56 Business <strong>The</strong> <strong>Economist</strong> <strong>April</strong> <strong>19</strong>th <strong>2014</strong>SchumpeterMunk’s taleHow a formerrefugee from the Nazis made and lost several fortunesYOU can’t be right all the time. In a <strong>19</strong>95 profile of Peter Munk,the founder of Barrick Gold, a mining giant, <strong>The</strong> <strong>Economist</strong>concluded that the biggest problem facing the company was whowould replace him as boss. Mr Munkwill at last step down as thecompany’s chairman at the annual meeting on <strong>April</strong> 30th, aged86. In the same profile we fretted that by spending $500m on aproperty company, Mr Munk risked ending up in the same boatas two fellow Canadian tycoons, Paul Reichmann and RobertCampeau, who had gone spectacularly bankrupt. In 2006 MrMunkhad the last laugh, selling the company for $9 billion.<strong>The</strong>re were lots of reasons why our <strong>19</strong>95 profile was so pessimistic.Mr Munk was already 67. <strong>The</strong> mining industry is an unforgivingone. Diversifying into property is a well-known road toruin. And Mr Munk had a catalogue of failures to his name. Butwe forgot one vital thing: his ability to turn failure into successand threat into opportunity.Failure is a hot topic in American business at the moment. SiliconValley entrepreneurs argue that the valley’s success is its tolerancefor failure. Historians apply the same argument to thegreat arc ofAmerican history: the United States has pulled aheadof its rivals in part because its entrepreneurs have always had atalent for picking themselves up, and its bankruptcy laws areamong the most lenient in the world.In Mr Munk’s early years, “threat” meant more than the possibilitythat his latest app might not get the nod from some venturecapitalist; and “opportunity” meant more than the chance ofbeing bought out by Facebook. In <strong>19</strong>44 he fled his native Hungaryon the “Kastnertrain”, which carried almost1,700 Jews who wereable to pay for their passage to Switzerland and thus escape thegas chambers. Four years laterhe arrived in Canada with his familyfortune gone, and worked his way through university, cleaningcars and selling Christmas trees, ending up with a degree inelectronic engineering.His first business, the Clairtone Sound Corporation, wentfrom boom to bust in 11 years. One moment the former pennilessimmigrant was driving a Pierce-Arrow convertible down MadisonAvenue and payingFrankSinatra to endorse his hi-fi systems.<strong>The</strong> next moment he was unceremoniously dumped from thecompany, which then folded, the victim ofoverambitious expansionand Japanese competition. Nina Munk, one of his five children,says that his first experience offailure marked him for life. Itprobably lay behind his penchant for hedging output when hestarted in mining, an innovation at the time among gold miners.“Every human being makes mistakes,” he says. “You have tohedge so that if a decision goes wrong it does not eliminate yourabilityto stayatthe table and playon.” Butitdid notdull his appetitefor venturing into challenging businesses.After the collapse of Clairtone Mr Munk “played on” by investingin hotels in the South Pacific. <strong>The</strong> threat of failure continuedto stalk him. A resort he tried to build in Egypt with AdnanKhashoggi, an arms dealer, went nowhere. Abusiness park he developedsouth of Berlin after the Soviet empire imploded beganwell but was undercut by competing parks on the Berlin ringroad. Nevertheless, he succeeded in restoring his fortune.Mr Munk’s greatest gamble was his move into mining whenhe founded Barrick in <strong>19</strong>83. He knew little about the business atthe time—just as he had known little about hotels before that. Buthis ignorance freed him from the assumptions that dominatedthe industry. It was mostly run by geologists and engineerswhose aim was to dig enormous holes with other people’s money,paying little regard to shareholder returns. Gold miners weresupposed to be “believers” in gold rather than efficient managersout to maximise profits. “Bullshit,” thought Mr Munk; he soonchanged all that. A string of ever-more audacious acquisitionsturned Barrick into what was for a while the world’s largest goldminer and is still among the biggest.MrMunkalso turned outto be a first-rate managerof hisgrowingbusiness empire. He may have been willing to overrule oldhands when it came to whether mining should be run by managersor miners—and do it with absolute self-confidence thatbrooked no question. But he was also willing to delegate operationaldecisions to experts. Indeed, he explicitly refused to micromanage,to give himselftime to thinkbig thoughts.Sailing into stormy weatherIn recent years Barrick’s competitive advantage has been erodedin partbecause everyotherminingcompanyhasnowrecognisedthe force of his insight. He is leaving the company he created at adifficult time: last year Barrick lost $10.4 billion as the gold pricetumbled; and a huge project in the Andes, that the firm has beenworking on for years, was halted. But none ofthese problems hasdulled his appetite for risk. He may yet have some big, farewelldeal for Barrick up his sleeve. Even if not, he can now give his fullattention to a side-project he has been working on for years, toturn an old naval dockyard in Montenegro into a marina wherethe super-rich can parktheir yachts alongside his.Whether fortune will smile on his latest venture is unclear:will Russian oligarchs, its most obvious customers, be impoverishedby Western sanctions over Russia’s meddling in Ukraine, orwill they flock to his marina to hunker down until the stormblows over? But Mr Munk is less troubled by the prospect of failurethis time around. He plans to give almost all of his fortune tocharity, and has already made a start by giving $160m to hospitalsand universities in Canada and Israel. He wishes to spare his childrenthe curse of too much inherited wealth. Take it from a manwho knows a thing or two about success or failure: there are fewthings more dangerous than making life too easy. 7<strong>Economist</strong>.com/blogs/schumpeter

