Introduzione al corso di Analisi delle Serie Temporali

Introduzione al corso di Analisi delle Serie Temporali

Introduzione al corso di Analisi delle Serie Temporali

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

An<strong>al</strong>isi <strong>Serie</strong> Tempor<strong>al</strong>i<br />

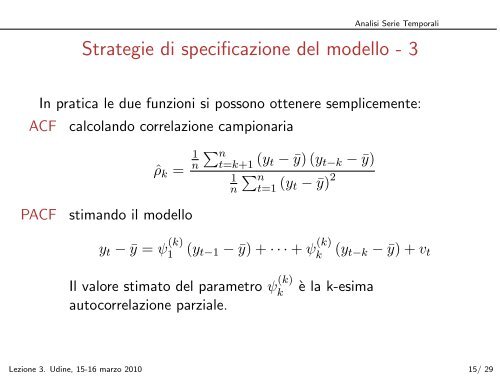

Strategie <strong>di</strong> specificazione del modello - 3<br />

In pratica le due funzioni si possono ottenere semplicemente:<br />

ACF c<strong>al</strong>colando correlazione campionaria<br />

ˆρk =<br />

PACF stimando il modello<br />

1 n n<br />

t=k+1 (yt − ¯y) (yt−k − ¯y)<br />

1<br />

n<br />

n<br />

t=1 (yt − ¯y) 2<br />

yt − ¯y = ψ (k)<br />

1 (yt−1 − ¯y) + · · · + ψ (k)<br />

k (yt−k − ¯y) + vt<br />

Il v<strong>al</strong>ore stimato del parametro ψ (k)<br />

k è la k-esima<br />

autocorrelazione parzi<strong>al</strong>e.<br />

Lezione 3. U<strong>di</strong>ne, 15-16 marzo 2010 15/ 29