Istruzioni per la compilazione della D.S.E. - Città di Torino

Istruzioni per la compilazione della D.S.E. - Città di Torino

Istruzioni per la compilazione della D.S.E. - Città di Torino

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

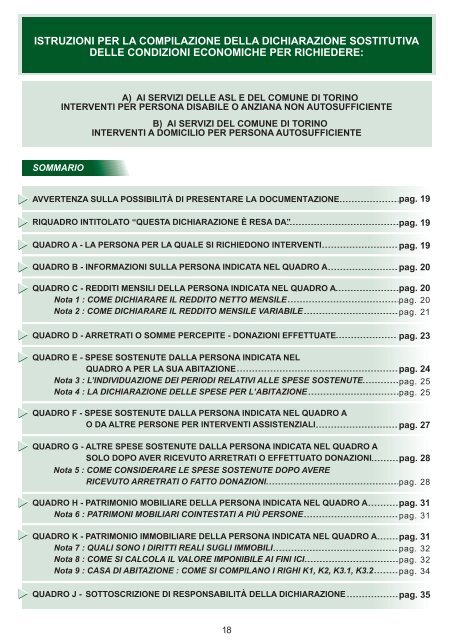

ISTRUZIONI PER LA COMPILAZIONE DELLA DICHIARAZIONE SOSTITUTIVA<br />

DELLE CONDIZIONI ECONOMICHE PER RICHIEDERE:<br />

SOMMARIO<br />

A) AI SERVIZI DELLE ASL E DEL COMUNE DI TORINO<br />

INTERVENTI PER PERSONA DISABILE O ANZIANA NON AUTOSUFFICIENTE<br />

B) AI SERVIZI DEL COMUNE DI TORINO<br />

INTERVENTI A DOMICILIO PER PERSONA AUTOSUFFICIENTE<br />

AVVERTENZA SULLA POSSIBILITÀ DI PRESENTARE LA DOCUMENTAZIONE<br />

RIQUADRO INTITOLATO “QUESTA DICHIARAZIONE È RESA DA”<br />

QUADRO A - LA PERSONA PER LA QUALE SI RICHIEDONO INTERVENTI<br />

QUADRO B - INFORMAZIONI SULLA PERSONA INDICATA NEL QUADRO A<br />

QUADRO C - REDDITI MENSILI DELLA PERSONA INDICATA NEL QUADRO A<br />

Nota 1 : COME DICHIARARE IL REDDITO NETTO MENSILE<br />

Nota 2 : COME DICHIARARE IL REDDITO MENSILE VARIABILE<br />

QUADRO D - ARRETRATI O SOMME PERCEPITE - DONAZIONI EFFETTUATE<br />

QUADRO E - SPESE SOSTENUTE DALLA PERSONA INDICATA NEL<br />

QUADRO A PER LA SUA ABITAZIONE<br />

Nota 3 : L’INDIVIDUAZIONE DEI PERIODI RELATIVI ALLE SPESE SOSTENUTE<br />

Nota 4 : LA DICHIARAZIONE DELLE SPESE PER L’ABITAZIONE<br />

QUADRO F - SPESE SOSTENUTE DALLA PERSONA INDICATA NEL QUADRO A<br />

O DA ALTRE PERSONE PER INTERVENTI ASSISTENZIALI<br />

QUADRO G - ALTRE SPESE SOSTENUTE DALLA PERSONA INDICATA NEL QUADRO A<br />

SOLO DOPO AVER RICEVUTO ARRETRATI O EFFETTUATO DONAZIONI<br />

Nota 5 : COME CONSIDERARE LE SPESE SOSTENUTE DOPO AVERE<br />

RICEVUTO ARRETRATI O FATTO DONAZIONI<br />

QUADRO H - PATRIMONIO MOBILIARE DELLA PERSONA INDICATA NEL QUADRO A<br />

Nota 6 : PATRIMONI MOBILIARI COINTESTATI A PIÙ PERSONE<br />

QUADRO K - PATRIMONIO IMMOBILIARE DELLA PERSONA INDICATA NEL QUADRO A<br />

Nota 7 : QUALI SONO I DIRITTI REALI SUGLI IMMOBILI<br />

Nota 8 : COME SI CALCOLA IL VALORE IMPONIBILE AI FINI ICI<br />

Nota 9 : CASA DI ABITAZIONE : COME SI COMPILANO I RIGHI K1, K2, K3.1, K3.2<br />

QUADRO J - SOTTOSCRIZIONE DI RESPONSABILITÀ DELLA DICHIARAZIONE<br />

18<br />

pag. 19<br />

pag. 19<br />

pag. 19<br />

pag. 20<br />

pag. 20<br />

pag. 20<br />

pag. 21<br />

pag. 23<br />

pag. 24<br />

pag. 25<br />

pag. 25<br />

pag. 27<br />

pag. 28<br />

pag. 28<br />

pag. 31<br />

pag. 31<br />

pag. 31<br />

pag. 32<br />

pag. 32<br />

pag. 34<br />

pag. 35

AVVERTENZA SULLA POSSIBILITA’ DI PRESENTARE LA DOCUMENTAZIONE<br />

Chiunque presenta <strong>la</strong> <strong>di</strong>chiarazione può scegliere se preferisce:<br />

• presentare al Servizio sociale <strong>la</strong> <strong>di</strong>chiarazione compi<strong>la</strong>ta, senza portare le copie dei documenti<br />

che attestano il possesso <strong>di</strong> red<strong>di</strong>ti, dei beni, delle spese (ad esempio le ricevute dell’affitto, del<strong>la</strong><br />

pensione riscossa, ecc…) e <strong>di</strong> tutto quanto descritto nel<strong>la</strong> <strong>di</strong>chiarazione<br />

• oppure portare al Servizio sociale anche questi documenti, <strong>per</strong> farsi aiutare dal Servizio a<br />

compi<strong>la</strong>re <strong>la</strong> <strong>di</strong>chiarazione.<br />

RIQUADRO INTITOLATO “QUESTA DICHIARAZIONE E’ RESA DA”<br />

Nel riquadro intito<strong>la</strong>to “QUESTA DICHIARAZIONE E’ RESA DA” si devono in<strong>di</strong>care i dati del<strong>la</strong><br />

<strong>per</strong>sona che compi<strong>la</strong> e firma <strong>la</strong> <strong>di</strong>chiarazione. Chi firma <strong>la</strong> <strong>di</strong>chiarazione è il <strong>di</strong>chiarante, che può<br />

essere:<br />

1) <strong>la</strong> stessa <strong>per</strong>sona del Quadro A che richiede gli interventi<br />

2) oppure una <strong>per</strong>sona <strong>di</strong>versa dal<strong>la</strong> <strong>per</strong>sona del Quadro A se <strong>la</strong> <strong>per</strong>sona del Quadro A (che<br />

deve ricevere gli interventi), <strong>per</strong> motivi <strong>di</strong> salute non può temporaneamente compi<strong>la</strong>re e firmare<br />

<strong>la</strong> <strong>di</strong>chiarazione; in questo caso al suo posto e nel suo interesse:<br />

2.1) <strong>la</strong> <strong>di</strong>chiarazione può essere compi<strong>la</strong>ta e firmata soltanto dai seguenti suoi parenti e soltanto<br />

nel seguente or<strong>di</strong>ne: il coniuge, i figli (se manca il coniuge), i parenti in linea retta o col<strong>la</strong>terale<br />

fino al terzo grado (se non vi sono figli), che sono: i genitori, i nonni, i nipoti (cioè i figli dei figli),<br />

i fratelli, gli zii, i cugini.<br />

ESEMPIO: Una signora, che è vedova, ha una mano fratturata: <strong>per</strong>tanto <strong>per</strong> motivi <strong>di</strong> salute<br />

non può temporaneamente né compi<strong>la</strong>re né sottoscrivere <strong>la</strong> <strong>di</strong>chiarazione. Poiché essendo<br />

vedova non ha marito che può <strong>di</strong>chiarare <strong>per</strong> lei, <strong>la</strong> figlia può compi<strong>la</strong>re e firmare <strong>la</strong><br />

<strong>di</strong>chiarazione nell’interesse del<strong>la</strong> madre: quin<strong>di</strong> nel riquadro intito<strong>la</strong>to “QUESTA DICHIARAZIONE<br />

E’ RESA DA” <strong>la</strong> figlia scrive i propri dati (e non quelli del<strong>la</strong> madre);<br />

2.2) al posto del<strong>la</strong> <strong>per</strong>sona del Quadro A e nel suo interesse, può compi<strong>la</strong>re e firmare <strong>la</strong> <strong>di</strong>chiarazione<br />

chi ne ha <strong>la</strong> rappresentanza legale: il suo Tutore, o ancora il suo Amministratore <strong>di</strong> Sostegno<br />

(entrambi nominati dal Giu<strong>di</strong>ce Tute<strong>la</strong>re).<br />

Se invece <strong>la</strong> <strong>per</strong>sona del Quadro A non ha parenti come quelli descritti sopra al punto 2.1),<br />

nell’interesse del<strong>la</strong> <strong>per</strong>sona del Quadro A un’altra <strong>per</strong>sona può consegnare ai Servizi copia dei<br />

documenti re<strong>la</strong>tivi al<strong>la</strong> con<strong>di</strong>zione economica del<strong>la</strong> <strong>per</strong>sona del Quadro A, invece <strong>di</strong> presentare<br />