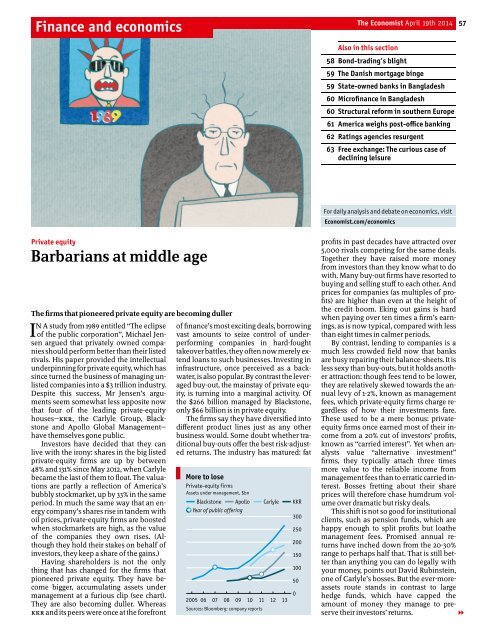

Finance and economics<strong>The</strong> <strong>Economist</strong> <strong>April</strong> <strong>19</strong>th <strong>2014</strong> 57Also in this section58 Bond-trading’s blight59 <strong>The</strong> Danish mortgage binge59 State-owned banks in Bangladesh60 Microfinance in Bangladesh60 Structural reform in southern Europe61 America weighs post-office banking62 Ratings agencies resurgent63 Free exchange: <strong>The</strong> curious case ofdeclining leisureFor daily analysis and debate on economics, visit<strong>Economist</strong>.com/economicsPrivate equityBarbarians at middle age<strong>The</strong> firms that pioneered private equity are becoming dullerIN A study from <strong>19</strong>89 entitled “<strong>The</strong> eclipseof the public corporation”, Michael Jensenargued that privately owned companiesshouldperform betterthan their listedrivals. His paper provided the intellectualunderpinningforprivate equity, which hassince turned the business of managing unlistedcompanies into a $3 trillion industry.Despite this success, Mr Jensen’s argumentsseem somewhat less apposite nowthat four of the leading private-equityhouses—KKR, the Carlyle Group, Blackstoneand Apollo Global Management—have themselves gone public.Investors have decided that they canlive with the irony: shares in the big listedprivate-equity firms are up by between48% and 131% since May 2012, when Carlylebecame the last ofthem to float. <strong>The</strong> valuationsare partly a reflection of America’sMore to losebubbly stockmarket, up by 33% in the sameperiod. In much the same way that an energycompany’s shares rise in tandem withBlackstoneoil prices, private-equity firms are boostedwhen stockmarkets are high, as the valueof the companies they own rises. (Althoughthey hold their stakes on behalf ofinvestors, they keep a share ofthe gains.)Having shareholders is not the onlything that has changed for the firms thatpioneered private equity. <strong>The</strong>y have becomebigger, accumulating assets undermanagement at a furious clip (see chart).<strong>The</strong>y are also becoming duller. WhereasKKR and itspeerswere once atthe forefrontoffinance’s most exciting deals, borrowingvast amounts to seize control of underperformingcompanies in hard-foughttakeoverbattles, theyoften nowmerely extendloans to such businesses. Investing ininfrastructure, once perceived as a backwater,is also popular. By contrast the leveragedbuy-out, the mainstay of private equity,is turning into a marginal activity. Ofthe $266 billion managed by Blackstone,only $66 billion is in private equity.<strong>The</strong> firms say they have diversified intodifferent product lines just as any otherbusiness would. Some doubt whether traditionalbuy-outs offer the best risk-adjustedreturns. <strong>The</strong> industry has matured: fatPrivate-equity firmsAssets under management, $bnApolloYear of public offeringSources: Bloomberg; company reportsCarlyle2005 06 07 08 09 10 11 12 13KKR300<strong>25</strong>0200150100500profits in past decades have attracted over5,000 rivals competing for the same deals.Together they have raised more moneyfrom investors than they know what to dowith. Many buy-out firms have resorted tobuying and selling stuff to each other. Andprices for companies (as multiples of profits)are higher than even at the height ofthe credit boom. Eking out gains is hardwhen paying over ten times a firm’s earnings,as is now typical, compared with lessthan eight times in calmer periods.By contrast, lending to companies is amuch less crowded field now that banksare busy repairingtheirbalance-sheets. It isless sexy than buy-outs, but it holds anotherattraction: though fees tend to be lower,they are relatively skewed towards the annuallevy of 1-2%, known as managementfees, which private-equity firms charge regardlessof how their investments fare.<strong>The</strong>se used to be a mere bonus: privateequityfirms once earned most of their incomefrom a 20% cut of investors’ profits,known as “carried interest”. Yet when analystsvalue “alternative investment”firms, they typically attach three timesmore value to the reliable income frommanagement fees than to erratic carried interest.Bosses fretting about their shareprices will therefore chase humdrum volumeover dramatic but risky deals.This shift is not so good for institutionalclients, such as pension funds, which arehappy enough to split profits but loathemanagement fees. Promised annual returnshave inched down from the 20-30%range to perhaps half that. That is still betterthan anything you can do legally withyour money, points out David Rubinstein,one of Carlyle’s bosses. But the ever-moreassetsroute stands in contrast to largehedge funds, which have capped theamount of money they manage to preservetheir investors’ returns.1