Staatsolie Annual Report 2017

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Confidence in Our Own Abilities<br />

26<br />

<strong>Report</strong> on the Audit of the Consolidated Financial Statements<br />

(Continued)<br />

Key audit matters<br />

(Continued)<br />

We have fulfilled the responsibilities described in the Auditor’s responsibilities for the audit of the<br />

consolidated financial statements section of our report, including in relation to these matters.<br />

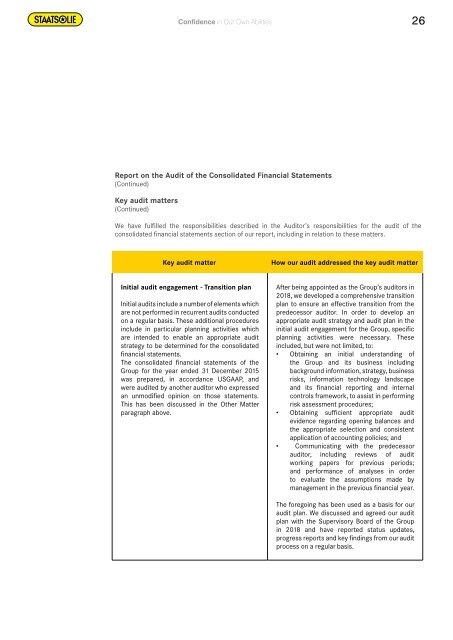

Key audit matter<br />

How our audit addressed the key audit matter<br />

Initial audit engagement - Transition plan<br />

Initial audits include a number of elements which<br />

are not performed in recurrent audits conducted<br />

on a regular basis. These additional procedures<br />

include in particular planning activities which<br />

are intended to enable an appropriate audit<br />

strategy to be determined for the consolidated<br />

financial statements.<br />

The consolidated financial statements of the<br />

Group for the year ended 31 December 2015<br />

was prepared, in accordance USGAAP, and<br />

were audited by another auditor who expressed<br />

an unmodified opinion on those statements.<br />

This has been discussed in the Other Matter<br />

paragraph above.<br />

After being appointed as the Group’s auditors in<br />

2018, we developed a comprehensive transition<br />

plan to ensure an effective transition from the<br />

predecessor auditor. In order to develop an<br />

appropriate audit strategy and audit plan in the<br />

initial audit engagement for the Group, specific<br />

planning activities were necessary. These<br />

included, but were not limited, to:<br />

• Obtaining an initial understanding of<br />

the Group and its business including<br />

background information, strategy, business<br />

risks, information technology landscape<br />

and its financial reporting and internal<br />

controls framework, to assist in performing<br />

risk assessment procedures;<br />

• Obtaining sufficient appropriate audit<br />

evidence regarding opening balances and<br />

the appropriate selection and consistent<br />

application of accounting policies; and<br />

• Communicating with the predecessor<br />

auditor, including reviews of audit<br />

working papers for previous periods;<br />

and performance of analyses in order<br />

to evaluate the assumptions made by<br />

management in the previous financial year.<br />

The foregoing has been used as a basis for our<br />

audit plan. We discussed and agreed our audit<br />

plan with the Supervisory Board of the Group<br />

in 2018 and have reported status updates,<br />

progress reports and key findings from our audit<br />

process on a regular basis.