<strong>la</strong> <strong>di</strong>chiarazione. In questo caso, chi presenta i documenti del<strong>la</strong> <strong>per</strong>sona del Quadro A<br />

non firma <strong>la</strong> <strong>di</strong>chiarazione, ma firma una ricevuta re<strong>la</strong>tiva ai documenti che ha consegnato<br />

al Servizio Sociale.<br />

QUADRO A - LA PERSONA PER LA QUALE SI RICHIEDONO INTERVENTI<br />

Nel Quadro A, il <strong>di</strong>chiarante deve scrivere i dati del<strong>la</strong> <strong>per</strong>sona che deve ricevere l’intervento <strong>per</strong><br />

il quale viene presentata questa <strong>di</strong>chiarazione.<br />

ATTENZIONE: Chi compi<strong>la</strong> e firma questa <strong>di</strong>chiarazione (ossia il <strong>di</strong>chiarante) deve scrivere in tutti<br />

i quadri del<strong>la</strong> <strong>di</strong>chiarazione i dati che riguardano <strong>la</strong> <strong>per</strong>sona che deve avere l’intervento, ossia <strong>la</strong><br />

<strong>per</strong>sona del Quadro A.<br />

ESEMPIO: La figlia che compi<strong>la</strong> e firma <strong>la</strong> <strong>di</strong>chiarazione al posto del<strong>la</strong> madre è <strong>la</strong> <strong>di</strong>chiarante,<br />

e deve scrivere dal Quadro A al Quadro K i dati che riguardano <strong>la</strong> madre. Al Quadro J, <strong>la</strong><br />

figlia sottoscrive <strong>la</strong> <strong>di</strong>chiarazione <strong>di</strong> responsabilità.<br />

19

QUADRO B - INFORMAZIONI SULLA PERSONA INDICATA NEL QUADRO A<br />

1) Il <strong>di</strong>chiarante deve fare una croce su SI o NO e scrivere le informazioni richieste<br />

2) Il <strong>di</strong>chiarante deve in<strong>di</strong>care (con una croce sul SI o sul NO) se <strong>la</strong> <strong>per</strong>sona del Quadro A ha una<br />

invali<strong>di</strong>tà civile, ossia se si è sottoposta al<strong>la</strong> visita presso <strong>la</strong> Commissione Me<strong>di</strong>ca <strong>per</strong> gli Invali<strong>di</strong><br />

Civili presso l’ASL, e l’ASL le ha consegnato un certificato con <strong>la</strong> <strong>per</strong>centuale <strong>di</strong> invali<strong>di</strong>tà civile<br />

riconosciuta. Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere qui questa <strong>per</strong>centuale.<br />

3) Il <strong>di</strong>chiarante deve in<strong>di</strong>care (con una croce sul SI o sul NO) se <strong>la</strong> <strong>per</strong>sona del Quadro A ha una<br />

delle seguenti indennità:<br />

• indennità <strong>di</strong> accompagnamento: è l’indennità pagata dall’INPS alle <strong>per</strong>sone che hanno bisogno<br />

<strong>di</strong> assistenza continua. E’ data anche ai ciechi assoluti;<br />

• indennità <strong>di</strong> comunicazione: è l’indennità data ai sordomuti <strong>di</strong> età maggiore <strong>di</strong> 12 anni che<br />

hanno <strong>per</strong>so più <strong>di</strong> 75 decibel <strong>di</strong> u<strong>di</strong>to ed ai minori <strong>di</strong> 12 anni che abbiano <strong>per</strong>so almeno 60 decibel<br />

<strong>di</strong> u<strong>di</strong>to;<br />

• indennità <strong>di</strong> frequenza: assegno mensile dato dall’INPS ai minori invali<strong>di</strong> civili che frequentano<br />

le scuole o altre attività.<br />

Se il <strong>di</strong>chiarante fa una croce sul NO deve scrivere (con una croce sul SI o NO successivo) se<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A ha presentato <strong>la</strong> domanda presso l’ASL <strong>per</strong> richiedere una <strong>di</strong> queste<br />

indennità.<br />

QUADRO C - REDDITI MENSILI DELLA PERSONA INDICATA NEL QUADRO A<br />

Nel Quadro C il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo dei red<strong>di</strong>ti che <strong>la</strong> <strong>per</strong>sona del Quadro A riceve<br />

nel mese in cui si presenta <strong>la</strong> <strong>di</strong>chiarazione.<br />

Il <strong>di</strong>chiarante NON deve <strong>di</strong>chiarare (e quin<strong>di</strong> non deve scriverne gli importi):<br />

• l'indennità <strong>di</strong> accompagnamento erogata dall'I.N.P.S.;<br />

• l’indennità <strong>di</strong> frequenza erogata dall’INPS ai minori con <strong>di</strong>fficoltà a svolgere funzioni proprie<br />

dell'età;<br />

• l'indennità <strong>di</strong> comunicazione e le indennità <strong>per</strong> cecità parziale e assoluta;<br />

• le ren<strong>di</strong>te <strong>per</strong> inabilità <strong>per</strong>manente, silicosi e asbestosi, anche <strong>per</strong> i su<strong>per</strong>stiti, e gli assegni<br />

<strong>per</strong>sonali <strong>per</strong> assistenza erogati dall'I.N.A.I.L.;<br />

• gli assegni terapeutici erogati dai servizi psichiatrici delle A.S.L.;<br />

• le tre<strong>di</strong>cesime mensilità <strong>di</strong> pensioni, indennità e stipen<strong>di</strong>.<br />

Nota 1: COME DICHIARARE IL REDDITO NETTO MENSILE<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo dei red<strong>di</strong>ti netti del<strong>la</strong> <strong>per</strong>sona del Quadro A ricevuti nel mese<br />

in cui presenta <strong>la</strong> <strong>di</strong>chiarazione.<br />

Se quando il <strong>di</strong>chiarante presenta <strong>la</strong> <strong>di</strong>chiarazione <strong>la</strong> <strong>per</strong>sona del Quadro A non ha ancora<br />

<strong>per</strong>cepito nessuno dei red<strong>di</strong>ti descritti nel Quadro C, ma li riceverà nel mese in corso, il <strong>di</strong>chiarante<br />

deve in<strong>di</strong>care i red<strong>di</strong>ti <strong>per</strong>cepiti nel mese precedente dal<strong>la</strong> <strong>per</strong>sona del Quadro A. Tale evento<br />

capita <strong>di</strong> solito quando il <strong>di</strong>chiarante compi<strong>la</strong> <strong>la</strong> <strong>di</strong>chiarazione nei primi giorni del mese.<br />

ESEMPIO 1: La <strong>per</strong>sona del Quadro A compi<strong>la</strong> <strong>la</strong> <strong>di</strong>chiarazione il giorno 1° luglio 2006. In<br />

tale data non ha ancora ricevuto <strong>la</strong> sua pensione <strong>per</strong> il mese <strong>di</strong> luglio. Al Quadro C del<strong>la</strong><br />

<strong>di</strong>chiarazione <strong>di</strong>chiara <strong>per</strong>ciò l’importo che ha ricevuto a giugno 2006. Se nel mese in cui<br />

presenta <strong>la</strong> <strong>di</strong>chiarazione <strong>la</strong> <strong>per</strong>sona del Quadro A ha ricevuto red<strong>di</strong>ti <strong>di</strong> importo <strong>di</strong>verso<br />

rispetto a quelli che riceve in tutti gli altri mesi (ad esempio a causa <strong>di</strong> conguagli straor<strong>di</strong>nari)<br />

allora il <strong>di</strong>chiarante deve scrivere l’importo che <strong>la</strong> <strong>per</strong>sona del Quadro A riceve <strong>di</strong> solito.<br />

ESEMPIO 2: La <strong>per</strong>sona del Quadro A riceve uno stipen<strong>di</strong>o mensile da red<strong>di</strong>to <strong>di</strong> <strong>la</strong>voro<br />

<strong>di</strong>pendente <strong>di</strong> Euro 850,00. La <strong>per</strong>sona del Quadro A presenta <strong>la</strong> <strong>di</strong>chiarazione il 28/01/2007.<br />

In questo mese il suo stipen<strong>di</strong>o è stato <strong>di</strong> Euro 400,00 a causa <strong>di</strong> conguaglio fiscale annuale.<br />

20

Allora il <strong>di</strong>chiarante deve scrivere l’importo <strong>di</strong> Euro 850,00 (somma che solitamente riceve<br />

ogni mese <strong>la</strong> <strong>per</strong>sona del Quadro A) e non l’importo <strong>di</strong> Euro 400,00, in quanto 400,00 è una<br />

somma che non rappresenta il suo stipen<strong>di</strong>o consueto. Infatti nel mese <strong>di</strong> febbraio riceverà<br />

nuovamente uno stipen<strong>di</strong>o <strong>di</strong> Euro 850,00.<br />

Questi red<strong>di</strong>ti devono essere netti, cioè senza le trattenute fiscali e contributive. Il <strong>di</strong>chiarante<br />

non deve invece sottrarre dai red<strong>di</strong>ti altri tipi <strong>di</strong> spese, come <strong>la</strong> cessione <strong>di</strong> stipen<strong>di</strong>,<br />

pagamento <strong>di</strong> mutui, alimenti pagati al coniuge <strong>di</strong>vorziato, iscrizione a Sindacati o Associazioni.<br />

ESEMPIO 3: La <strong>per</strong>sona del Quadro A riceve al mese Euro 420,00 <strong>di</strong> pensione. Su questi<br />

Euro 420,00 ha una trattenuta <strong>di</strong> Euro 15,00 <strong>per</strong> iscrizioni al Sindacato. Il <strong>di</strong>chiarante deve<br />

scrivere Euro 420,00 e NON Euro 405,00.<br />

Rigo C1<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

red<strong>di</strong>ti provenienti da ogni tipo <strong>di</strong> pensione, compresi l’invali<strong>di</strong>tà e <strong>la</strong> reversibilità (pensione che<br />

viene data al<strong>la</strong> moglie o ai figli oppure ai nipoti minorenni se erano mantenuti dal defunto che<br />

prendeva <strong>la</strong> pensione). Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere l’importo netto che<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A riceve al mese (ve<strong>di</strong> <strong>la</strong> Nota 1, pag. 20), il tipo <strong>di</strong> pensione e l’Ente<br />

