<strong>ICT</strong> <strong>and</strong> e-bus<strong>in</strong>ess impact <strong>in</strong> <strong>the</strong> furniture <strong>in</strong>dustry3.3.2 SCM <strong>in</strong> <strong>the</strong> furniture <strong>in</strong>dustryA complex <strong>in</strong>dustry value cha<strong>in</strong>As highlighted <strong>in</strong> section 2.3, today's furniture manufacturers face new bus<strong>in</strong>esscomplexities. Product dem<strong>and</strong>s span a broad range, from commoditized to highlycustomized products. Customer dem<strong>and</strong> is cont<strong>in</strong>uously chang<strong>in</strong>g, while competition fromlow-cost countries is <strong>in</strong>creas<strong>in</strong>g. Creat<strong>in</strong>g br<strong>and</strong> differentiation <strong>and</strong> keep<strong>in</strong>g market sharedepend more than ever on underst<strong>and</strong><strong>in</strong>g customer needs <strong>and</strong> provid<strong>in</strong>g customerservice <strong>and</strong> sales effectiveness. To keep pace with <strong>the</strong> customers’ dem<strong>and</strong>manufacturers are offer<strong>in</strong>g exp<strong>and</strong>ed product l<strong>in</strong>es <strong>and</strong> custom options. The wide varietyof dimensions, colours, f<strong>in</strong>ishes, fabrics <strong>and</strong> product options - leav<strong>in</strong>g aside <strong>the</strong> value of<strong>the</strong> stock, efficiencies <strong>in</strong> storage <strong>and</strong> logistics - are plac<strong>in</strong>g <strong>in</strong>creased dem<strong>and</strong>s on<strong>in</strong>formation systems to provide <strong>the</strong> functionality <strong>and</strong> flexibility required to address all <strong>the</strong>bus<strong>in</strong>ess requirements. On top of this come <strong>the</strong> dem<strong>and</strong>s by customers for reduceddelivery times. In addition, <strong>in</strong> some market segments such as contract furnish<strong>in</strong>gs,custom orders are <strong>the</strong> norm. The result is a low volume production environment with verycomplex product development, schedul<strong>in</strong>g, <strong>and</strong> production needs. This sort of low volumeproduction environment is also very common <strong>in</strong> high-tech <strong>in</strong>dustries such as defence ormedical <strong>in</strong>strumentation. The difference is that <strong>the</strong>re is considerably more price sensitivity<strong>in</strong> <strong>the</strong> furniture <strong>in</strong>dustry <strong>and</strong> little tolerance for miss<strong>in</strong>g production deadl<strong>in</strong>es.Flexibility <strong>and</strong> process efficiency are key success factorsThese trends are accompanied by pressure of ma<strong>in</strong>ta<strong>in</strong><strong>in</strong>g marg<strong>in</strong>s <strong>and</strong> profitability. Vitalto success is, <strong>the</strong>refore, <strong>the</strong> ability to control costs <strong>and</strong> optimize processes. As a result,many furniture companies are focus<strong>in</strong>g on improv<strong>in</strong>g supply cha<strong>in</strong> management, onstreaml<strong>in</strong><strong>in</strong>g operations <strong>and</strong> optimiz<strong>in</strong>g <strong>the</strong>ir ability to adapt to a chang<strong>in</strong>g bus<strong>in</strong>essenvironment.However, at <strong>the</strong> same time, supply cha<strong>in</strong> improvement efforts are constra<strong>in</strong>ed, especiallyamong smaller players, by a fragmented <strong>and</strong> disparate <strong>ICT</strong> <strong>in</strong>frastructure, poorly<strong>in</strong>tegrated solutions, <strong>in</strong>clud<strong>in</strong>g legacy systems, manufactur<strong>in</strong>g execution systems, <strong>and</strong> anassortment of custom applications. Not only does this mean high <strong>in</strong>tegration costs, butmore importantly, it means impaired visibility <strong>in</strong>to supply cha<strong>in</strong> processes.SCM <strong>and</strong> <strong>in</strong>ternal process automationA major technological issue is that SCM applications rely upon <strong>the</strong> k<strong>in</strong>d of <strong>in</strong>formation thatis stored <strong>in</strong> ERP software or <strong>in</strong> o<strong>the</strong>r applications used for <strong>in</strong>ternal processes.Theoretically, SCM applications could be fed with data from legacy systems (for manysmall companies this means Excel spreadsheets spread across <strong>the</strong> company) but this<strong>in</strong>evitably would impact on <strong>the</strong> quality of <strong>the</strong> outputs. SCM applications benefit fromhav<strong>in</strong>g a s<strong>in</strong>gle major source for <strong>in</strong>formation, ideally ERP. It can be concluded, <strong>the</strong>refore,that <strong>the</strong> successful implementation of supply cha<strong>in</strong> <strong>in</strong>tegration can hardly be achievedunless <strong>in</strong>ternal process <strong>in</strong>tegration has been previously <strong>and</strong> effectively achieved.The two areas, <strong>in</strong>tra-enterprise <strong>in</strong>tegration (ma<strong>in</strong>ly represented by ERP) <strong>and</strong> <strong>in</strong>terenterprise<strong>in</strong>tegration (ma<strong>in</strong>ly represented by SCM) are strongly <strong>in</strong>tertw<strong>in</strong>ed <strong>and</strong> havevery similar features.55

