Export Marketing Survey: German Market for Textile and Clothing

Export Marketing Survey: German Market for Textile and Clothing

Export Marketing Survey: German Market for Textile and Clothing

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

This Project is financed<br />

by the European Union<br />

Support to <strong>Export</strong> Promotion<br />

<strong>and</strong> Investment Attraction in<br />

the Republic of Moldova<br />

EuropeAid/126810/C/SER/MD<br />

This Project is implemented by a<br />

Consortium led by GFA<br />

Consulting Group<br />

Structure of the<br />

<strong>German</strong> textile <strong>and</strong><br />

clothing industry<br />

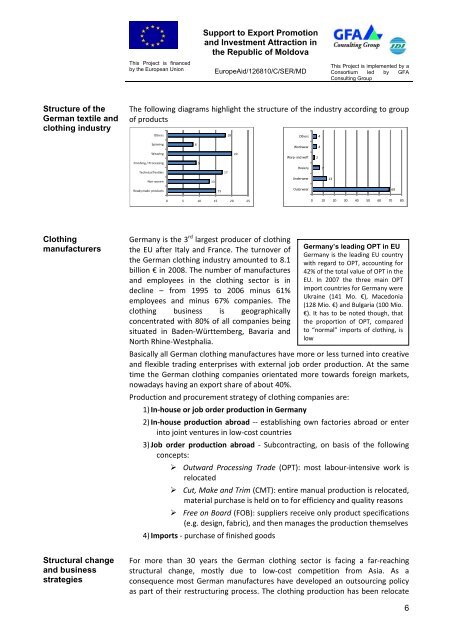

The following diagrams highlight the structure of the industry according to group<br />

of products<br />

Others<br />

18<br />

Others<br />

4<br />

Spinning<br />

8<br />

Workwear<br />

4<br />

Weaving<br />

Finishing / Processing<br />

Technical <strong>Textile</strong>s<br />

9<br />

17<br />

20<br />

Warp‐<strong>and</strong> weft<br />

Hosiery<br />

2<br />

7<br />

Non‐woven<br />

13<br />

Underwear<br />

13<br />

Ready made products<br />

15<br />

Outerwear<br />

69<br />

0 5 10 15 20 25<br />

0 10 20 30 40 50 60 70 80<br />

<strong>Clothing</strong><br />

manufacturers<br />

<strong>German</strong>y is the 3 rd largest producer of clothing<br />

the EU after Italy <strong>and</strong> France. The turnover of<br />

the <strong>German</strong> clothing industry amounted to 8.1<br />

billion € in 2008. The number of manufactures<br />

<strong>and</strong> employees in the clothing sector is in<br />

decline – from 1995 to 2006 minus 61%<br />

employees <strong>and</strong> minus 67% companies. The<br />

clothing business is geographically<br />

concentrated with 80% of all companies being<br />

situated in Baden‐Württemberg, Bavaria <strong>and</strong><br />

North Rhine‐Westphalia.<br />

<strong>German</strong>y’s leading OPT in EU<br />

<strong>German</strong>y is the leading EU country<br />

with regard to OPT, accounting <strong>for</strong><br />

42% of the total value of OPT in the<br />

EU. In 2007 the three main OPT<br />

import countries <strong>for</strong> <strong>German</strong>y were<br />

Ukraine (141 Mo. €), Macedonia<br />

(128 Mio. €) <strong>and</strong> Bulgaria (100 Mio.<br />

€). It has to be noted though, that<br />

the proportion of OPT, compared<br />

to “normal” imports of clothing, is<br />

low<br />

Basically all <strong>German</strong> clothing manufactures have more or less turned into creative<br />

<strong>and</strong> flexible trading enterprises with external job order production. At the same<br />

time the <strong>German</strong> clothing companies orientated more towards <strong>for</strong>eign markets,<br />

nowadays having an export share of about 40%.<br />

Production <strong>and</strong> procurement strategy of clothing companies are:<br />

1) In‐house or job order production in <strong>German</strong>y<br />

2) In‐house production abroad ‐‐ establishing own factories abroad or enter<br />

into joint ventures in low‐cost countries<br />

3) Job order production abroad ‐ Subcontracting, on basis of the following<br />

concepts:<br />

‣ Outward Processing Trade (OPT): most labour‐intensive work is<br />

relocated<br />

‣ Cut, Make <strong>and</strong> Trim (CMT): entire manual production is relocated,<br />

material purchase is held on to <strong>for</strong> efficiency <strong>and</strong> quality reasons<br />

‣ Free on Board (FOB): suppliers receive only product specifications<br />

(e.g. design, fabric), <strong>and</strong> then manages the production themselves<br />

4) Imports ‐ purchase of finished goods<br />

Structural change<br />

<strong>and</strong> business<br />

strategies<br />

For more than 30 years the <strong>German</strong> clothing sector is facing a far‐reaching<br />

structural change, mostly due to low‐cost competition from Asia. As a<br />

consequence most <strong>German</strong> manufactures have developed an outsourcing policy<br />

as part of their restructuring process. The clothing production has been relocate<br />

6