(ad esempio l’INPS) che paga questa pensione.<br />

Rigo C2<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

red<strong>di</strong>ti da <strong>la</strong>voro <strong>di</strong>pendente o simili, ad esempio red<strong>di</strong>ti da <strong>la</strong>vori socialmente utili, da contratto<br />

<strong>di</strong> appren<strong>di</strong>stato o <strong>di</strong> inserimento, da svolgimento <strong>di</strong> <strong>la</strong>vori a progetto, da borsa <strong>di</strong> stu<strong>di</strong>o, borsa<br />

<strong>di</strong> <strong>la</strong>voro o simili, da svolgimento <strong>di</strong> carica <strong>di</strong> amministratore, sindaco o revisore <strong>di</strong> società, da soci<br />

<strong>di</strong> coo<strong>per</strong>ative <strong>di</strong> produzione e <strong>la</strong>voro/<strong>di</strong> servizi/agricole, dal<strong>la</strong> cassa integrazione guadagni/<br />

indennità <strong>di</strong> mobilità/indennità <strong>di</strong> <strong>di</strong>soccupazione, indennità <strong>di</strong> maternità (data dall’INPS in sostituzione<br />

del<strong>la</strong> retribuzione alle <strong>la</strong>voratrici in stato <strong>di</strong> gravidanza <strong>per</strong> 5 mesi), indennità <strong>di</strong> ma<strong>la</strong>ttia (pagata<br />

dall’INPS ai <strong>la</strong>voratori in ma<strong>la</strong>ttia). Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere l’importo<br />

netto che <strong>la</strong> <strong>per</strong>sona del Quadro A riceve al mese (ve<strong>di</strong> <strong>la</strong> Nota 1, pag. 20), il tipo <strong>di</strong> red<strong>di</strong>to e il<br />

nominativo e in<strong>di</strong>rizzo del datore <strong>di</strong> <strong>la</strong>voro o dell’Ente che lo paga.<br />

Rigo C3<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

red<strong>di</strong>ti da partecipazione a società, imprese o associazioni (somme che riceve <strong>per</strong>ché ha una<br />

partecipazione, ossia possiede una quota <strong>di</strong> una società <strong>di</strong> <strong>per</strong>sone, <strong>di</strong> un’associazione<br />

oppure <strong>di</strong> un’impresa familiare). Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere il tipo <strong>di</strong><br />

red<strong>di</strong>to e il nominativo del<strong>la</strong> società/impresa/associazione in cui ha <strong>la</strong> partecipazione.<br />

Poiché tali red<strong>di</strong>ti non si ricevono tutti i mesi, se il <strong>di</strong>chiarante ha messo <strong>la</strong> crocetta sul SI <strong>per</strong><br />

scrivere l’importo deve procedere come descritto al<strong>la</strong> Nota 2 qui sotto.<br />

Nota 2: COME DICHIARARE IL REDDITO MENSILE VARIABILE<br />

Se l’importo del red<strong>di</strong>to che <strong>la</strong> <strong>per</strong>sona del Quadro A riceve al mese è variabile, cioè tutti i mesi<br />

non ha sempre il medesimo importo, allora il <strong>di</strong>chiarante deve scrivere <strong>la</strong> me<strong>di</strong>a degli importi che<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A ha avuto nei 6 mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

ESEMPIO: Dichiarazione presentata <strong>per</strong> <strong>la</strong> richiesta dell’intervento il 1° luglio 2006. Red<strong>di</strong>ti<br />

da partecipazione ricevuti dal<strong>la</strong> <strong>per</strong>sona del Quadro A nei 6 mesi precedenti a tale data:<br />

Febbraio 2006 ricevuti Euro 250,00 / Marzo 2006 ricevuti Euro 300,00 / Aprile 2006 ricevuti<br />

Euro 150,00 / Maggio 2006 ricevuti Euro 230,00 / Giugno 2006 ricevuti Euro 180,00.<br />

Il totale delle somme ricevute è: Euro (250+300+150+230+180)= 1.110,00.<br />

La me<strong>di</strong>a si ottiene <strong>di</strong>videndo il totale delle somme <strong>per</strong> il numero <strong>di</strong> mesi (ossia 6):<br />

Euro 1.110,00 / 6 = 185,00 e questo è l’importo da scrivere nel<strong>la</strong> <strong>di</strong>chiarazione.<br />

Rigo C4<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

red<strong>di</strong>ti da <strong>la</strong>voro autonomo o d’impresa, cioè riceve somme dallo svolgimento <strong>di</strong> <strong>la</strong>voro autonomo<br />

(ad esempio è un agente <strong>di</strong> commercio o un libero professionista), oppure <strong>per</strong>ché è tito<strong>la</strong>re <strong>di</strong><br />

un’impresa (<strong>di</strong>tta in<strong>di</strong>viduale, ad esempio è commerciante). Il <strong>di</strong>chiarante deve inoltre scrivere le<br />

21

somme che <strong>la</strong> <strong>per</strong>sona del Quadro A ha ricevuto <strong>per</strong> lo svolgimento <strong>di</strong> col<strong>la</strong>borazioni occasionali,<br />

consulenze, gettoni <strong>di</strong> presenza in assemblee. Se mette una croce sul SI, il <strong>di</strong>chiarante deve<br />

scrivere l’importo netto che <strong>la</strong> <strong>per</strong>sona del Quadro A riceve nel mese in cui presenta <strong>la</strong> <strong>di</strong>chiarazione<br />

(ve<strong>di</strong> <strong>la</strong> Nota 1, pag. 20), il tipo <strong>di</strong> attività che <strong>la</strong> <strong>per</strong>sona del Quadro A svolge e il nominativo e<br />

l’in<strong>di</strong>rizzo dell’impresa.<br />

Se l’importo del red<strong>di</strong>to del<strong>la</strong> <strong>per</strong>sona del Quadro A è variabile, allora il <strong>di</strong>chiarante deve scrivere<br />

<strong>la</strong> me<strong>di</strong>a degli importi degli ultimi 6 mesi (ve<strong>di</strong> <strong>la</strong> Nota 2, pag. 21).<br />

Rigo C5<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce sul SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A riceve<br />

denaro come interessi dai capitali investiti: <strong>di</strong>viden<strong>di</strong> (red<strong>di</strong>ti che si ricevono dal possesso <strong>di</strong> azioni<br />

<strong>di</strong> società <strong>di</strong> capitali), red<strong>di</strong>ti <strong>di</strong> quote <strong>di</strong> fon<strong>di</strong> comuni <strong>di</strong> investimento, interessi maturati sui conti<br />

correnti (bancari o postali), interessi ricevuti da BOT, CCT o altri titoli pubblici che <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A possiede, interessi ricevuti da titoli privati (obbligazioni <strong>di</strong> società), somme ricevute<br />

dall’investimento in assicurazioni o ancora altre ren<strong>di</strong>te finanziarie.<br />

Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere l’importo netto che <strong>la</strong> <strong>per</strong>sona del Quadro<br />

A riceve nel mese in cui presenta <strong>la</strong> <strong>di</strong>chiarazione (ve<strong>di</strong> <strong>la</strong> Nota 1, pag. 20), il tipo <strong>di</strong> red<strong>di</strong>to che<br />

riceve e il nominativo e l’in<strong>di</strong>rizzo dell’ufficio/banca/ gestore del capitale.<br />

Se l’importo del red<strong>di</strong>to che <strong>la</strong> <strong>per</strong>sona del Quadro A ottiene al mese è variabile, allora il <strong>di</strong>chiarante<br />

deve scrivere <strong>la</strong> me<strong>di</strong>a degli importi degli ultimi 6 mesi (ve<strong>di</strong> <strong>la</strong> Nota 2, pag. 21)<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è 25/06/2006. Il 14/05/2006 <strong>la</strong> <strong>per</strong>sona del Quadro A<br />

ha ricevuto Euro 650,00 dal<strong>la</strong> cedo<strong>la</strong> <strong>di</strong> interessi <strong>di</strong> CCT e in data 15/02/2006 ha ricevuto<br />

Euro 1.000,00 come interessi da obbligazioni private. Al Rigo C5) il <strong>di</strong>chiarante deve scrivere<br />

Euro 275,00, derivante dal<strong>la</strong> somma dei due importi incassati (dato che entrambi sono stati<br />

incassati nei 6 mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione) <strong>di</strong>viso 6 mesi.<br />

Euro (650+1000)= Euro 1.650,00 / 6 = Euro 275,00.<br />

Rigo C6<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A riceve<br />

denaro da fabbricati o da terreni, ossia riceve somme dall’utilizzo da parte <strong>di</strong> altre <strong>per</strong>sone <strong>di</strong><br />

fabbricati o terreni <strong>di</strong> sua proprietà o <strong>di</strong> suo usufrutto (ad esempio riceve denaro <strong>per</strong>ché ha affittato<br />

un suo terreno o un suo fabbricato). Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere l’importo<br />

netto che <strong>la</strong> <strong>per</strong>sona del Quadro A riceve nel mese in cui presenta <strong>la</strong> <strong>di</strong>chiarazione (ve<strong>di</strong> <strong>la</strong> Nota 1,<br />

pag. 20), i tipi <strong>di</strong> immobili che gli procurano questo danaro (terreni o fabbricati) e il luogo dove si<br />

trovano.<br />

Se l’importo del red<strong>di</strong>to che <strong>la</strong> <strong>per</strong>sona del Quadro A ottiene al mese è variabile, allora il<br />

