TOTT 14 February 2019

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

10 Talk of the Town ADVERTISING / NEWSDESK: (046) 624 4356 Find us on Facebook <strong>February</strong> <strong>14</strong>, <strong>2019</strong> ADVERTISING / NEWSDESK: (046) 624 4356 Find us on Facebook<br />

Talk of the Town 11<br />

advertising feature<br />

advertising feature<br />

A world of financial and legal services at your fingertips<br />

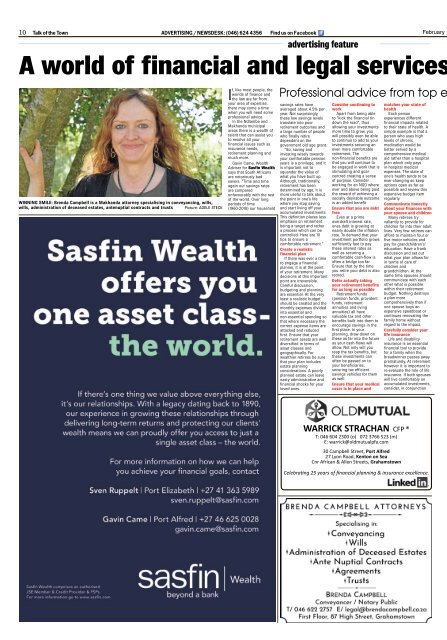

WINNING SMILE: Brenda Campbell is a Makhanda attorney specialising in conveyancing, wills,<br />

wills, administration of deceased estates, antenuptial contracts and trusts Picture: ADELE STECK<br />

