to each market’s<br />

respective benchmark indices.<br />

www.munier-bbn.com<br />

... and climbing.<br />

A global player<br />

in asset servicing...<br />

Oering leading value in<br />

investor services demands<br />

constant evolution.<br />

At CACEIS, our strategy of<br />

sustained growth is helping<br />

customers meet competitive<br />

challenges on a global scale.<br />

Find out how our highly<br />

adapted investor services can<br />

keep you a leap ahead.<br />

CACEIS, your comprehensive<br />

securities servicing partner.<br />

Custody-Depositary / Trustee<br />

Fund Administration<br />

Corporate Trust<br />

CACEIS benefits from an S&P AA- rating<br />

www.caceis.com<br />

15

PRIVATE EQUITY: IMPROVING OUTLOOK<br />

16<br />

In the Markets<br />

EVERY WHICH<br />

WAY BUT LOOSE<br />

Undoubtedly private equity is a tough place to be these days.<br />

However, despite the current difficulties, most private equity<br />

professionals expect conditions to improve towards the end of<br />

2010. According to Brian Livingston, head of private equity at<br />

Smith & Williamson, the accountancy and financial services firm in<br />

the United Kingdom: “The debt-fuelled frenzy is over, and financial<br />

engineering can no longer be relied on to generate equity returns.<br />

Private equity will have to go back to fundamentals—<br />

concentrating on old fashioned, solid businesses with strong<br />

management in attractive sectors. With returns based on business,<br />

rather than banking, we see a further move to more realistic<br />

pricing … Some have claimed that the private equity market is<br />

dead. The love affair with debt may be over but private equity will<br />

survive and adapt—this is the age of equity investment.” Is<br />

Livingstone right? Neil O’Hara assesses the industry outlook.<br />

Photograph supplied by<br />

istockphotos.com, supplied<br />

August 2009.<br />

PRIVATE EQUITY INVESTORS<br />

worldwide expect 10% of<br />

limited partners to default on<br />

their capital commitments in the next<br />

two years, according to a summer<br />

2009 survey conducted by Coller<br />

Capital, a boutique securities house<br />

based in London that specialises in<br />

secondary transactions in private<br />

equity interests. Investors in the<br />

United States are even more<br />

pessimistic: they expect a 13% default<br />

rate. The potential shortfall exceeds<br />

$80bn in the US alone, where private<br />

equity firms raised an aggregate<br />

$630bn in 2007 and 2008. Although<br />

many investors ended up overexposed<br />

to private equity after the market<br />

meltdown (which played havoc with<br />

target asset allocations) they haven’t<br />

yet defaulted in droves—and may<br />

never do so.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

PRIVATE EQUITY: IMPROVING OUTLOOK<br />

18<br />

In the Markets<br />

Christian Oberbeck, a founding partner of Saratoga Partners, a New York-based private equity<br />

firm that manages $250m. Oberbeck says: “All of a sudden you stop getting liquidity flows<br />

from prior investments …You have to tap into other investments in the rest of the portfolio to<br />

fund the call.” Photograph kindly supplied by Saratoga Partners, August 2009.<br />