<strong>di</strong>chiarante deve scrivere <strong>la</strong> me<strong>di</strong>a degli importi degli ultimi 6 mesi (ve<strong>di</strong> <strong>la</strong> Nota 2, pag. 21).<br />

ESEMPIO 1: La <strong>per</strong>sona del Quadro A è proprietaria <strong>di</strong> una casa a Foggia; ha dato in affitto<br />

questa casa e riceve Euro 250,00 ogni mese. Il <strong>di</strong>chiarante nel Rigo C6, dove c’è scritto<br />

“Fabbricati costituiti da:” deve in<strong>di</strong>care il tipo <strong>di</strong> fabbricato (abitazione) e l’in<strong>di</strong>rizzo in cui si<br />

trova <strong>la</strong> casa e dove c’è scritto “Importo mensile” deve in<strong>di</strong>care l’importo <strong>di</strong> Euro 250,00.<br />

ESEMPIO 2: La <strong>per</strong>sona del Quadro A è usufruttuaria <strong>di</strong> un terreno a Cosenza; l’ha affittato<br />

e riceve Euro 150,00 ogni mese. Il <strong>di</strong>chiarante nel Rigo C6, dove c’è scritto “Terreni non<br />

e<strong>di</strong>ficabili ed agricoli:” deve in<strong>di</strong>care il tipo <strong>di</strong> terreno (agricolo) e l’in<strong>di</strong>rizzo in cui si trova il<br />

terreno e dove c’è scritto “Importo mensile” deve in<strong>di</strong>care l’importo <strong>di</strong> Euro 150,00.<br />

Rigo C7<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

altre entrate, quali assegni dal coniuge separato o <strong>di</strong>vorziato, aiuti monetari da parenti o conoscenti,<br />

sussi<strong>di</strong> dello Stato o da altri Enti Pubblici (assistenza economica del Comune, assegni <strong>di</strong> maternità<br />

statali ed ai nuclei numerosi, altri bonus), red<strong>di</strong>ti che ottiene dallo svolgimento <strong>di</strong> attività agricole.<br />

Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere l’importo netto che <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A riceve nel mese in cui presenta <strong>la</strong> <strong>di</strong>chiarazione (ve<strong>di</strong> <strong>la</strong> Nota 1, pag. 20).<br />

Nelle altre righe del Rigo C7 il <strong>di</strong>chiarante può aggiungere altri red<strong>di</strong>ti mensili che eventualmente<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A <strong>per</strong>cepisce, <strong>di</strong>versi da quelli elencati nelle righe precedenti.<br />

Se l’importo del red<strong>di</strong>to che <strong>la</strong> <strong>per</strong>sona del Quadro A ottiene al mese è variabile, allora il <strong>di</strong>chiarante<br />

deve scrivere <strong>la</strong> me<strong>di</strong>a degli importi degli ultimi 6 mesi (ve<strong>di</strong> <strong>la</strong> Nota 2, pag. 21).<br />

22

QUADRO D - ARRETRATI O SOMME PERCEPITE - DONAZIONI EFFETTUATE<br />

Nel Quadro D il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo degli arretrati <strong>di</strong> red<strong>di</strong>ti mensili e/o somme in<br />

denaro <strong>di</strong>fferenti dai red<strong>di</strong>ti mensili che <strong>la</strong> <strong>per</strong>sona del Quadro A ha ricevuto.<br />

Inoltre, il <strong>di</strong>chiarante deve in<strong>di</strong>care le donazioni che <strong>la</strong> <strong>per</strong>sona del Quadro A ha effettuato nei 24<br />

mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

Rigo D1 - Arretrati<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

ricevuto arretrati o liquidazioni <strong>di</strong> stipen<strong>di</strong> o pensioni, ossia vecchie mensilità che non le erano<br />

state pagate prima, compreso il trattamento <strong>di</strong> fine rapporto (cioè <strong>la</strong> liquidazione che viene data<br />

al<strong>la</strong> cessazione <strong>di</strong> un rapporto <strong>di</strong> <strong>la</strong>voro).<br />

Il <strong>di</strong>chiarante deve scrivere questi importi solo se <strong>la</strong> <strong>per</strong>sona del Quadro A li ha incassati<br />

ENTRO I 6 MESI che precedono <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione che il <strong>di</strong>chiarante sta compi<strong>la</strong>ndo.<br />

Se sono stati <strong>per</strong>cepiti prima <strong>di</strong> 6 mesi da questa data, non vanno <strong>di</strong>chiarati.<br />

Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care il tipo <strong>di</strong> arretrato (ad esempio arretrati <strong>di</strong><br />

pensione) che <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato, <strong>la</strong> data <strong>di</strong> riscossione e l’importo ricevuto.<br />

Se nei 6 mesi <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato più arretrati il <strong>di</strong>chiarante deve in<strong>di</strong>carli tutti.<br />

ESEMPIO 1: La <strong>di</strong>chiarazione ha data 25/06/2006; <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato il<br />

15/04/2006 Euro 500,00 <strong>di</strong> arretrati <strong>di</strong> stipen<strong>di</strong>o. Questo importo (Euro 500,00) deve essere<br />

scritto <strong>per</strong>ché incassato nei 6 mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

ESEMPIO 2: La <strong>di</strong>chiarazione ha data 12/07/2006; <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato il<br />

25/11/2005 Euro 2.300,00 <strong>di</strong> trattamento <strong>di</strong> fine rapporto <strong>di</strong> <strong>la</strong>voro. Questo importo<br />

(Euro 2.300,00) NON deve essere scritto, <strong>per</strong>ché <strong>la</strong> <strong>per</strong>sona del Quadro A lo ha incassato<br />

oltre i 6 mesi dal<strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

Rigo D2 - Somme in denaro <strong>di</strong>versi dai red<strong>di</strong>ti mensili<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

ricevuto somme in denaro <strong>di</strong>verse da arretrati <strong>di</strong> pensioni o stipen<strong>di</strong>, ossia <strong>di</strong>verse dalle somme<br />

in<strong>di</strong>cate al Rigo D1: ad esempio, <strong>per</strong> risarcimenti derivanti da assicurazioni o vertenze sindacali,<br />

<strong>per</strong> liquidazioni (<strong>di</strong>verse dal Trattamento <strong>di</strong> fine rapporto), <strong>per</strong> ere<strong>di</strong>tà in denaro, <strong>per</strong> ven<strong>di</strong>ta <strong>di</strong><br />

beni immobili (fabbricati e/o terreni), <strong>per</strong> ven<strong>di</strong>ta <strong>di</strong> beni mobili (ad esempio automobili, motociclette,<br />

titoli azionari, obbligazioni pubbliche o private, quote <strong>di</strong> fon<strong>di</strong>, ecc..).<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care anche gli importi che <strong>la</strong> <strong>per</strong>sona del Quadro A ha ricevuto dal Fondo<br />

Nazionale <strong>per</strong> il Sostegno al<strong>la</strong> Locazione Legge n. 431/98 (contributo che è dato dal Comune <strong>per</strong><br />

aiutare le <strong>per</strong>sone a bassi red<strong>di</strong>ti nel pagamento dell’affitto del<strong>la</strong> propria abitazione).<br />

Il <strong>di</strong>chiarante deve scrivere questi importi solo se <strong>la</strong> <strong>per</strong>sona del Quadro A li ha incassati NEI<br />

24 MESI che precedono <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione che il <strong>di</strong>chiarante sta compi<strong>la</strong>ndo.<br />

Se li ha <strong>per</strong>cepiti più <strong>di</strong> 24 mesi prima <strong>di</strong> questa data non vanno <strong>di</strong>chiarati. Se mette una<br />

croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care il tipo <strong>di</strong> somma che <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato,<br />

<strong>la</strong> data <strong>di</strong> incasso e l’importo. Se nei 24 mesi <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato più somme,<br />

il <strong>di</strong>chiarante deve in<strong>di</strong>carle tutte.<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è 15/07/2006; <strong>la</strong> <strong>per</strong>sona del Quadro A ha incassato: il<br />

18/10/2005 Euro 250,00 come risarcimento da assicurazione, il 09/02/2005 Euro 750,00 derivante<br />

dal<strong>la</strong> ven<strong>di</strong>ta <strong>di</strong> un’automobile, il 15/05/2004 Euro 600,00 come contributo Legge n. 431/98.<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care sia Euro 250,00 che Euro 750,00, <strong>per</strong>ché entrambi gli importi<br />

sono stati incassati dal<strong>la</strong> <strong>per</strong>sona del Quadro A nei 24 mesi precedenti <strong>la</strong> data del<strong>la</strong><br />

<strong>di</strong>chiarazione, ma NON deve in<strong>di</strong>care Euro 600,00 <strong>per</strong>ché <strong>la</strong> somma è stata incassata oltre<br />

i 24 mesi prima del<strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

Rigo D3 - Donazione <strong>di</strong> beni mobili<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

intestato o donato, ossia ha trasferito <strong>la</strong> proprietà <strong>di</strong> beni mobili (tutto ciò che non è immobile e<br />

quin<strong>di</strong> non è un terreno o un fabbricato) ad altre <strong>per</strong>sone senza ottenere denaro in cambio. Il<br />

<strong>di</strong>chiarante deve descrivere solo i beni mobili donati o intestati <strong>per</strong> <strong>la</strong> cui donazione o intestazione<br />

23

<strong>la</strong> <strong>per</strong>sona del Quadro A ha stipu<strong>la</strong>to un rego<strong>la</strong>re contratto <strong>di</strong> donazione o intestazione.<br />