If, like most people, the<br />

worlds of finance and<br />

the law are far from<br />

your area of expertise,<br />

there may come a time<br />

when you will need some<br />

professional advice.<br />

In the Ndlambe and<br />

Makhanda municipal<br />

areas there is a wealth of<br />

talent that can assist you<br />

to resolve all your<br />

financial issues such as<br />

insurance needs,<br />

retirement planning and<br />

much more.<br />

Gavin Came, Wealth<br />

Adviser for Sasfin Wealth<br />

says that South Africans<br />

are notoriously bad<br />

savers. “Time and time<br />

again our savings rates<br />

are compared<br />

unfavourably with the rest<br />

of the world. Over long<br />

periods of time<br />

(1960-2018) our household<br />

Professional advice from top experts in their various fields<br />

savings rates have<br />

averaged about 4.5% per<br />

year. Not surprisingly,<br />

these low savings levels<br />

translate into poor<br />

retirement outcomes and<br />

a large number of people<br />

who finally retire<br />

dependent on the<br />

government old age grant.<br />

“So, saving and<br />

investing wisely towards<br />

your comfortable pension<br />

years is a privilege, and it<br />

is important not to<br />

squander the value of<br />

what you have built up.<br />

Although, traditionally,<br />

retirement has been<br />

determined by age, it is<br />

more useful to talk about<br />

the point in one’s life<br />

where you stop saving<br />

and start living off your<br />

accumulated investments.<br />

This definition places less<br />

emphasis on retirement<br />

being a target and rather<br />

a process which can be<br />

controlled. Here are 10<br />

tips to ensure a<br />

comfortable retirement.”<br />

Create a realistic<br />

financial plan<br />

If there was ever a time<br />

to engage a financial<br />

planner, it is at the point<br />

of your retirement. Many<br />

decisions at this important<br />

point are irreversible.<br />

Careful discussion,<br />

budgeting and planning<br />

are essential. At the very<br />

least a realistic budget<br />

should be created and the<br />

monthly expenses divided<br />

into essential and<br />

non-essential spending so<br />

that where necessary the<br />

correct expense items are<br />

attacked and reduced<br />

first. Ensure that your<br />

retirement assets are well<br />

diversified in terms of<br />

asset classes and<br />

geographically. For<br />

wealthier retirees be sure<br />

that your plan includes<br />

estate planning<br />

considerations. A poorly<br />

planned estate can leave<br />

nasty administrative and<br />

financial shocks for your<br />

loved ones.<br />

Consider continuing to<br />

work<br />

Apart from being able<br />

to “kick the financial tin<br />

down the road”, thus<br />

allowing your investments<br />

more time to grow, you<br />

will possibly even be able<br />

to continue to add to your<br />

investments securing an<br />

even more comfortable<br />

retirement. The<br />

non-financial benefits are<br />

that you will continue to<br />

be engaged in work that is<br />

stimulating and goalcentred<br />

creating a sense<br />

of purpose. Consider<br />

working for an NGO where<br />

over and above being paid<br />

the reward of achieving a<br />

socially desirable outcome<br />

is an added benefit<br />

Ensure that you are debt<br />

free<br />

Even at a prime<br />

overdraft interest rate,<br />

ones debt is growing at<br />

nearly double the inflation<br />

rate. To demand that your<br />

investment portfolio grows<br />

sufficiently fast to pay<br />

these interest rates as<br />

well as securing a<br />

comfortable cash-flow is<br />

often a bridge too far.<br />

Ensure that by the time<br />

you retire your debt is also<br />

retired.<br />

Defer actually taking<br />

your retirement benefits<br />

for as long as possible<br />

Retirement funds<br />

(pension funds, provident<br />

funds, retirement<br />

annuities and living<br />

annuities) all have<br />

valuable tax and other<br />

benefits built into them to<br />

encourage savings in the<br />

first place. In your<br />

planning, draw down on<br />

these as far into the future<br />

as your cash-flows will<br />

allow. Not only will you<br />

reap the tax benefits, but<br />

these investments can<br />

often be passed on to<br />

your beneficiaries,<br />

securing tax efficient<br />

savings vehicles for them<br />

as well.<br />

Ensure that your medical<br />

cover is in place and<br />

matches your state of<br />

health<br />

Each person<br />

experiences different<br />

financial impacts related<br />

to their state of health. A<br />

simple example is that a<br />

person who uses high<br />

levels of chronic<br />

medication would be<br />

better served by a<br />

comprehensive medical<br />

aid rather than a hospital<br />

plan which only pays<br />

in-hospital medical<br />

