Smart Beta 2.0 - EDHEC-Risk

Smart Beta 2.0 - EDHEC-Risk

Smart Beta 2.0 - EDHEC-Risk

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

2. Controlling the <strong>Risk</strong>s of <strong>Smart</strong> <strong>Beta</strong> Investing:<br />

The <strong>Smart</strong> <strong>Beta</strong> <strong>2.0</strong> Approach<br />

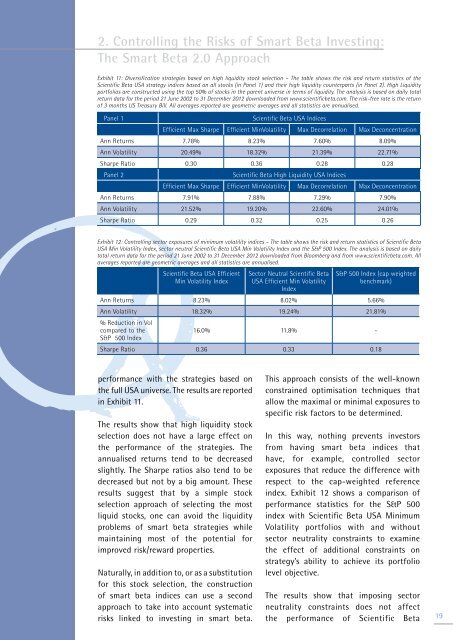

Exhibit 11: Diversification strategies based on high liquidity stock selection – The table shows the risk and return statistics of the<br />

Scientific <strong>Beta</strong> USA strategy indices based on all stocks (in Panel 1) and their high liquidity counterparts (in Panel 2). High Liquidity<br />

portfolios are constructed using the top 50% of stocks in the parent universe in terms of liquidity. The analysis is based on daily total<br />

return data for the period 21 June 2002 to 31 December 2012 downloaded from www.scientificbeta.com. The risk-free rate is the return<br />

of 3 months US Treasury Bill. All averages reported are geometric averages and all statistics are annualised.<br />

Panel 1<br />

Scientific <strong>Beta</strong> USA Indices<br />

Efficient Max Sharpe Efficient MinVolatility Max Decorrelation Max Deconcentration<br />

Ann Returns 7.78% 8.23% 7.60% 8.09%<br />

Ann Volatility 20.49% 18.32% 21.39% 22.71%<br />

Sharpe Ratio 0.30 0.36 0.28 0.28<br />

Panel 2<br />

Scientific <strong>Beta</strong> High Liquidity USA Indices<br />

Efficient Max Sharpe Efficient MinVolatility Max Decorrelation Max Deconcentration<br />

Ann Returns 7.91% 7.88% 7.29% 7.90%<br />

Ann Volatility 21.52% 19.20% 22.60% 24.01%<br />

Sharpe Ratio 0.29 0.32 0.25 0.26<br />

Exhibit 12: Controlling sector exposures of minimum volatility indices – The table shows the risk and return statistics of Scientific <strong>Beta</strong><br />

USA Min Volatility Index, sector neutral Scientific <strong>Beta</strong> USA Min Volatility Index and the S&P 500 Index. The analysis is based on daily<br />

total return data for the period 21 June 2002 to 31 December 2012 downloaded from Bloomberg and from www.scientificbeta.com. All<br />

averages reported are geometric averages and all statistics are annualised.<br />

Scientific <strong>Beta</strong> USA Efficient<br />

Min Volatility Index<br />

Sector Neutral Scientific <strong>Beta</strong><br />

USA Efficient Min Volatility<br />

Index<br />

S&P 500 Index (cap weighted<br />

benchmark)<br />

Ann Returns 8.23% 8.02% 5.66%<br />

Ann Volatility 18.32% 19.24% 21.81%<br />

% Reduction in Vol<br />

compared to the<br />

16.0% 11.8% -<br />

S&P 500 Index<br />

Sharpe Ratio 0.36 0.33 0.18<br />

performance with the strategies based on<br />

the full USA universe. The results are reported<br />

in Exhibit 11.<br />

The results show that high liquidity stock<br />

selection does not have a large effect on<br />

the performance of the strategies. The<br />

annualised returns tend to be decreased<br />

slightly. The Sharpe ratios also tend to be<br />

decreased but not by a big amount. These<br />

results suggest that by a simple stock<br />

selection approach of selecting the most<br />

liquid stocks, one can avoid the liquidity<br />

problems of smart beta strategies while<br />

maintaining most of the potential for<br />

improved risk/reward properties.<br />

Naturally, in addition to, or as a substitution<br />

for this stock selection, the construction<br />

of smart beta indices can use a second<br />

approach to take into account systematic<br />

risks linked to investing in smart beta.<br />

This approach consists of the well-known<br />

constrained optimisation techniques that<br />

allow the maximal or minimal exposures to<br />

specific risk factors to be determined.<br />

In this way, nothing prevents investors<br />

from having smart beta indices that<br />

have, for example, controlled sector<br />

exposures that reduce the difference with<br />

respect to the cap-weighted reference<br />

index. Exhibit 12 shows a comparison of<br />

performance statistics for the S&P 500<br />

index with Scientific <strong>Beta</strong> USA Minimum<br />

Volatility portfolios with and without<br />

sector neutrality constraints to examine<br />

the effect of additional constraints on<br />

strategy’s ability to achieve its portfolio<br />

level objective.<br />

The results show that imposing sector<br />

neutrality constraints does not affect<br />

the performance of Scientific <strong>Beta</strong> 19