Chapter 9 Materiality and Risk - HCC Learning Web

Chapter 9 Materiality and Risk - HCC Learning Web

Chapter 9 Materiality and Risk - HCC Learning Web

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

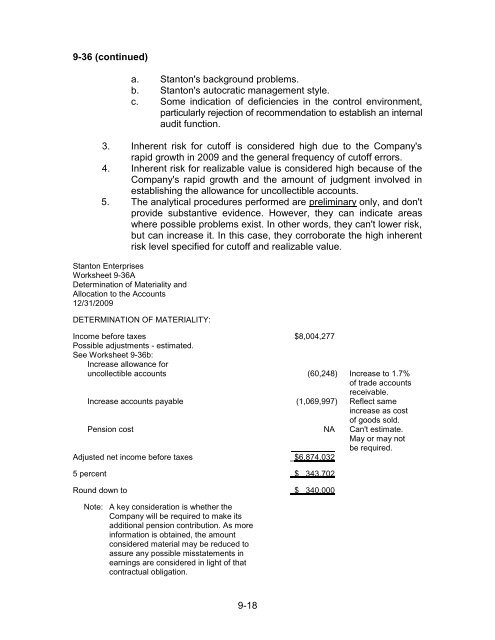

9-36 (continued)a. Stanton's background problems.b. Stanton's autocratic management style.c. Some indication of deficiencies in the control environment,particularly rejection of recommendation to establish an internalaudit function.3. Inherent risk for cutoff is considered high due to the Company'srapid growth in 2009 <strong>and</strong> the general frequency of cutoff errors.4. Inherent risk for realizable value is considered high because of theCompany's rapid growth <strong>and</strong> the amount of judgment involved inestablishing the allowance for uncollectible accounts.5. The analytical procedures performed are preliminary only, <strong>and</strong> don'tprovide substantive evidence. However, they can indicate areaswhere possible problems exist. In other words, they can't lower risk,but can increase it. In this case, they corroborate the high inherentrisk level specified for cutoff <strong>and</strong> realizable value.Stanton EnterprisesWorksheet 9-36ADetermination of <strong>Materiality</strong> <strong>and</strong>Allocation to the Accounts12/31/2009DETERMINATION OF MATERIALITY:Income before taxes $8,004,277Possible adjustments - estimated.See Worksheet 9-36b:Increase allowance foruncollectible accounts (60,248) Increase to 1.7%of trade accountsreceivable.Increase accounts payable (1,069,997) Reflect sameincrease as costof goods sold.Pension cost NA Can't estimate.May or may notbe required.Adjusted net income before taxes $6,874,0325 percent $ 343,702Round down to $ 340,000Note: A key consideration is whether theCompany will be required to make itsadditional pension contribution. As moreinformation is obtained, the amountconsidered material may be reduced toassure any possible misstatements inearnings are considered in light of thatcontractual obligation.9-18