MICROBANKING BULLETIN - Microfinance Information Exchange

MICROBANKING BULLETIN - Microfinance Information Exchange

MICROBANKING BULLETIN - Microfinance Information Exchange

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

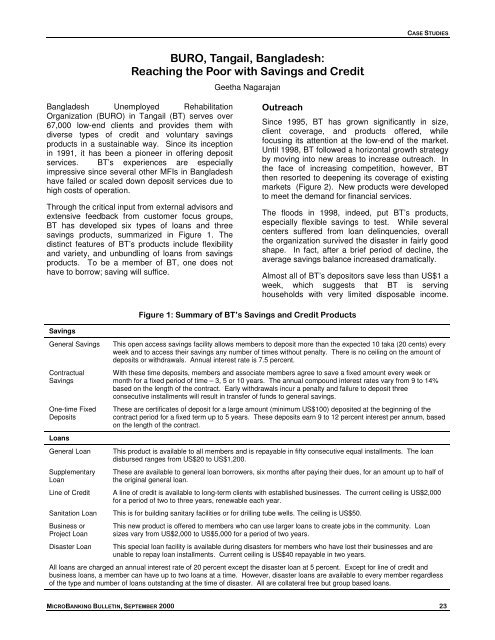

CASE STUDIESBURO, Tangail, Bangladesh:Reaching the Poor with Savings and CreditGeetha NagarajanBangladesh Unemployed RehabilitationOrganization (BURO) in Tangail (BT) serves over67,000 low-end clients and provides them withdiverse types of credit and voluntary savingsproducts in a sustainable way. Since its inceptionin 1991, it has been a pioneer in offering depositservices. BT’s experiences are especiallyimpressive since several other MFIs in Bangladeshhave failed or scaled down deposit services due tohigh costs of operation.Through the critical input from external advisors andextensive feedback from customer focus groups,BT has developed six types of loans and threesavings products, summarized in Figure 1. Thedistinct features of BT’s products include flexibilityand variety, and unbundling of loans from savingsproducts. To be a member of BT, one does nothave to borrow; saving will suffice.OutreachSince 1995, BT has grown significantly in size,client coverage, and products offered, whilefocusing its attention at the low-end of the market.Until 1998, BT followed a horizontal growth strategyby moving into new areas to increase outreach. Inthe face of increasing competition, however, BTthen resorted to deepening its coverage of existingmarkets (Figure 2). New products were developedto meet the demand for financial services.The floods in 1998, indeed, put BT’s products,especially flexible savings to test. While severalcenters suffered from loan delinquencies, overallthe organization survived the disaster in fairly goodshape. In fact, after a brief period of decline, theaverage savings balance increased dramatically.Almost all of BT’s depositors save less than US$1 aweek, which suggests that BT is servinghouseholds with very limited disposable income.Figure 1: Summary of BT’s Savings and Credit ProductsSavingsGeneral SavingsContractualSavingsOne-time FixedDepositsLoansGeneral LoanSupplementaryLoanLine of CreditSanitation LoanBusiness orProject LoanDisaster LoanThis open access savings facility allows members to deposit more than the expected 10 taka (20 cents) everyweek and to access their savings any number of times without penalty. There is no ceiling on the amount ofdeposits or withdrawals. Annual interest rate is 7.5 percent.With these time deposits, members and associate members agree to save a fixed amount every week ormonth for a fixed period of time – 3, 5 or 10 years. The annual compound interest rates vary from 9 to 14%based on the length of the contract. Early withdrawals incur a penalty and failure to deposit threeconsecutive installments will result in transfer of funds to general savings.These are certificates of deposit for a large amount (minimum US$100) deposited at the beginning of thecontract period for a fixed term up to 5 years. These deposits earn 9 to 12 percent interest per annum, basedon the length of the contract.This product is available to all members and is repayable in fifty consecutive equal installments. The loandisbursed ranges from US$20 to US$1,200.These are available to general loan borrowers, six months after paying their dues, for an amount up to half ofthe original general loan.A line of credit is available to long-term clients with established businesses. The current ceiling is US$2,000for a period of two to three years, renewable each year.This is for building sanitary facilities or for drilling tube wells. The ceiling is US$50.This new product is offered to members who can use larger loans to create jobs in the community. Loansizes vary from US$2,000 to US$5,000 for a period of two years.This special loan facility is available during disasters for members who have lost their businesses and areunable to repay loan installments. Current ceiling is US$40 repayable in two years.All loans are charged an annual interest rate of 20 percent except the disaster loan at 5 percent. Except for line of credit andbusiness loans, a member can have up to two loans at a time. However, disaster loans are available to every member regardlessof the type and number of loans outstanding at the time of disaster. All are collateral free but group based loans.<strong>MICROBANKING</strong> <strong>BULLETIN</strong>, SEPTEMBER 2000 23