expenses. The state of<br />

one’s health tends to be<br />

ever-changing so keep<br />

options open as far as<br />

possible and review this<br />

expensive budget item<br />

r e g u l a r l y.<br />

Communicate honestly<br />

about your finances with<br />

your spouse and children<br />

Many retirees try<br />

valiantly to provide for<br />

children far into their adult<br />

lives. Very few retirees can<br />

afford to maintain four or<br />

five motor vehicles and<br />

pay for grandchildren’s’<br />

education. Have a frank<br />

discussion and set out<br />

what your plan allows for<br />

in terms of care of<br />

children and<br />

grandchildren. At the<br />

same time spouses should<br />

communicate with each<br />

other what is possible<br />

within their retirement<br />

budget. Nothing destroys<br />

a plan more<br />

comprehensively than if<br />

one spouse buys an<br />

expensive speedboat or<br />

continues renovating the<br />

family home without<br />

regard to the impact.<br />

Carefully consider your<br />

life insurance<br />

Life and disability<br />

insurance is an essential<br />

financial tool to provide<br />

for a family when the<br />

breadwinner passes away<br />

prematurely. At retirement<br />

however it is important to<br />

re-evaluate the role of life<br />

insurance. If both spouses<br />

will live comfortably on<br />

accumulated investments,<br />

consider, in conjunction<br />

WARRICK STRACHAN CFP ®<br />

T: 046 604 2300 (o) 072 3766 523 (m)<br />

E: warrick@oldmutualpfa.com<br />

30 Campbell Street, Port Alfred<br />

27 Lyon Road, Kenton on Sea<br />

Cnr African & Allen Streets, Grahamstown<br />

with your adviser,<br />

cancelling life insurance in<br />

favour of other budget<br />

items.<br />

Don’t forget about<br />

i n f l at i o n<br />

Inflation is an evil<br />

phenomenon that creeps<br />

up on the most<br />

well-funded retirement<br />

plan. Although the official<br />

government inflation rate<br />

is well monitored and is a<br />

critical financial tool for a<br />

number of purposes, each<br />

of us has our own<br />

personal inflation rate<br />

based on what we spend<br />

our money on. As one gets<br />

older, for example,<br />

medical costs including<br />

medical aids become a<br />

bigger and bigger<br />

proportion of our monthly<br />

spend. Over the years<br />

medical inflation has<br />

operated at 2-3<br />

percentage points higher<br />

than the published<br />

inflation rate. And we<br />

h av e n ’t even spoken about<br />

E s ko m .<br />

Keep reviewing your<br />

plan<br />

Your financial<br />

circumstances in<br />

retirement will be<br />

constantly changing. Over<br />

a year you could spend<br />

more or less than<br />

originally planned. You<br />

could face unforeseen<br />

capital expenses, perhaps<br />

a new car or a medical<br />

emergency, or receive an<br />

unexpected inheritance. It<br />

is therefore essential that<br />

the original plan is<br />

reviewed at least annually.<br />

Don’t keep up with the<br />

Joneses<br />

One last point, at this<br />

stage, of all times in one<br />

life, do not succumb to<br />

“keeping up with the<br />

Joneses”. Funding a trip<br />

to Mauritius with your<br />

mates, which is not<br />

covered by your plan, is a<br />

no-no. A bring-and-braai<br />

party may well be your<br />

only way of reciprocating<br />

rather than a dinner at a<br />

fancy restaurant and<br />

sharing a hefty bill. Ensure<br />

that you live within your<br />

means and within your<br />

plan. Plan your retirement<br />

by speaking to your Sasfin<br />

Wealth Adviser or Portfolio<br />

Manager about our global<br />

solutions, for at Sasfin<br />

Wealth we offer you one<br />

asset class – the world.<br />

At Old Mutual, “We run<br />

my financial planning<br />

practice using integrated<br />

wealth planning principles<br />

as our guiding process,”<br />

said executive financial<br />

adviser Warrick Strachan.<br />

“This entails using a<br />

financial goal-based<br />

planning process in which<br />

our customers the central<br />

and most important figure<br />

and who prioritise their<br />

goals and dreams. A<br />

financial needs analysis<br />

follows, solutions<br />

recommended and when<br />

the customer is satisfied,<br />

solutions are<br />

implemented. A critical<br />

component is the ongoing<br />

and regular review<br />

process to ensure the<br />

implemented solutions<br />

continue to meet the<br />

c u st o m e r ’s objectives and<br />

BENASURE<br />

BROKERS<br />

BK/CC<br />

CK90/19680/23<br />

Korttermynversekeringsmakelaars<br />

Short Term Insurance Brokers<br />

FIA Lid/ Member # 02006027<br />

FSP: 13586<br />

10 Hancorn Lane/Hancornlaan 10<br />

Port Alfred 6170<br />

Tel: 046 624 1524<br />

Faks/Fax: 086 697 4208<br />

Petro: 082 8242 937<br />

E-pos/mail:benadej@mweb.co.za<br />