Serial investors in private equity<br />

have undrawn commitments to newer<br />

funds while older ones throw off cash<br />

as the sponsor liquidates successful<br />

investments; in effect, returns from<br />

older funds provide a significant<br />

portion of the cash needed to finance<br />

future commitments. The amount<br />

invested at any one time may be no<br />

more than 50%-60% of the nominal<br />

exposure, so investors often sign up<br />

for higher commitments to keep the<br />

average amount invested close to their<br />

goal. The market crash eliminated the<br />

customary exit strategies for fund<br />

sponsors. However, it decimated<br />

merger activity, undermined the<br />

economics of recapitalisations and<br />

shut down initial public offerings<br />

altogether. Investors who have no<br />

cash coming in but still have to fund<br />

capital calls are now struggling to<br />

meet their obligations. “All of a<br />

sudden you stop getting liquidity<br />

flows from prior investments,” says<br />

Christian Oberbeck, a founding<br />

partner of Saratoga Partners, a New<br />

York-based private equity firm that<br />

manages $250m.“You have to tap into<br />

other investments in the rest of the<br />

portfolio to fund the call.”<br />

Suppose a $1bn pension fund had<br />

10% committed to private equity<br />

before the crash; if the portfolio also<br />

included $500m in equities whose<br />

value tumbled 50%, it became a $750m<br />

fund—and the $100m in private equity<br />

represents 13.3%, way above target.<br />

For high net worth individuals who<br />

used leverage to fund their private<br />

equity commitments, allocations got<br />

even more out of whack.<br />

Relations between private equity<br />

firms and their investors could turn<br />

ugly if limited partners do start to<br />

default. In early March, CapGen, a<br />

New York-based private equity shop,<br />

filed a complaint in Delaware<br />

`<br />

Relations between<br />

private equity firms and<br />

their investors could turn<br />

ugly if limited partners do<br />

start to default. In early<br />

March, CapGen, a New<br />

York-based private equity<br />

shop, filed a complaint in<br />

Delaware Chancery Court<br />

against two of its limited<br />

partners whom it claimed<br />

had defaulted on capital<br />

calls due on 31st<br />

December, 2008.<br />

Chancery Court against two of its<br />

limited partners whom it claimed had<br />

defaulted on capital calls due on 31st<br />

December, 2008. CapGen’s funds had<br />

$500m committed in total but the<br />

alleged defaulters were bit players:<br />

Chalice Fund was on the hook for<br />

$3.5m and WK GG Investment for<br />

$1m—and the missed call was for less<br />

than 25% of those amounts.<br />

Frank Morgan, president of Coller<br />

Capital in the US, points out that<br />

partnership documents typically<br />

permit the general partner to call on<br />

other limited partners to make up any<br />

defaulted amount, but CapGen chose<br />

to take legal action against two high<br />

net worth individuals instead. “It was<br />

a warning to other larger investors not<br />

to try this,” he says, “I do not think a<br />

lot of defaults have occurred.”<br />

In a slow deal market, Morgan says<br />

private equity firms haven’t been<br />

making many capital calls except for<br />

follow-on commitments to existing<br />

investments anyway. At some point<br />

that will change—probably sooner<br />

rather than later. Private equity funds<br />

have “use it or lose it” provisions that<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

