Contents - Tanzania Revenue Authority

Contents - Tanzania Revenue Authority

Contents - Tanzania Revenue Authority

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

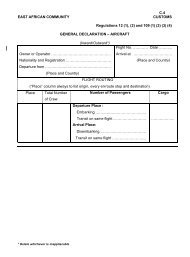

Example 6 Calculations<br />

Note: The Excise duty 10%*: The rate is imposed on Non- utility<br />

vehicles with engine capacity of more than 2,000 cc and with<br />

less than ten years from the year of manufacture.<br />

7.3 INCOME TAX<br />

In order to obtain import duty to be paid,<br />

take the certified customs value and<br />

multiply by the import duty rate (25%).<br />

USD 3,800 x 25% = USD 950<br />

USD 950 x TZS 1,300 =<br />

In order to obtain excise duty value, take<br />

the certified customs value plus import<br />

duty calculated in (i). Then multiply by<br />

the excise duty rate (10 %)<br />

USD (3,800+950) = USD 4,750<br />

USD 4,750 x 10% =USD475<br />

USD 475 x TZS 1,300=<br />

In order to get the value of VAT, take the<br />

certified value and add to it the import<br />

duty and the excise duty you have<br />

calculated in (ii). Then multiply by the<br />

VAT rate (20%).<br />

USD (4750+475) = USD5225<br />

USD5225 x 20% = USD 1,045<br />

USD 1,045 x TZS1300= TZS 1,358,500/=<br />

7.3.1 The Income tax is a tax on gains or profits from person’s<br />

income from employment, business or ownership of property<br />

and an investments in corporations and other entities<br />

• Income from employment<br />

The total income of each person is determined separately.<br />

This includes salaried people who are taxed at<br />

progressive individual income tax rate that varies from the<br />

lowest marginal rate of 18.5% to the top marginal rate of<br />

30%. Benefits in kind are also to be included in<br />

determining the taxable income of an employee.<br />

31