to set new goals.<br />

“As a trusted partner in<br />

our client’s lives over the<br />

past 25 years we strive to<br />

remain relevant by<br />

complying with the<br />

stringent requirements of<br />

the Financial Planning<br />

Institute, utilising the<br />

support and infrastructure<br />

of SA’s biggest and most<br />

trusted financial services<br />

brands, Old<br />

Mutual.”<br />

Their Port Alfred offices<br />

are at 30 Campbell Street<br />

where they are open<br />

Monday to Friday 9am to<br />

4pm. They also have<br />

offices in Grahamstown.<br />

Everyone needs legal<br />

advice at some time or<br />

other. Whether for an<br />

antenuptual contract or<br />

litigation, having an<br />

attorney on your side to<br />

offer advice and to fight<br />

your case for you if<br />

necessar y.<br />

Woolgar Attorneys do<br />

mainly conveyancing,<br />

estates, commercial work,<br />

collections, litigation and<br />

wills. Barry Woollgar was<br />

admitted as an attorney<br />

28 years ago and moved<br />

his practice to Port Alfred<br />

in 2012.<br />

For any legal<br />

requirements feel free to<br />

contact our offices. See<br />

the advert.<br />

Short-term insurance<br />

brokers with almost 30<br />

years’ experience to back<br />

them up, Benasure<br />

Brokers specialise in<br />

personal and business<br />

insurance, contract works<br />

and liability as well as<br />

all-risk insurance for<br />

plant.<br />

Call Petro Benade for<br />

assistance with revisions<br />

to your current insurance<br />

portfolio, or ask for a<br />

comparative quotation to<br />

see how much you can<br />

save on your current<br />

short-term insurance<br />

policies. Ask for current<br />

and outstanding claims or<br />

just for general advice on<br />

all your short-term<br />

insurance needs. Visit<br />

Benasure Brokers at 10<br />

Hancorn Lane in Port<br />

Alfred or phone on<br />

082-824-2937 or 046-<br />

624-1524.<br />

HMB Attorneys (HM<br />

Botha) was founded in<br />

1990 in Gauteng, with its<br />

head office in Midrand.<br />

The firm opened the<br />

Port Alfred branch office<br />

in 2018. The Port Alfred<br />

office is under the control<br />

of Marietjie Robb, who is<br />

an attorney, notary and<br />

conveyancer with 32<br />

years’ experience.<br />

“Our partners and staff<br />

are passionate about law<br />

and provide a friendly,<br />

personal and professional<br />

ser vice,” said Robb. “Our<br />

Port Alfred branch<br />

specialises in property<br />

law, property<br />

development,<br />

conveyancing, estate<br />

planning, wills,<br />

administration of estates<br />

and general contracts,<br />

including antenuptial<br />

contracts as well as<br />

mining law.<br />

“We believe in<br />

supporting the local<br />

community and look<br />

forward to becoming a<br />

part of it.”<br />

FOR FRIENDLY AND<br />

EFFICIENT SERVICE,<br />

CONTACT US FOR<br />

ALL YOUR LEGAL<br />

REQUIREMENTS.<br />

TAKING PART: Posing for a photo after taking part in the recent Rotary Swim-a-thon were the Seeff<br />

team of, from left, Antony de Bruin, Catelyn Lewis, Ella Funde and Mia Marias Picture: NTOMBI MSUTU<br />

PROUD MOMENT: Taking some time out after judging the recent Swim-a-Thon at the Port Alfred<br />

High School Pool were, from left, Lion president Francois de Klerk, Rotarian Tina Hon, Lion Neville<br />

Williamson, Sheena Louca, and Rotarians Hans Hon and Mike Millard Picture: NTOMBI MSUTU<br />

MC DUTIES: Lion Neville Williamson with Port<br />

Alfred High School head of marketing Laura<br />

Guest at the Rotary Swim-a-thon held at the<br />

Port Alfred High School pool recently<br />

Picture: NTOMBI MSUTU<br />

WATER FOR OUR NEIGHBOURS: Port Alfred High<br />

School Grade 2 pupil Kourtney Wright was one<br />

of many who brought water to school this past<br />

week as part of the school’s efforts to assist<br />

pupils in Makhanda who are in serious need.<br />

Members of the public are welcome to send or<br />

drop off water at the front office between<br />

7.30am and 3pm, Monday to Friday<br />

ĞůĞďĂŶŐĞĂŽĨĮŶĂŶĐŝĂůůĂŶŶŝŶŐΘŝŶĂŶĐĞĞĐĞůůĞŶĐĞ<br />

SHOES COLLECTION: Head girl of Port Alfred<br />

High School, Lynn Baatjies, recently handed<br />

over a collection of shoes to Temba Tele of<br />

Confident Girls. The collection began with the<br />

2018 matrics at the end of last year and<br />

included sports shoes from several pupils in<br />

other grades at the start of this year. Temba<br />

will distribute to those in need<br />

PAHS CARNIVAL LAUNCH: The annual major<br />

fundraiser for Port Alfred High School has got<br />

off to a flying start with every pupil now selling<br />

raffle tickets for a Trolley Dash sponsored by<br />

the Rosehill SUPERSPAR. Grade 2 pupil Matthew<br />

Steck is counting down the days until the PAHS<br />

Carnival and Food Fair takes place on Friday<br />

March 1 from 3pm until 6pm on the school<br />

fields