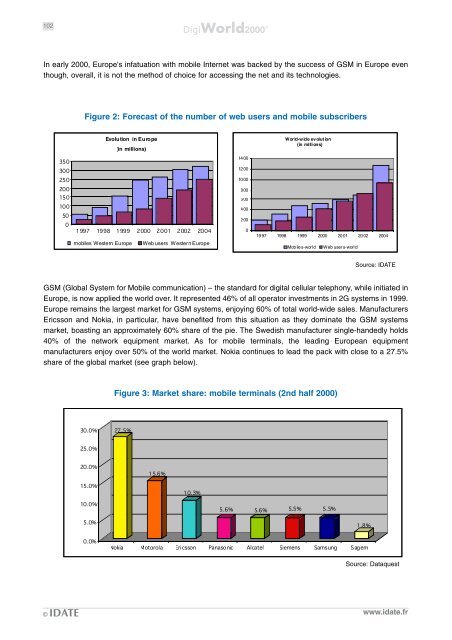

102World2000 In early 2000, Europe's infatuation with mobile Internet was backed by the success of GSM in Europe eventhough, overall, it is not the method of choice for accessing the net and its technologies.Figure 2: Forecast of the number of web users and mobile subscribersEvolution in Europe(in millions)World-wide evolution(in millions)14 0012 0010 00 mobiles Western Europe Web users Western Europe800600400200019 97 1998 1999 2000 20 01 20 02 2004Mobiles-worldWeb users-worldSource: IDATEGSM (Global System for Mobile communication) – the standard for digital cellular telephony, while initiated inEurope, is now applied the world over. It represented 46% of all operator investments in 2G systems in 1999.Europe remains the largest market for GSM systems, enjoying 60% of total world-wide sales. ManufacturersEricsson and Nokia, in particular, have benefited from this situation as they dominate the GSM systemsmarket, boasting an approximately 60% share of the pie. The Swedish manufacturer single-handedly holds40% of the network equipment market. As for mobile terminals, the leading European equipmentmanufacturers enjoy over 50% of the world market. Nokia continues to lead the pack with close to a 27.5%share of the global market (see graph below).Figure 3: Market share: mobile terminals (2nd half 2000) Source: Dataquest© IDATE www.idate.fr

World2000 103Furthermore, European mobile subscribers totalled 245 million, compared to 105 million in the US, in late2000. By 2004, three-quarters of Western Europe's population will be using cellular telephony services.It must be said, however, that while the mobile penetration rate in the US was close to 40% at the end of lastyear (37.5% in September 2000), compared with 62.9%(39,7% in December 99) for Europe, Americamaintains a much higher rate of use of pocket computers and PDAs which now enable wirelesscommunications. According to Gartner, annual world-wide sales of PDAs are expected to increase from 9.4million units in 2000 to 33.7 million units in 2004, keeping in mind that close to half of those sales will takeplace in the States. Additionally, the diversification of terminals should, at term, make for more opencompetition (among North American PC and PDA manufacturers as well as Japanese audiovisual specialists),while the increasing significance of data and IP could open up the equipment market to players such as Cisco.In early 2000, Europe was geared up for the prospects that mobile Internet was offering, reflected in:- a schedule, if not a set timetable, for the progressive deployment of technologies enabling increasinglypowerful platforms (WAP, GRPS, UMTS,….),- an immediate commitment to the UMTS licence allocation procedures in Europe.Faltering WAPDeveloped with the support of mobile manufacturers with an eye on renewing their deployed base, WAP(Wireless Application Protocol) was quick to woo mobile network operators as they were facing stiffcompetition on their national markets as well as a gradual decrease in ARPU (Average Revenue Per User).WAP was given a quick launch, touted via futuristic-style advertising campaigns, but the pioneer servicesproved disappointing to users who had expected to be able to surf the web on their mobiles. WAP servicescontinue to resemble early Videotex or teletext services rather than real web pages. Added to this deceptivecommunication was the under-estimation of the difficulties involved in launching a new technology on themarket, as well as the positioning of the services. Among the various factors which accumulated, makingWAP's launch a relative failure, of particular note are:- delays in the terminals' availability in addition to their poor performance,- slow connection time, linked in part to the GSM platform circuit,- limited speeds which cannot enable the graphic interfaces to which web users are accustomed,- the poor quality of the initial services due to the hasty launch and a non-exist market segmentation. Itappears that operators under-estimated the adaptations required to be made to those services whichwere responsible for the net's success, coming up against the mobiles' ergonomic constraints given theirlow bit rates. They also failed to take proper account of the specific assets that mobile Internet could haverepresented (see insert on mobile Internet's assets). Of particular note is the locating function which,while deemed highly promising for a number of applications, is still in its early stages of development.Lastly, a debate between mobile network operators, who want to maximum visibility, if not exclusivity, for theirportal of services, and content or bouquet editors, who want to see open platforms available to all, has servedto bring to the fore the uncertainties surrounding the regulatory and business model which will prevail.In this context, then, the WAP market developed much less significantly than had been expected in early 2000.France Telecom's WAP subscribers number some 450,000 on its domestic market, for close to a millionterminals in use. BT, which had high hopes for WAP, has not managed to attract more than a million users forits WAP compatible terminal.These issues sometimes gave rise to questions regarding WAP's pertinence for handling mobile informationservices. Operators and service providers alike are focusing on the performance offered by their voiceservices and particularly on the still under-exploited possibilities of SMS systems, along with users' recent© IDATE www.idate.fr