Staatsolie Annual Report 2017

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Confidence in Our Own Abilities<br />

70<br />

<strong>Staatsolie</strong> Maatschappij Suriname N.V.<br />

<strong>Staatsolie</strong> Maatschappij Suriname N.V.<br />

Notes to the Consolidated financial statements for the years ended December 31, <strong>2017</strong> and 2016<br />

(continued) Notes to the Consolidated financial statements for the years ended December 31, <strong>2017</strong> and 2016<br />

(continued)<br />

Available-for-sale (AFS) financial investments<br />

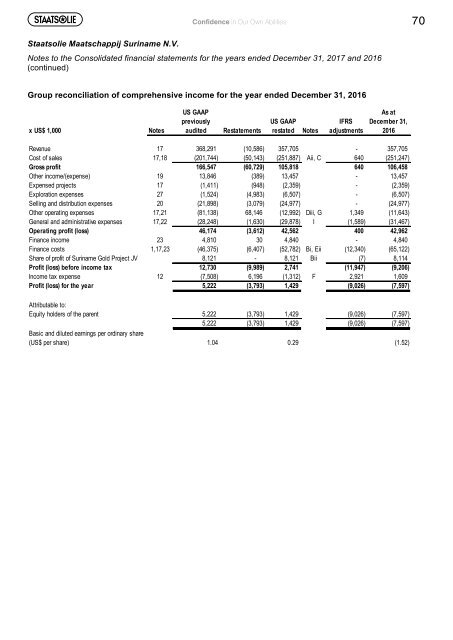

Group reconciliation of comprehensive income for the year ended December 31, 2016<br />

AFS financial investments include equity and debt securities. Equity investments classified as availablefor-sale<br />

are those neither classified as held-for-trading previously nor designated US GAAP at fair value through IFRS profit December or loss. 31,<br />

US GAAP<br />

As at<br />

x US$ 1,000<br />

Notes audited Restatements restated Notes adjustments 2016<br />

After initial measurement, AFS financial investments are subsequently measured at fair value with<br />

unrealized Revenue gains or losses recognized 17 as OCI 368,291 until the investment (10,586) 357,705 is derecognized, at which - time, 357,705 the<br />

Cost of sales 17,18 (201,744) (50,143) (251,887) Aii, C 640 (251,247)<br />

cumulative<br />

Gross profit<br />

gain or loss is recognized in other<br />

166,547<br />

operating<br />

(60,729)<br />

income<br />

105,818<br />

or expense, or the<br />

640<br />

investment<br />

106,458<br />

is<br />

determined Other income/(expense) to be impaired, at which 19time, the cumulative 13,846 loss (389) is reclassified 13,457 to the consolidated - statement 13,457<br />

Expensed projects 17 (1,411) (948) (2,359) - (2,359)<br />

of Exploration profit or expenses loss in finance costs and 27 removed from (1,524) the OCI. (4,983) The Group (6,507) evaluates its AFS - financial assets (6,507)<br />

to Selling determine and distribution whether expenses the ability and 20 intention to (21,898) sell them in the (3,079) near term (24,977) is still appropriate. - (24,977)<br />

Other operating expenses 17,21 (81,138) 68,146 (12,992) Diii, G 1,349 (11,643)<br />

General and administrative expenses 17,22 (28,248) (1,630) (29,878) I (1,589) (31,467)<br />

Operating profit (loss) 46,174 (3,612) 42,562 400 42,962<br />

(ii) Financial liabilities<br />

Finance income 23 4,810 30 4,840 - 4,840<br />

Finance costs 1,17,23 (46,375) (6,407) (52,782) Bi, Eii (12,340) (65,122)<br />

Recognition and measurement<br />

Share of profit of Suriname Gold Project JV 8,121 - 8,121 Bii (7) 8,114<br />

Financial Profit (loss) before liabilities income are taxclassified, at initial recognition, 12,730 as financial (9,989) liabilities 2,741 at fair value (11,947) through profit (9,206) or<br />

Income tax expense 12 (7,508) 6,196 (1,312) F 2,921 1,609<br />

loss, loans and borrowings, payables, as appropriate. All financial liabilities are recognized initially at fair<br />

Profit (loss) for the year 5,222 (3,793) 1,429 (9,026) (7,597)<br />

value and, in the case of loans and borrowings and payables, net of directly attributable transaction costs.<br />

Attributable to:<br />

The Group’s financial liabilities include trade and other payables, loans and borrowings including bank<br />

Equity holders of the parent 5,222 (3,793) 1,429 (9,026) (7,597)<br />

overdrafts.<br />

5,222 (3,793) 1,429 (9,026) (7,597)<br />

Basic and diluted earnings per ordinary share<br />

(US$ per share) 1.04 0.29 (1.52)<br />

Loans and borrowings<br />

This is the category most relevant to the Group. After initial recognition, interest bearing loans and<br />

borrowings are subsequently measured at amortized cost using the EIR method. Gains and losses are<br />

recognized in the consolidated statement of profit or loss when the liabilities are derecognized as well as<br />

through the EIR amortization process. Amortized cost is calculated by taking into account any discount or<br />

premium on acquisition and fees or costs that are an integral part of the EIR. The EIR amortization is<br />

included in finance costs in the consolidated statement of profit or loss. This category generally applies to<br />

interest-bearing loans and borrowings.<br />

m. Inventories<br />

Petroleum products are valued at the lower of cost and net realizable value.<br />

Raw materials:<br />

• Purchase cost is valued on weighted average method<br />

Finished goods and work in progress:<br />

• Cost of direct materials and labor and a proportion of manufacturing overheads based on normal<br />

operating capacity but excluding borrowing costs<br />

Page 62<br />

Page 70