Introduzione al corso di Analisi delle Serie Temporali

Introduzione al corso di Analisi delle Serie Temporali

Introduzione al corso di Analisi delle Serie Temporali

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

An<strong>al</strong>isi <strong>Serie</strong> Tempor<strong>al</strong>i<br />

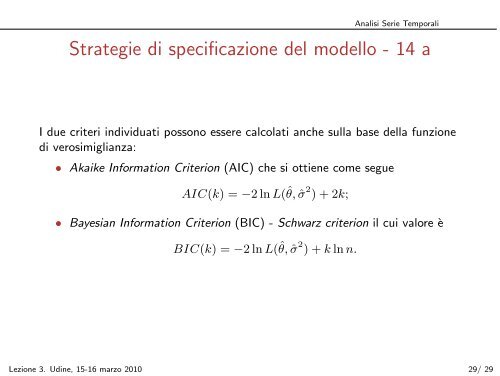

Strategie <strong>di</strong> specificazione del modello - 14 a<br />

I due criteri in<strong>di</strong>viduati possono essere c<strong>al</strong>colati anche sulla base della funzione<br />

<strong>di</strong> verosimiglianza:<br />

• Akaike Information Criterion (AIC) che si ottiene come segue<br />

AIC(k) = −2 ln L( ˆ θ, ˆσ 2 ) + 2k;<br />

• Bayesian Information Criterion (BIC) - Schwarz criterion il cui v<strong>al</strong>ore è<br />

BIC(k) = −2 ln L( ˆ θ, ˆσ 2 ) + k ln n.<br />

Lezione 3. U<strong>di</strong>ne, 15-16 marzo 2010 29/ 29