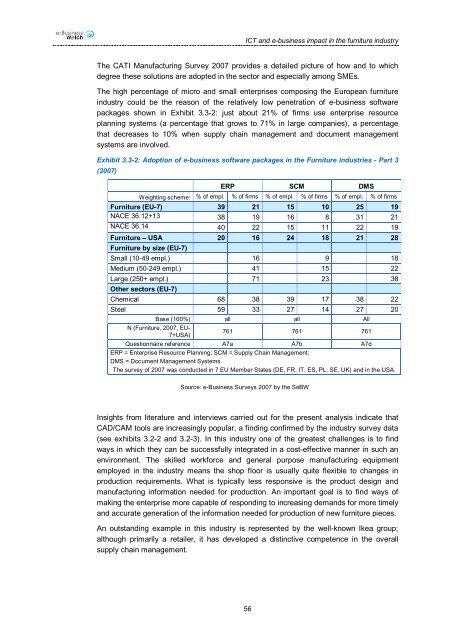

<strong>ICT</strong> <strong>and</strong> e-bus<strong>in</strong>ess impact <strong>in</strong> <strong>the</strong> furniture <strong>in</strong>dustryThe CATI Manufactur<strong>in</strong>g Survey 2007 provides a detailed picture of how <strong>and</strong> to whichdegree <strong>the</strong>se solutions are adopted <strong>in</strong> <strong>the</strong> sector <strong>and</strong> especially among SMEs.The high percentage of micro <strong>and</strong> small enterprises compos<strong>in</strong>g <strong>the</strong> European furniture<strong>in</strong>dustry could be <strong>the</strong> reason of <strong>the</strong> relatively low penetration of e-bus<strong>in</strong>ess softwarepackages shown <strong>in</strong> Exhibit 3.3-2: just about 21% of firms use enterprise resourceplann<strong>in</strong>g systems (a percentage that grows to 71% <strong>in</strong> large companies), a percentagethat decreases to 10% when supply cha<strong>in</strong> management <strong>and</strong> document managementsystems are <strong>in</strong>volved.Exhibit 3.3-2: Adoption of e-bus<strong>in</strong>ess software packages <strong>in</strong> <strong>the</strong> <strong>Furniture</strong> <strong>in</strong>dustries - Part 3(2007)ERP SCM DMSWeight<strong>in</strong>g scheme: % of empl. % of firms % of empl. % of firms % of empl. % of firms<strong>Furniture</strong> (EU-7) 39 21 15 10 25 19NACE 36.12+13 38 19 16 8 31 21NACE 36.14 40 22 15 11 22 19<strong>Furniture</strong> – USA 20 16 24 18 21 28<strong>Furniture</strong> by size (EU-7)Small (10-49 empl.) 16 9 18Medium (50-249 empl.) 41 15 22Large (250+ empl.) 71 23 38O<strong>the</strong>r sectors (EU-7)Chemical 68 38 39 17 38 22Steel 59 33 27 14 27 20Base (100%) all all AllN (<strong>Furniture</strong>, 2007, EU-7+USA)761 761 761Questionnaire reference A7a A7b A7dERP = Enterprise Resource Plann<strong>in</strong>g; SCM = Supply Cha<strong>in</strong> Management;DMS = Document Management SystemsThe survey of 2007 was conducted <strong>in</strong> 7 EU Member States (DE, FR, IT, ES, PL, SE, UK) <strong>and</strong> <strong>in</strong> <strong>the</strong> USA.Source: e-<strong>Bus<strong>in</strong>ess</strong> Surveys 2007 by <strong>the</strong> SeBWInsights from literature <strong>and</strong> <strong>in</strong>terviews carried out for <strong>the</strong> present analysis <strong>in</strong>dicate thatCAD/CAM tools are <strong>in</strong>creas<strong>in</strong>gly popular, a f<strong>in</strong>d<strong>in</strong>g confirmed by <strong>the</strong> <strong>in</strong>dustry survey data(see exhibits 3.2-2 <strong>and</strong> 3.2-3). In this <strong>in</strong>dustry one of <strong>the</strong> greatest challenges is to f<strong>in</strong>dways <strong>in</strong> which <strong>the</strong>y can be successfully <strong>in</strong>tegrated <strong>in</strong> a cost-effective manner <strong>in</strong> such anenvironment. The skilled workforce <strong>and</strong> general purpose manufactur<strong>in</strong>g equipmentemployed <strong>in</strong> <strong>the</strong> <strong>in</strong>dustry means <strong>the</strong> shop floor is usually quite flexible to changes <strong>in</strong>production requirements. What is typically less responsive is <strong>the</strong> product design <strong>and</strong>manufactur<strong>in</strong>g <strong>in</strong>formation needed for production. An important goal is to f<strong>in</strong>d ways ofmak<strong>in</strong>g <strong>the</strong> enterprise more capable of respond<strong>in</strong>g to <strong>in</strong>creas<strong>in</strong>g dem<strong>and</strong>s for more timely<strong>and</strong> accurate generation of <strong>the</strong> <strong>in</strong>formation needed for production of new furniture pieces.An outst<strong>and</strong><strong>in</strong>g example <strong>in</strong> this <strong>in</strong>dustry is represented by <strong>the</strong> well-known Ikea group;although primarily a retailer, it has developed a dist<strong>in</strong>ctive competence <strong>in</strong> <strong>the</strong> overallsupply cha<strong>in</strong> management.56