Il <strong>di</strong>chiarante deve scrivere questi importi solo se <strong>la</strong> <strong>per</strong>sona del Quadro A li ha donati o intestati<br />

NEI 24 MESI che precedono <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione che il <strong>di</strong>chiarante sta compi<strong>la</strong>ndo.<br />

Se li ha donati o intestati più <strong>di</strong> 24 mesi prima <strong>di</strong> questa data non vanno <strong>di</strong>chiarati.<br />

Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care che cosa <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

intestato o donato, <strong>la</strong> data del<strong>la</strong> donazione o intestazione e il valore del bene donato o intestato,<br />

che è il valore scritto nel contratto <strong>di</strong> donazione o intestazione. Se nei 24 mesi <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A ha intestato o donato più beni mobili il <strong>di</strong>chiarante deve in<strong>di</strong>carli tutti.<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è 01/07/2006; <strong>la</strong> <strong>per</strong>sona del Quadro A ha donato: il<br />

10/5/2006 una motocicletta il cui valore scritto sul contratto <strong>di</strong> donazione è <strong>di</strong> Euro 550,00<br />

ed il 01/06/2004 ha donato un’automobile il cui valore scritto sul contratto <strong>di</strong> donazione è<br />

<strong>di</strong> Euro 1.000,00. Il <strong>di</strong>chiarante deve in<strong>di</strong>care in <strong>di</strong>chiarazione solo Euro 550,00 del<strong>la</strong><br />

donazione del<strong>la</strong> motocicletta, <strong>per</strong>ché <strong>la</strong> data del<strong>la</strong> donazione fatta dal<strong>la</strong> <strong>per</strong>sona del Quadro A è<br />

compresa nei 24 mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione, ma NON deve in<strong>di</strong>care Euro<br />

1.000,00 del<strong>la</strong> donazione dell’autovettura <strong>per</strong>ché <strong>la</strong> data del<strong>la</strong> donazione è oltre i 24 mesi<br />

prima del<strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

Rigo D4 - Donazione <strong>di</strong> beni immobili<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A<br />

ha intestato o donato, ossia ha trasferito <strong>la</strong> proprietà o l’usufrutto <strong>di</strong> beni immobili (cioè <strong>di</strong> terreni<br />

e fabbricati; ve<strong>di</strong> <strong>la</strong> Nota 7, pag. 32) ad altre <strong>per</strong>sone senza ottenere denaro in cambio.<br />

Il Dichiarante deve scrivere questi importi solo se <strong>la</strong> <strong>per</strong>sona del Quadro A li ha donati o<br />

intestati NEI 24 MESI che precedono <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione che il <strong>di</strong>chiarante sta<br />

compi<strong>la</strong>ndo. Se li ha donati/intestati più <strong>di</strong> 24 mesi prima <strong>di</strong> questa data non vanno <strong>di</strong>chiarati.<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è 25/06/2006; <strong>la</strong> <strong>per</strong>sona del Quadro A ha donato:<br />

il 18/04/2006 un alloggio il cui valore scritto sul contratto <strong>di</strong> donazione è <strong>di</strong> Euro 25.000,00<br />

ed il 25/03/2004 ha donato un terreno il cui valore scritto sul contratto <strong>di</strong> donazione è <strong>di</strong><br />

Euro 10.000,00.<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care so<strong>la</strong>mente Euro 25.000,00, valore del<strong>la</strong> donazione dell’alloggio,<br />

<strong>per</strong>ché <strong>la</strong> data <strong>di</strong> questa donazione fatta dal<strong>la</strong> <strong>per</strong>sona del Quadro A è compresa nei 24<br />

mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione, ma NON deve in<strong>di</strong>care Euro 10.000,00, valore<br />

del<strong>la</strong> donazione del terreno, poiché <strong>la</strong> data <strong>di</strong> questa donazione è oltre i 24 mesi prima del<strong>la</strong><br />

data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

Se mette una croce su SI, il <strong>di</strong>chiarante deve scrivere il tipo <strong>di</strong> beni immobili che <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A ha intestato o donato, <strong>la</strong> data del<strong>la</strong> donazione o intestazione ed il valore dell’immobile:<br />

questo valore è l’imponibile ai fini ICI del terreno o del fabbricato donato o intestato. Il modo <strong>per</strong><br />

trovare il valore imponibile ai fini ICI è in<strong>di</strong>cato al<strong>la</strong> Nota 8, pag. 32.<br />

Se esisteva un mutuo sul fabbricato o sul terreno donato o intestato, allora il <strong>di</strong>chiarante deve<br />

scrivere il valore imponibile ICI senza l’importo del mutuo che restava ancora da pagare al<strong>la</strong> data<br />

del contratto <strong>di</strong> donazione o intestazione.<br />

ESEMPIO: La <strong>per</strong>sona del Quadro A ha donato in data 13/02/2006 un fabbricato il cui valore<br />

imponibile ai fini ICI (calco<strong>la</strong>to come in<strong>di</strong>cato al<strong>la</strong> Nota 8, pag. 32) è <strong>di</strong> Euro 70.000,00.<br />

Ma al<strong>la</strong> data del<strong>la</strong> donazione su questo fabbricato deve ancora essere pagato un mutuo <strong>di</strong><br />

Euro 25.000,00.<br />

Chiunque debba pagare questo mutuo, il <strong>di</strong>chiarante deve scrivere come valore<br />

dell’immobile l’importo <strong>di</strong> Euro 45.000,00, derivante da Euro (70.000,00 - 25.000,00).<br />

Se nei 24 mesi <strong>la</strong> <strong>per</strong>sona del Quadro A ha intestato o donato più beni immobili, il <strong>di</strong>chiarante<br />

deve in<strong>di</strong>carli tutti.<br />

QUADRO E - SPESE SOSTENUTE DALLA PERSONA INDICATA NEL QUADRO<br />

A PER LA SUA ABITAZIONE<br />

Nel Quadro E il <strong>di</strong>chiarante deve in<strong>di</strong>care <strong>la</strong> situazione abitativa del<strong>la</strong> <strong>per</strong>sona del Quadro A e le<br />

spese che <strong>la</strong> <strong>per</strong>sona del Quadro A sostiene <strong>per</strong> l’abitazione.<br />

24

Nota 3: L’INDIVIDUAZIONE DEI PERIODI RELATIVI ALLE SPESE SOSTENUTE<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo delle spese sostenute <strong>di</strong>rettamente dal<strong>la</strong> <strong>per</strong>sona del Quadro<br />

A nel mese in cui presenta <strong>la</strong> <strong>di</strong>chiarazione. Se quando il <strong>di</strong>chiarante presenta <strong>la</strong> <strong>di</strong>chiarazione<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A <strong>per</strong> caso non ha ancora sostenuto nessuna delle spese <strong>di</strong> quelle in<strong>di</strong>cate<br />

nei Quadri E e F, ma le dovrà sostenere nel mese in corso, il <strong>di</strong>chiarante deve in<strong>di</strong>care<br />

le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha effettuato il mese precedente <strong>la</strong> <strong>di</strong>chiarazione.<br />

ESEMPIO 1: il <strong>di</strong>chiarante compi<strong>la</strong> <strong>la</strong> <strong>di</strong>chiarazione il giorno 1° luglio 2006. In tale data <strong>la</strong><br />

<strong>per</strong>sona del Quadro A non ha ancora sostenuto <strong>la</strong> spesa <strong>per</strong> i buoni pasto re<strong>la</strong>tiva al mese<br />

<strong>di</strong> luglio, ma <strong>la</strong> sosterrà. Il <strong>di</strong>chiarante scrive al Rigo F1 del Quadro F l’importo pagato dal<strong>la</strong><br />

<strong>per</strong>sona del Quadro A <strong>per</strong> i buoni pasto re<strong>la</strong>tivo al mese <strong>di</strong> giugno 2006.<br />

ESEMPIO 2: il <strong>di</strong>chiarante compi<strong>la</strong> <strong>la</strong> <strong>di</strong>chiarazione il giorno 14 giugno 2006. In tale data <strong>la</strong><br />

<strong>per</strong>sona del Quadro A non ha ancora sostenuto <strong>la</strong> spesa <strong>per</strong> l’affitto re<strong>la</strong>tiva al mese <strong>di</strong><br />

giugno, ma <strong>la</strong> dovrà sostenere. Il <strong>di</strong>chiarante scrive al Rigo F1 del Quadro F l’importo<br />

pagato dal<strong>la</strong> <strong>per</strong>sona del Quadro A <strong>per</strong> l’affitto re<strong>la</strong>tivo al mese <strong>di</strong> maggio 2006.<br />

Nota 4: LA DICHIARAZIONE DELLE SPESE PER L’ABITAZIONE<br />

Il <strong>di</strong>chiarante deve scrivere le spese <strong>per</strong> l’abitazione solo se queste spese le ha pagate <strong>la</strong><br />

<strong>per</strong>sona del Quadro A con denaro proprio. Quin<strong>di</strong> il <strong>di</strong>chiarante non deve scrivere le spese <strong>per</strong><br />

l’abitazione del<strong>la</strong> <strong>per</strong>sona del Quadro A che sono pagate con denaro <strong>di</strong> altre <strong>per</strong>sone.<br />