A Unique<br />

Model of Success

PRIVATE EQUITY: IMPROVING OUTLOOK<br />

20<br />

In the Markets<br />

require general partners to cancel<br />

commitments if the money is not<br />

invested within the investment period,<br />

which is typically five years. The clock<br />

is ticking, and firms don’t want to lose<br />

the management fees they charge<br />

even on uninvested funds.“If there are<br />

still economic pressures when activity<br />

picks up, you will start to see defaults<br />

or more product trading in the<br />

secondary market,”says Morgan.<br />

Investors in private equity funds make<br />

firm capital commitments at the outset,<br />

but the sponsor does not draw money<br />

down until needed to finance a particular<br />

investment. For their own protection in<br />

this deferred funding model, general<br />

partners have long insisted on draconian<br />

penalties to discourage limited partner<br />

default. Paul Ellis, a partner in the<br />

restructuring and recovery services<br />

practice at PricewaterhouseCoopers, says<br />

every fund is different, but limited<br />

partners in default always lose their<br />

voting rights and typically forfeit 25%-<br />

50% of future fund distributions. They<br />

may be liable for future management<br />

fees on the amount of their original<br />

commitment (including the defaulted<br />

amount), too.“Those penalties are pretty<br />

significant and they affect the reputation<br />

of the investor,”says Ellis.“We have not<br />

seen any significant volume of<br />

threatened or actual defaults.”<br />

Saratoga’s Oberbeck points out that<br />

the severity of the penalties depends on<br />

where the fund is in its lifecycle and<br />

how the early investments have<br />

performed. Investors will be loath to<br />

give up future gains from a successful<br />

fund, but if a fund made its initial<br />

investments in 2006 or the first half of<br />

2007 it may well be under water.“If you<br />

have invested $40m out of $100m but<br />

you think that $40m is worth zero, what<br />

do you lose by walking away?” asks<br />

Oberbeck. “Do you want to be in the<br />

back end of a fund that has lost money?<br />

The carried interest incentives for the<br />

fund manager are not there either.”<br />

Saratoga has not experienced any<br />

limited partner defaults itself although<br />

Oberbeck has heard talk of the<br />

phenomenon. Like Ellis, he suggests<br />

that investors and private equity firms<br />

are talking to each other to work out a<br />

solution acceptable to both. General<br />

partners have to be careful, however;<br />

whatever they do to accommodate<br />

one limited partner will set a<br />

precedent other investors may try to<br />

follow. Notwithstanding the CapGen<br />

case, Oberbeck doesn’t expect<br />

sponsors to resort to litigation. “You<br />

don’t bite the hand that feeds you,“ he<br />

says. “If you sue an endowment or a<br />

pension fund it will be all over the<br />

press. It doesn’t look good.”<br />

Ellis says private equity firms have<br />

become more willing to exchange<br />

information with limited partners,<br />

particularly about valuations and<br />

potential changes to the general<br />

partner’s investment strategy. For<br />

example, in the current environment<br />

many sponsors see opportunities to buy<br />

companies out of bankruptcy, which<br />

may not have been contemplated when<br />

a fund was first launched. “The<br />

underlying concept is understated<br />

value. It happens to reside in the<br />

bankruptcy world at the moment,”says<br />

Ellis. “Limited partners who have not<br />

been involved before are concerned<br />

enough to ask more questions about<br />

why sponsors are doing this and what<br />

the implications are.”<br />

While Ellis acknowledges that<br />

general partners may shy away from<br />

capital calls if they believe limited<br />

partners will default, he has not<br />

encountered any reticence among his<br />

clients. Quite the opposite, in fact:<br />

limited partners are pressing sponsors<br />

to deploy money—they don’t like to<br />

pay fees on unfunded capital<br />

commitments. Nevertheless, sponsors<br />

won’t go out of their way to<br />

antagonise limited partners by<br />

investing in troubled industries such<br />

Frank Morgan, president of Coller Capital in<br />

the US, points out that partnership<br />

documents typically permit the general<br />

partner to call on other limited partners to<br />

make up any defaulted amount, but CapGen<br />

chose to take legal action against two high<br />

net worth individuals instead.“It was a<br />

warning to other larger investors not to try<br />

this,” he says,“I don’t think a lot of defaults<br />

have occurred.” Photograph kindly provided<br />

by Coller Capital, August 2009.<br />

Paul Ellis, a partner in the restructuring and<br />

recovery services practice at<br />

PricewaterhouseCoopers, says every fund is<br />

different, but limited partners in default<br />

always lose their voting rights and typically<br />

forfeit 25%-50% of future fund distributions.<br />

Photograph kindly supplied by<br />

PricewaterhouseCoopers, August 2009.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

Looking for liquidity? Don’t take the wrong turning. The route to our Liquidity Hub<br />

is safe and dependable – and you’ll find a solution that’s exactly right for you.<br />

For more directions, call our Global Securities Financing team at +352-243-36868<br />

