Poland

RE_Guide_2016_final

RE_Guide_2016_final

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Polish Real Estate Market<br />

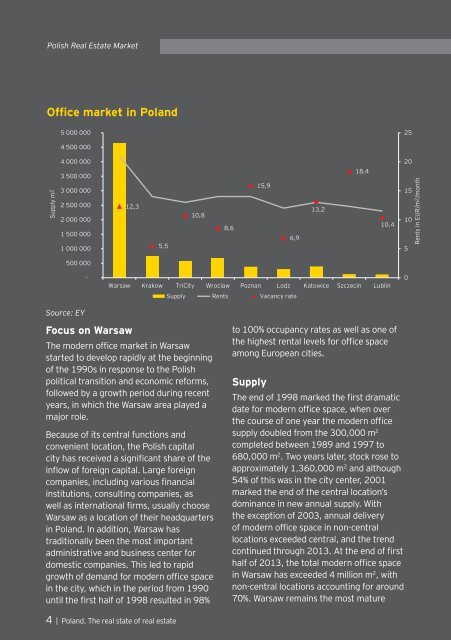

Office market in <strong>Poland</strong><br />

5 000 000<br />

25<br />

4 500 000<br />

Supply m 2<br />

4 000 000<br />

3 500 000<br />

3 000 000<br />

2 500 000<br />

2 000 000<br />

1 500 000<br />

1 000 000<br />

12,3<br />

5,5<br />

10,8<br />

8,6<br />

15,9<br />

6,9<br />

13,2<br />

18,4<br />

10,4<br />

20<br />

15<br />

10<br />

5<br />

Rents in EUR/m 2 /month<br />

500 000<br />

-<br />

Warsaw Krakow TriCity Wroclaw Poznan Lodz Katowice Szczecin Lublin<br />

Supply Rents Vacancy rate<br />

0<br />

Source: EY<br />

Focus on Warsaw<br />

The modern office market in Warsaw<br />

started to develop rapidly at the beginning<br />

of the 1990s in response to the Polish<br />

political transition and economic reforms,<br />

followed by a growth period during recent<br />

years, in which the Warsaw area played a<br />

major role.<br />

Because of its central functions and<br />

convenient location, the Polish capital<br />

city has received a significant share of the<br />

inflow of foreign capital. Large foreign<br />

companies, including various financial<br />

institutions, consulting companies, as<br />

well as international firms, usually choose<br />

Warsaw as a location of their headquarters<br />

in <strong>Poland</strong>. In addition, Warsaw has<br />

traditionally been the most important<br />

administrative and business center for<br />

domestic companies. This led to rapid<br />

growth of demand for modern office space<br />

in the city, which in the period from 1990<br />

until the first half of 1998 resulted in 98%<br />

to 100% occupancy rates as well as one of<br />

the highest rental levels for office space<br />

among European cities.<br />

Supply<br />

The end of 1998 marked the first dramatic<br />

date for modern office space, when over<br />

the course of one year the modern office<br />

supply doubled from the 300,000 m 2<br />

completed between 1989 and 1997 to<br />

680,000 m 2 . Two years later, stock rose to<br />

approximately 1,360,000 m 2 and although<br />

54% of this was in the city center, 2001<br />

marked the end of the central location’s<br />

dominance in new annual supply. With<br />

the exception of 2003, annual delivery<br />

of modern office space in non-central<br />

locations exceeded central, and the trend<br />

continued through 2013. At the end of first<br />

half of 2013, the total modern office space<br />

in Warsaw has exceeded 4 million m 2 , with<br />

non-central locations accounting for around<br />

70%. Warsaw remains the most mature<br />

4 | <strong>Poland</strong>. The real state of real estate