ESEMPIO: l’importo totale dell’affitto è <strong>di</strong> Euro 300,00. La <strong>per</strong>sona del Quadro A spende<br />

del proprio denaro solo Euro 100,00 <strong>per</strong> pagare l’affitto <strong>per</strong>ché Euro 200,00 sono pagate<br />

da suo figlio non convivente. Quin<strong>di</strong> come importo dell’affitto mensile il <strong>di</strong>chiarante deve<br />

scrivere solo Euro 100,00 e non Euro 300,00.<br />

Se <strong>la</strong> <strong>per</strong>sona del Quadro A vive con altre <strong>per</strong>sone che contribuiscono al pagamento dell’affitto,<br />

ma non è in grado <strong>di</strong> stabilire l’importo dell’affitto mensile che paga lei <strong>per</strong>sonalmente con danaro<br />

proprio, allora il <strong>di</strong>chiarante deve <strong>di</strong>videre l’importo totale dell’affitto mensile <strong>per</strong> il numero delle<br />

<strong>per</strong>sone che vivono con <strong>la</strong> <strong>per</strong>sona del Quadro A.<br />

ESEMPIO: L’importo totale dell’affitto ammonta a Euro 400,00 mensili; <strong>la</strong> <strong>per</strong>sona del Quadro A<br />

ha scritto al Rigo C1 <strong>di</strong> ricevere una pensione <strong>di</strong> Euro 500,00. Vive con <strong>la</strong> moglie. Non è in grado<br />

<strong>di</strong> stabilire quanto del<strong>la</strong> sua pensione copre il costo dell’affitto. Il <strong>di</strong>chiarante quin<strong>di</strong> deve <strong>di</strong>videre<br />

l’importo mensile dell’affitto <strong>per</strong> il numero delle <strong>per</strong>sone, ossia: Euro 400 / 2 = Euro 200,00.<br />

Il <strong>di</strong>chiarante scrive Euro 200,00 come importo dell’affitto mensile che paga <strong>la</strong> <strong>per</strong>sona del Quadro A.<br />

Inoltre, il <strong>di</strong>chiarante deve scrivere solo le spese re<strong>la</strong>tive ad un’abitazione il cui CONTRATTO <strong>di</strong><br />

affitto è stato REGISTRATO presso l’Agenzia delle Entrate.<br />

Nel<strong>la</strong> prima parte <strong>di</strong> questo Quadro E il Dichiarante deve mettere una croce su SI o NO a seconda<br />

se <strong>la</strong> <strong>per</strong>sona del Quadro A vive in una casa popo<strong>la</strong>re oppure in un altro tipo <strong>di</strong> casa. Inoltre, il<br />

<strong>di</strong>chiarante deve in<strong>di</strong>care <strong>la</strong> data e il numero <strong>di</strong> registrazione del contratto <strong>di</strong> affitto. Il <strong>di</strong>chiarante<br />

deve scrivere il costo TOTALE mensile dell’affitto, comprese le spese condominiali or<strong>di</strong>narie, come<br />

risulta dal contratto <strong>di</strong> affitto che è aggiornato ogni anno.<br />

Rigo E1<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se nel mese in cui il <strong>di</strong>chiarante<br />

presenta <strong>la</strong> <strong>di</strong>chiarazione (ve<strong>di</strong> sopra <strong>la</strong> Nota 3), <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato con il suo<br />

denaro l’affitto o parte <strong>di</strong> esso, senza considerare le spese <strong>di</strong> riscaldamento. Se mette una croce<br />

sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care tale importo (ve<strong>di</strong> sopra <strong>la</strong> Nota 4).<br />

Rigo E1.1<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se, al<strong>la</strong> data in cui presenta <strong>la</strong><br />

<strong>di</strong>chiarazione che sta compi<strong>la</strong>ndo, <strong>la</strong> <strong>per</strong>sona del Quadro A deve ancora pagare mesi <strong>di</strong> affitto<br />

passati, ossia è in ritardo con il pagamento dell’affitto. Se mette una croce sul SI, il <strong>di</strong>chiarante<br />

deve scrivere <strong>la</strong> somma <strong>di</strong> tutti gli affitti non pagati e, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha ricevuto<br />

25

un’ingiunzione <strong>di</strong> pagamento da parte del proprietario, o un’intimazione <strong>di</strong> sfratto, il<br />

<strong>di</strong>chiarante deve scrivere <strong>la</strong> cifra da pagare riportata nell’ingiunzione o nell’intimazione.<br />

ESEMPIO: Il <strong>di</strong>chiarante compi<strong>la</strong> <strong>la</strong> <strong>di</strong>chiarazione in data 25/06/2006. La <strong>per</strong>sona del Quadro A<br />

non paga l’affitto da marzo 2006. L’importo dell’affitto mensile è <strong>di</strong> Euro 300,00 e quin<strong>di</strong> <strong>la</strong><br />

<strong>per</strong>sona del Quadro A ha una morosità <strong>di</strong> Euro 1.200,00, ossia Euro 300,00 <strong>per</strong> 4 mesi<br />

<strong>di</strong> affitto. Il <strong>di</strong>chiarante deve scrivere al Rigo E1.1 come importo morosità Euro 1.200,00.<br />

Rigo E 1.2<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se, al<strong>la</strong> data in cui presenta <strong>la</strong><br />

<strong>di</strong>chiarazione che sta compi<strong>la</strong>ndo, <strong>la</strong> <strong>per</strong>sona del Quadro A deve ancora pagare bollette già<br />

scadute <strong>di</strong> luce, gas. Se mette una croce sul SI, il <strong>di</strong>chiarante deve scrivere <strong>la</strong> somma <strong>di</strong> tutte le<br />

bollette non pagate e se <strong>la</strong> <strong>per</strong>sona del Quadro A ha ricevuto un’ingiunzione <strong>di</strong> pagamento, il<br />

<strong>di</strong>chiarante deve scrivere <strong>la</strong> cifra da pagare riportata nell’ingiunzione.<br />

Rigo E2<br />

Il <strong>di</strong>chiarante deve compi<strong>la</strong>re questo Rigo E2 solo se <strong>la</strong> <strong>per</strong>sona del Quadro A non vive in affitto.<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A, nel mese<br />

in cui il <strong>di</strong>chiarante presenta <strong>la</strong> <strong>di</strong>chiarazione, ha pagato con il suo denaro (ve<strong>di</strong> <strong>la</strong> Nota 4, pag. 25)<br />

spese condominiali or<strong>di</strong>narie dell’abitazione in cui vive, senza considerare le spese <strong>di</strong> riscaldamento.<br />

Se <strong>la</strong> <strong>per</strong>sona del Quadro A non paga le spese condominiali or<strong>di</strong>narie una volta al mese, ma in<br />

rate <strong>per</strong>io<strong>di</strong>che (ad esempio ogni 3 mesi, ogni 6 mesi oppure una volta all’anno), il <strong>di</strong>chiarante<br />

deve considerare le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato nell’anno so<strong>la</strong>re precedente<br />

e <strong>di</strong>viderle <strong>per</strong> 12.<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è 28/11/2006; ogni anno <strong>la</strong> <strong>per</strong>sona del Quadro A<br />

riceve n. 4 rate <strong>di</strong> spese condominiali da pagare. Al<strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione <strong>la</strong> <strong>per</strong>sona<br />

del Quadro A ha pagato 3 rate; non ha ancora ricevuto <strong>la</strong> quarta. Poiché <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A non sa quanto pagherà <strong>di</strong> spese condominiali <strong>per</strong> tutto l’anno 2006, il <strong>di</strong>chiarante<br />

deve scrivere al Rigo E2 l’importo mensile delle spese condominiali pagato dal<strong>la</strong> <strong>per</strong>sona<br />

del Quadro A nell’anno 2005, <strong>di</strong>videndo tale importo totale <strong>per</strong> 12 mesi. Nell’anno 2005 le<br />

quattro rate delle spese condominiali ammontavano a Euro 1.200,00 (ciascuna rata era <strong>di</strong><br />

Euro 300,00). Al Rigo E2 il <strong>di</strong>chiarante scrive Euro 100,00, ossia Euro 1.200,00 <strong>di</strong>viso 12 mesi.<br />

Se nei 6 mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione, <strong>la</strong> <strong>per</strong>sona del Quadro A ha sostenuto spese<br />

condominiali straor<strong>di</strong>narie (ad esempio <strong>per</strong> <strong>la</strong>vori nelle parti comuni dello stabile in cui vive, <strong>per</strong><br />

il rifacimento del<strong>la</strong> facciata del pa<strong>la</strong>zzo, ecc.), il <strong>di</strong>chiarante deve scrivere l’importo totale <strong>di</strong> queste<br />

spese <strong>di</strong>viso <strong>per</strong> 6 mesi. Successivamente, il <strong>di</strong>chiarante deve sommare il risultato al totale delle<br />

spese sostenute dal<strong>la</strong> <strong>per</strong>sona del Quadro A <strong>per</strong> le spese or<strong>di</strong>narie.<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è 10/08/2006; in data 30/04/2006 <strong>la</strong> <strong>per</strong>sona del Quadro A<br />

ha pagato, come spese condominiali straor<strong>di</strong>narie, Euro 1.500,00 <strong>per</strong> il rifacimento del<strong>la</strong> facciata<br />

del pa<strong>la</strong>zzo in cui vive. Si <strong>di</strong>vide 1.500,00 Euro <strong>per</strong> 6 mesi: Euro 1.500 / 6 = Euro 250,00.<br />

Nel mese <strong>di</strong> agosto 2006, <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato 60,00 Euro <strong>per</strong> le spese<br />

condominiali or<strong>di</strong>narie. Al Rigo E2, il <strong>di</strong>chiarante deve scrivere l’importo <strong>di</strong> Euro 250 + 60 = 310,00.<br />

Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care quin<strong>di</strong> 310,00 Euro (ve<strong>di</strong> <strong>la</strong> Nota 4, pag. 25).<br />

Rigo E3<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se, nel mese in cui presenta <strong>la</strong><br />