or visit clearstream.com

PRIVATE EQUITY: IMPROVING OUTLOOK<br />

22<br />

In the Markets<br />

as auto parts, for example. “It would<br />

be reasonable to expect general<br />

partner reluctance to call capital<br />

without a significant amount of<br />

limited partner support,” says Ellis.<br />

“[However,] we are not seeing<br />

defaults or threats of default.”<br />

Kathy Jeramaz-Larson, executive<br />

director of the Institutional Limited<br />

Partners Association, a Toronto-based<br />

association dedicated to private equity<br />

investors around the globe, wonders<br />

whether the talk of limited partner<br />

default is real or if it is simply an urban<br />

legend.“I have not heard from either<br />

limited partners or general partners of<br />

any limited partner defaults,”she says.<br />

“That’s not to say they aren’t<br />

happening—it’s just that I am not<br />

aware of any specific instances.”<br />

Jeramaz-Larson has heard of<br />

situations where investors have made<br />

hard decisions not to reinvest in the next<br />

fund offered by a particular sponsor,<br />

however. That’s consistent with Coller<br />

Capital’s finding that 31% of limited<br />

partners plan to reduce the number of<br />

general partner relationships they have,<br />

and that 20% intend to cut their<br />

allocation to private equity in the next<br />

two years. Investors also expect that<br />

25% of private equity sponsors will be<br />

unable to raise new funds, effectively<br />

putting those firms out of business<br />

when their existing funds liquidate. If<br />

investors can afford to wait, a<br />

combination of future distributions<br />

and passing up opportunities to<br />

reinvest with some managers will get<br />

their allocation back on target. The<br />

secondary market is always an option<br />

for those under immediate pressure,<br />

too. “Not only do they get some<br />

consideration for what they invested<br />

in the fund but they get relieved of the<br />

ongoing commitment,” says Coller<br />

Capital’s Morgan. “I expect people to<br />

find that attractive.”For most investors<br />

under pressure from excess exposure<br />

to private equity, default on capital<br />

calls is likely to be a last resort.<br />

UK SURVEY CHARTS UPS &<br />

<strong>DO</strong>WNS OF PRIVATE EQUITY<br />

The number of private equity houses is expected<br />

to fall significantly over the next 24 months,<br />

according to a recent survey carried out by the<br />

UK accounting and financial services firm Smith &<br />

Williamson. The survey of 136 private equity senior<br />

executives was conducted between 10th June and<br />

3rd July 2009. Some 75 different mid-market<br />

(£5m-£50m) PE houses responded, between them<br />

representing more than two-thirds of all UK<br />

mid-market PE transactions.<br />

According to Brian Livingston, head of private<br />

equity at the firm, some two-thirds of the 136 senior<br />

private equity executives across the 75 firms polled<br />

shared the gloomy prediction for the industry.<br />

“Recent poor performance has meant many private<br />

equity houses are being squeezed: they cannot raise<br />

new equity funds and cannot raise bank finance<br />

either, since the banks are increasingly focusing on<br />

investors’ track records before committing finance for<br />

deals. As a result, many firms are effectively unable<br />

to make investments and may have little choice but<br />

to merge or shut down,” notes Livingston.<br />

While respondents overwhelmingly stated that<br />

entry multiples on new investments have fallen since<br />

2007, so far lower prices have not resulted in more<br />

deals. Some 82% of the survey respondents agreed<br />

that over the last two years it has become much<br />

harder for companies to raise finance from private<br />

equity investors. Moreover, 93% believe that more<br />

private equity-backed businesses will breach banking<br />

covenants in the year ahead. The private equity<br />

community does not expect to get much help from<br />

the government either. Only 12% believe government<br />

policies will help to ease problems in the private<br />

equity industry.<br />

Livingston adds: “Even with lower entry multiples,<br />

the lack of bank funding makes it difficult to<br />

structure deals in a way which will generate<br />

satisfactory returns. Instead, we are seeing more<br />

and more private equity houses shifting their focus<br />

from making new investments to preserving the value<br />

of their existing portfolios.”<br />

However, the outlook is brighter. Some 68% of<br />

survey respondents think investor confidence will<br />

begin to return, while half believe bank finance will<br />

become more readily available in coming months<br />

and 57% expect the current recession in the UK to<br />

end by 2010.<br />

S E P T E M B E R 2 0 0 9 • F T S E G L O B A L M A R K E T S

Looking for a risk management process<br />

for sophisticated UCITS III funds?<br />

EMA’s Excerpt meets regulatory and fund<br />

manager risk analysis and attribution needs,<br />

including:<br />

• coverage of portfolios of equities, bonds,<br />

currencies, and derivatives<br />

• historical and monte carlo VaR<br />

risk analyses with factor based attribution<br />

• fully repriced stress test using user defined<br />

or historical scenarios<br />

• long, long-short, 130/30 and absolute<br />

return portfolios.<br />

If you would like to discuss UCITS III or any<br />

other risk analysis issues, please contact us:<br />

www.emapplications.com<br />

+44 (0) 20 7397 8395<br />

enquiry@emapplications.com<br />

EM Applications<br />

analysis into action<br />

The EM Applications risk model is based on<br />

original work by Al Stroyny

INTEREST RATE OUTLOOK: STEADY AS SHE GOES<br />

24<br />