Taxability of Real Estate transactions

Taxability of Real Estate transactions

Taxability of Real Estate transactions

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

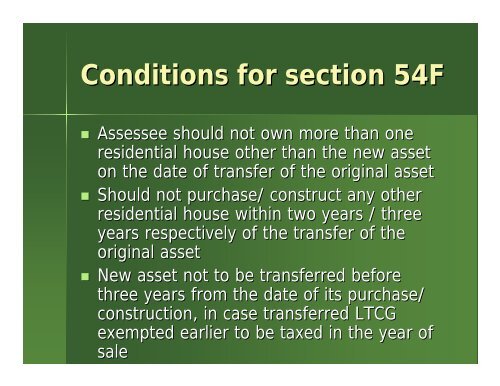

Conditions for section 54F<br />

• Assessee should not own more than one<br />

residential house other than the new asset<br />

on the date <strong>of</strong> transfer <strong>of</strong> the original asset<br />

• Should not purchase/ construct any other<br />

residential house within two years / three<br />

years respectively <strong>of</strong> the transfer <strong>of</strong> the<br />

original asset<br />

• New asset not to be transferred before<br />

three years from the date <strong>of</strong> its purchase/<br />

construction, in case transferred LTCG<br />

exempted earlier to be taxed in the year <strong>of</strong><br />

sale