<strong>di</strong>chiarazione, <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato con il suo denaro <strong>la</strong> rata <strong>di</strong> un mutuo che ha<br />

stipu<strong>la</strong>to <strong>per</strong> pagare l’abitazione in cui vive. Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care<br />

tale importo (ve<strong>di</strong> <strong>la</strong> Nota 3 e 4, pag. 25).<br />

ESEMPIO: La <strong>per</strong>sona del Quadro A è proprietaria dell’abitazione in cui vive; il mutuo <strong>di</strong><br />

Euro 500,00 mensili viene pagato dal figlio. Il <strong>di</strong>chiarante NON deve scrivere l’importo del<br />

mutuo poiché è pagato dal figlio e non dal<strong>la</strong> <strong>per</strong>sona del Quadro A.<br />

26

QUADRO F - SPESE SOSTENUTE DALLA PERSONA INDICATA NEL QUADRO<br />

A O DA ALTRE PERSONE PER INTERVENTI ASSISTENZIALI<br />

Rigo F1<br />

a) Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se nel mese in cui il <strong>di</strong>chiarante<br />

presenta <strong>la</strong> <strong>di</strong>chiarazione che sta compi<strong>la</strong>ndo, <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato con denaro<br />

proprio (ve<strong>di</strong> <strong>la</strong> Nota 3, pag. 25) le seguenti spese a favore <strong>di</strong> qualsiasi <strong>per</strong>sona <strong>di</strong>versa da<br />

se stessa:<br />

• spese sostenute <strong>per</strong> contribuire al costo <strong>di</strong> servizi assistenziali (ad esempio, il pagamento<br />

delle tariffe <strong>per</strong> l’assistenza domiciliare, il telesoccorso, i pasti a domicilio, i buoni taxi)<br />

• spese sostenute <strong>per</strong> il pagamento delle rette dei ricoveri in residenze sociosanitarie o<br />

socioassistenziali (cioè NON in ospedale)<br />

• spese sostenute <strong>per</strong> il pagamento <strong>di</strong> <strong>la</strong>voratori domestici che hanno prestato assistenza a<br />

domicilio. Il <strong>di</strong>chiarante deve scrivere le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha sostenuto <strong>per</strong><br />

pagare questi <strong>la</strong>voratori a domicilio solo se esiste un rego<strong>la</strong>re contratto <strong>di</strong> <strong>la</strong>voro subor<strong>di</strong>nato, in<br />

base alle leggi che rego<strong>la</strong>no <strong>la</strong> materia.<br />

Se mette una croce sul SI del Rigo F1, il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo che <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A ha pagato.<br />

ESEMPIO 1: La <strong>di</strong>chiarazione è datata 18/06/2006. La <strong>per</strong>sona del Quadro A ha pagato il<br />

15/04/2006 Euro 1.000,00 ad un <strong>la</strong>voratore domiciliare che ha assistito suo marito convivente.<br />

Il <strong>la</strong>voratore non aveva contratto <strong>di</strong> <strong>la</strong>voro, quin<strong>di</strong> il <strong>di</strong>chiarante deve mettere NO al Rigo F1<br />

e NON deve in<strong>di</strong>care Euro 1.000,00 al Rigo F1.<br />

ESEMPIO 2: La <strong>di</strong>chiarazione è datata 20/07/2006. La <strong>per</strong>sona del Quadro A ha pagato il<br />

15/07/2006 (o pagherà comunque nel mese <strong>di</strong> luglio) Euro 2.000,00 ad un <strong>la</strong>voratore<br />

domiciliare <strong>per</strong> l’assistenza a suo figlio, <strong>la</strong>voratore con il quale è stato stipu<strong>la</strong>to contratto <strong>di</strong> <strong>la</strong>voro;<br />

quin<strong>di</strong> il <strong>di</strong>chiarante deve mettere SI al Rigo F1 e deve in<strong>di</strong>care Euro 2.000,00 al Rigo F1.<br />

Il <strong>di</strong>chiarante NON deve invece in<strong>di</strong>care al Rigo F1 le spese sanitarie pagate. Ad esempio,<br />

non si devono in<strong>di</strong>care le spese sostenute <strong>per</strong>: le prestazioni chirurgiche; le analisi, le<br />

prestazioni specialistiche; l’acquisto o affitto <strong>di</strong> protesi sanitarie; le prestazioni rese da un<br />

me<strong>di</strong>co (comprese le prestazioni rese <strong>per</strong> visite e cure <strong>di</strong> me<strong>di</strong>cina omeopatica); i ricoveri<br />

collegati ad una o<strong>per</strong>azione chirurgica o le degenze; l’acquisto <strong>di</strong> me<strong>di</strong>cinali; le spese re<strong>la</strong>tive<br />

all’acquisto o all’affitto <strong>di</strong> attrezzature sanitarie; gli importi pagati <strong>per</strong> i ticket; l’assistenza<br />

infermieristica e riabilitativa (ad esempio, fisioterapia, <strong>la</strong>serterapia, ecc...).<br />

b) Sempre nel Rigo F1, il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se nel<br />

mese in cui il <strong>di</strong>chiarante presenta <strong>la</strong> <strong>di</strong>chiarazione (ve<strong>di</strong> <strong>la</strong> Nota 3, pag. 25), <strong>la</strong> <strong>per</strong>sona del<br />

Quadro A ha pagato con denaro proprio le spese sostenute solo a favore <strong>di</strong> se stessa <strong>per</strong><br />

contribuire al costo <strong>di</strong> servizi assistenziali (ad esempio, <strong>per</strong> il pagamento delle tariffe <strong>per</strong> i suoi<br />

buoni taxi). Se mette una croce sul SI del Rigo F1 il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo totale che<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

ESEMPIO: La <strong>di</strong>chiarazione è datata 18/06/2006. La <strong>per</strong>sona del Quadro A ha pagato il<br />

15/04/2006 Euro 200,00 quale tariffa <strong>per</strong> i buoni taxi del mese <strong>di</strong> giugno 2006. Il <strong>di</strong>chiarante<br />

deve in<strong>di</strong>care SI al Rigo F1 e deve in<strong>di</strong>care Euro 200,00 al Rigo F1.<br />

Il <strong>di</strong>chiarante NON deve in<strong>di</strong>care né le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha sostenuto <strong>per</strong> il<br />

pagamento <strong>di</strong> rette <strong>per</strong> il suo ricovero in residenze sociosanitarie o socioassistenziali, né le spese<br />

<strong>per</strong> il pagamento del suo telesoccorso, né dei suoi pasti a domicilio, né dei suoi ricoveri <strong>di</strong> sollievo,<br />

né <strong>per</strong> i <strong>la</strong>voratori domestici che le hanno prestato assistenza.<br />

Anche in questo caso il <strong>di</strong>chiarante NON deve in<strong>di</strong>care le spese sanitarie che ha pagato con<br />

denaro proprio a favore <strong>di</strong> se stessa, come prima specificate.<br />

ATTENZIONE: nel Rigo F1 si devono <strong>di</strong>chiarare le spese sostenute nel mese in cui si<br />

presenta <strong>la</strong> <strong>di</strong>chiarazione (ve<strong>di</strong> <strong>la</strong> Nota 3, pag. 25); se tali spese nei mesi dopo <strong>la</strong> <strong>di</strong>chiarazione<br />

cambiano <strong>di</strong> più del 20% dell’importo iniziale, il <strong>di</strong>chiarante deve <strong>di</strong>chiarare al Servizio<br />

Sociale questa variazione (ve<strong>di</strong> in fondo le istruzioni del Quadro J).<br />

27

Rigo F2<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A oppure<br />

altre <strong>per</strong>sone hanno pagato <strong>per</strong> <strong>la</strong> <strong>per</strong>sona del Quadro A spese <strong>per</strong> <strong>la</strong> retta <strong>di</strong> ricovero in strutture<br />

residenziali sociosanitarie <strong>di</strong>verse da ricoveri in ospedali nei 24 mesi precedenti il mese in cui il<br />

<strong>di</strong>chiarante presenta <strong>la</strong> <strong>di</strong>chiarazione che sta compi<strong>la</strong>ndo. Se mette una croce sul SI, il <strong>di</strong>chiarante<br />

deve in<strong>di</strong>care l’importo TOTALE pagato nel <strong>per</strong>iodo, ossia sommare tutti gli importi pagati da<br />

chiunque durante i 24 mesi precedenti <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

ESEMPIO: La data del<strong>la</strong> <strong>di</strong>chiarazione è il 30/08/2006; <strong>la</strong> <strong>per</strong>sona del Quadro A, il 16/01/2006<br />

ha pagato Euro 1.500,00 <strong>per</strong> il suo ricovero in Residenza Sanitaria Assistenziale; il 15/05/2005<br />

il figlio del<strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato Euro 3.000,00 <strong>per</strong> il ricovero in Residenza<br />

Sanitaria Assistenziale del<strong>la</strong> <strong>per</strong>sona del Quadro A; il 15/07/2004 <strong>la</strong> <strong>per</strong>sona del Quadro A<br />

ha pagato Euro 2.000,00 <strong>per</strong> il suo ricovero in Residenza Sanitaria Assistenziale. Il <strong>di</strong>chiarante<br />

deve scrivere al Rigo F2 le spese <strong>di</strong> Euro 1.500,00 e <strong>di</strong> Euro 3.000,00, poiché sostenute<br />

nei 24 mesi che precedono <strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione, ma NON deve scrivere <strong>la</strong> spesa <strong>di</strong><br />

Euro 2.000,00 <strong>per</strong>ché sostenuta oltre 24 mesi prima del<strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

Rigo F3<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A oppure<br />

altre <strong>per</strong>sone hanno pagato, nei 24 mesi precedenti a quello in cui presenta <strong>la</strong> <strong>di</strong>chiarazione che<br />

sta compi<strong>la</strong>ndo, spese <strong>per</strong> l’assistenza domiciliare <strong>per</strong>sonale del<strong>la</strong> <strong>per</strong>sona del Quadro A. Il<br />

<strong>di</strong>chiarante deve scrivere le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha sostenuto <strong>per</strong> pagare questi<br />

<strong>la</strong>voratori solo se esiste un rego<strong>la</strong>re contratto <strong>di</strong> <strong>la</strong>voro subor<strong>di</strong>nato, in base alle leggi che rego<strong>la</strong>no<br />

<strong>la</strong> materia. Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo TOTALE pagato, ossia<br />

sommare tutti gli importi pagati da chiunque <strong>per</strong> tale prestazione nel corso dei 24 mesi precedenti<br />

<strong>la</strong> data del<strong>la</strong> <strong>di</strong>chiarazione.<br />

QUADRO G - ALTRE SPESE SOSTENUTE DALLA PERSONA INDICATA NEL<br />

QUADRO A SOLO DOPO AVER RICEVUTO ARRETRATI<br />

O EFFETTUATO DONAZIONI<br />

Questo Quadro G del<strong>la</strong> <strong>di</strong>chiarazione è strettamente legato al Quadro D, <strong>per</strong> il fatto che nel Quadro G<br />

il <strong>di</strong>chiarante deve ri<strong>la</strong>sciare le informazioni richieste:<br />

• soltanto se ha già ri<strong>la</strong>sciato delle informazioni al Quadro D<br />

• soltanto le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato dopo che ha ricevuto degli<br />

arretrati <strong>di</strong>chiarati al Quadro D, oppure dopo le intestazioni o donazioni fatte e <strong>di</strong>chiarate<br />

al Quadro D.<br />

Nel Quadro G il <strong>di</strong>chiarante deve scrivere SOLO le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha sostenuto<br />

con denaro proprio e che ha speso <strong>per</strong>:<br />

• se stessa<br />

• oppure che ha sostenuto a favore <strong>di</strong> <strong>per</strong>sone che vivevano con lei al<strong>la</strong> data in cui ha sostenuto<br />

le spese.<br />

Nota 5: COME CONSIDERARE LE SPESE SOSTENUTE DOPO AVERE RICEVUTO ARRETRATI<br />

O FATTO DONAZIONI<br />

• Se il <strong>di</strong>chiarante non ha messo neanche una crocetta sui SI nel Quadro D, e non ha scritto<br />

nessun importo o valore nel Quadro D, allora non deve compi<strong>la</strong>re questo Quadro G.<br />

• Se il <strong>di</strong>chiarante ha <strong>di</strong>chiarato un importo o un valore ad una domanda del Quadro D, allora<br />

deve scrivere in questo Quadro G le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato dopo <strong>la</strong> data<br />

che ha in<strong>di</strong>cato al Rigo del Quadro D.<br />

• Se il <strong>di</strong>chiarante ha <strong>di</strong>chiarato importi/valori su più domande del Quadro D allora deve scrivere<br />

in questo Quadro G le spese che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato dopo <strong>la</strong> data più lontana<br />

nel tempo tra quelle che ha in<strong>di</strong>cato nelle righe del Quadro D.<br />

28

ESEMPIO: La <strong>per</strong>sona del Quadro A era un impren<strong>di</strong>tore ed è fallito; ha pagato debiti da<br />

fallimento <strong>per</strong> Euro 2.000,00 a Febbraio 2004. La <strong>per</strong>sona del Quadro A ha inoltre maturato<br />

delle morosità <strong>di</strong> affitto <strong>per</strong> Euro 1.000,00 a febbraio 2005. Il <strong>di</strong>chiarante al Rigo D1 ha<br />

scritto Data <strong>di</strong> riscossione 15/01/2006; al Rigo D2 ha scritto Data <strong>di</strong> riscossione 18/01/2005;<br />

al Rigo D3 ha scritto Data <strong>di</strong> riscossione 23/06/2005: <strong>la</strong> data più lontana nel tempo è<br />

18/01/2005, quin<strong>di</strong> nel Quadro G il <strong>di</strong>chiarante deve scrivere SOLO le spese sostenute dal<strong>la</strong><br />

<strong>per</strong>sona del Quadro A dopo il 18/01/2005, ossia al Rigo G1 non scrive alcun importo poiché<br />

i debiti <strong>per</strong> fallimento sono stati pagati prima del 18/01/2005, mentre al Rigo G3 scrive Euro 1.000,00<br />

poiché <strong>la</strong> morosità è stata pagata dopo il 18/01/2005.<br />

Rigo G1<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio debiti riguardanti fallimenti o altre procedure simili, che, secondo le<br />

norme in vigore, hanno riguardato <strong>la</strong> <strong>per</strong>sona del Quadro A oppure le <strong>per</strong>sone che vivevano con<br />

lei al<strong>la</strong> data in cui ha sostenuto le spese. Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care<br />

l’importo che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

Rigo G2<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio debiti re<strong>la</strong>tivi ad usura, ossia in seguito ad estorsione <strong>di</strong> denaro subite<br />

durante lo svolgimento <strong>di</strong> attività <strong>di</strong> <strong>la</strong>voro autonomo o d’impresa. Questi debiti devono essere<br />

stati pagati dal<strong>la</strong> <strong>per</strong>sona del Quadro A a favore <strong>di</strong> se stessa oppure a favore <strong>di</strong> <strong>per</strong>sone che<br />

vivevano con lei al<strong>la</strong> data in cui ha sostenuto le spese. Il <strong>di</strong>chiarante deve scrivere queste spese,<br />

a con<strong>di</strong>zione che sia stata presentata rego<strong>la</strong>re quere<strong>la</strong> all’Autorità Giu<strong>di</strong>ziaria e non ha ricevuto<br />

il contributo dal Fondo Nazionale o Regionale <strong>per</strong> le vittime dell’usura.<br />

Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

Rigo G3<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio (ve<strong>di</strong> <strong>la</strong> Nota 4, pag. 25) debiti riguardanti affitti arretrati, ossia scaduti,<br />

a seguito dei quali è <strong>di</strong>ventato moroso nell’affitto. Questi debiti devono essere stati pagati dal<strong>la</strong><br />

<strong>per</strong>sona del Quadro A a favore <strong>di</strong> se stessa oppure a favore delle <strong>per</strong>sone che vivevano con lei<br />

al<strong>la</strong> data in cui ha sostenuto le spese. Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care<br />

l’importo che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

Rigo G4<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio (ve<strong>di</strong> <strong>la</strong> Nota 4, pag. 25) debiti riguardanti bollette scadute, ossia <strong>per</strong><br />

cui ha una morosità <strong>di</strong> luce e gas. Questi debiti devono essere stati pagati dal<strong>la</strong> <strong>per</strong>sona del<br />

Quadro A a favore <strong>di</strong> se stessa oppure a favore delle <strong>per</strong>sone che vivevano con lei al<strong>la</strong> data in<br />

cui ha sostenuto le spese. Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo che<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

Rigo G5<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio spese funerarie <strong>per</strong> il decesso del coniuge, <strong>di</strong> parenti entro il quarto<br />

grado (anche non conviventi con <strong>la</strong> <strong>per</strong>sona del Quadro A), <strong>di</strong> parenti entro il quarto grado <strong>di</strong><br />

<strong>per</strong>sone che vivono con <strong>la</strong> <strong>per</strong>sona del Quadro A. Queste spese devono essere state pagate dal<strong>la</strong><br />

<strong>per</strong>sona del Quadro A a favore delle <strong>per</strong>sone che vivevano con lei al<strong>la</strong> data in cui ha sostenuto<br />

le spese.<br />

I parenti entro il quarto grado sono: i figli legittimi o legittimati o adottivi e, in loro mancanza,<br />

i <strong>di</strong>scendenti prossimi, anche naturali; i genitori e in loro mancanza, gli ascendenti prossimi,<br />

gli adottanti; i generi e le nuore; il suocero e <strong>la</strong> suocera; i fratelli e le sorelle. Se mette una croce<br />

sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo che <strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

Rigo G6<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio spese <strong>per</strong> rendere agibile l’abitazione in cui vive. Queste spese devono<br />

29

essere state pagate dal<strong>la</strong> <strong>per</strong>sona del Quadro A a favore <strong>di</strong> se stessa oppure a favore delle <strong>per</strong>sone<br />

che vivevano con lei al<strong>la</strong> data in cui ha sostenuto le spese. Il <strong>di</strong>chiarante deve scrivere queste<br />

spese soltanto se l’Autorità competente ha emanato una <strong>di</strong>chiarazione <strong>di</strong> inagibilità <strong>di</strong> tale abitazione.<br />

Il <strong>di</strong>chiarante non deve quin<strong>di</strong> scrivere le spese fatte <strong>per</strong> ristrutturazioni dell’abitazione in assenza<br />

<strong>di</strong> <strong>di</strong>chiarazione <strong>di</strong> inagibilità. Se mette una croce sul SI, il <strong>di</strong>chiarante deve in<strong>di</strong>care l’importo che<br />

<strong>la</strong> <strong>per</strong>sona del Quadro A ha pagato.<br />

Rigo G7<br />

Il <strong>di</strong>chiarante deve in<strong>di</strong>care, con una croce su SI oppure su NO, se <strong>la</strong> <strong>per</strong>sona del Quadro A ha<br />

pagato con denaro proprio spese <strong>per</strong> togliere barriere architettoniche che esistevano nell’abitazione<br />

in cui vive. Queste spese devono essere state pagate dal<strong>la</strong> <strong>per</strong>sona del Quadro A a favore <strong>di</strong> se<br />