Management of the Holyrood building project (PDF ... - Audit Scotland

Management of the Holyrood building project (PDF ... - Audit Scotland

Management of the Holyrood building project (PDF ... - Audit Scotland

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

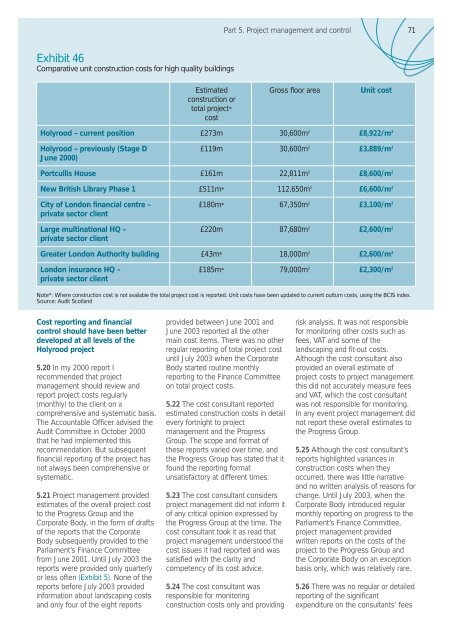

Exhibit 46<br />

Comparative unit construction costs for high quality <strong>building</strong>s<br />

Cost reporting and financial<br />

control should have been better<br />

developed at all levels <strong>of</strong> <strong>the</strong><br />

<strong>Holyrood</strong> <strong>project</strong><br />

5.20 In my 2000 report I<br />

recommended that <strong>project</strong><br />

management should review and<br />

report <strong>project</strong> costs regularly<br />

(monthly) to <strong>the</strong> client on a<br />

comprehensive and systematic basis.<br />

The Accountable Officer advised <strong>the</strong><br />

<strong>Audit</strong> Committee in October 2000<br />

that he had implemented this<br />

recommendation. But subsequent<br />

financial reporting <strong>of</strong> <strong>the</strong> <strong>project</strong> has<br />

not always been comprehensive or<br />

systematic.<br />

5.21 Project management provided<br />

estimates <strong>of</strong> <strong>the</strong> overall <strong>project</strong> cost<br />

to <strong>the</strong> Progress Group and <strong>the</strong><br />

Corporate Body, in <strong>the</strong> form <strong>of</strong> drafts<br />

<strong>of</strong> <strong>the</strong> reports that <strong>the</strong> Corporate<br />

Body subsequently provided to <strong>the</strong><br />

Parliament’s Finance Committee<br />

from June 2001. Until July 2003 <strong>the</strong><br />

reports were provided only quarterly<br />

or less <strong>of</strong>ten (Exhibit 5). None <strong>of</strong> <strong>the</strong><br />

reports before July 2003 provided<br />

information about landscaping costs<br />

and only four <strong>of</strong> <strong>the</strong> eight reports<br />

Part 5. Project management and control<br />

Estimated Gross floor area Unit cost<br />

construction or<br />

total <strong>project</strong>*<br />

cost<br />

<strong>Holyrood</strong> – current position £273m 30,600m 2 £8,922/m 2<br />

<strong>Holyrood</strong> – previously (Stage D £119m 30,600m 2 £3,889/m 2<br />

June 2000)<br />

Portcullis House £161m 22,811m 2 £8,600/m 2<br />

New British Library Phase 1 £511m* 112,650m 2 £6,600/m 2<br />

City <strong>of</strong> London financial centre – £180m* 67,350m 2 £3,100/m 2<br />

private sector client<br />

Large multinational HQ – £220m 87,680m 2 £2,600/m 2<br />

private sector client<br />

Greater London Authority <strong>building</strong> £43m* 18,000m 2 £2,600/m 2<br />

London insurance HQ – £185m* 79,000m 2 £2,300/m 2<br />

private sector client<br />

Note*: Where construction cost is not available <strong>the</strong> total <strong>project</strong> cost is reported. Unit costs have been updated to current outturn costs, using <strong>the</strong> BCIS index.<br />

Source: <strong>Audit</strong> <strong>Scotland</strong><br />

provided between June 2001 and<br />

June 2003 reported all <strong>the</strong> o<strong>the</strong>r<br />

main cost items. There was no o<strong>the</strong>r<br />

regular reporting <strong>of</strong> total <strong>project</strong> cost<br />

until July 2003 when <strong>the</strong> Corporate<br />

Body started routine monthly<br />

reporting to <strong>the</strong> Finance Committee<br />

on total <strong>project</strong> costs.<br />

5.22 The cost consultant reported<br />

estimated construction costs in detail<br />

every fortnight to <strong>project</strong><br />

management and <strong>the</strong> Progress<br />

Group. The scope and format <strong>of</strong><br />

<strong>the</strong>se reports varied over time, and<br />

<strong>the</strong> Progress Group has stated that it<br />

found <strong>the</strong> reporting format<br />

unsatisfactory at different times.<br />

5.23 The cost consultant considers<br />

<strong>project</strong> management did not inform it<br />

<strong>of</strong> any critical opinion expressed by<br />

<strong>the</strong> Progress Group at <strong>the</strong> time. The<br />

cost consultant took it as read that<br />

<strong>project</strong> management understood <strong>the</strong><br />

cost issues it had reported and was<br />

satisfied with <strong>the</strong> clarity and<br />

competency <strong>of</strong> its cost advice.<br />

5.24 The cost consultant was<br />

responsible for monitoring<br />

construction costs only and providing<br />

71<br />

risk analysis. It was not responsible<br />

for monitoring o<strong>the</strong>r costs such as<br />

fees, VAT and some <strong>of</strong> <strong>the</strong><br />

landscaping and fit-out costs.<br />

Although <strong>the</strong> cost consultant also<br />

provided an overall estimate <strong>of</strong><br />

<strong>project</strong> costs to <strong>project</strong> management<br />

this did not accurately measure fees<br />

and VAT, which <strong>the</strong> cost consultant<br />

was not responsible for monitoring.<br />

In any event <strong>project</strong> management did<br />

not report <strong>the</strong>se overall estimates to<br />

<strong>the</strong> Progress Group.<br />

5.25 Although <strong>the</strong> cost consultant’s<br />

reports highlighted variances in<br />

construction costs when <strong>the</strong>y<br />

occurred, <strong>the</strong>re was little narrative<br />

and no written analysis <strong>of</strong> reasons for<br />

change. Until July 2003, when <strong>the</strong><br />

Corporate Body introduced regular<br />

monthly reporting on progress to <strong>the</strong><br />

Parliament’s Finance Committee,<br />

<strong>project</strong> management provided<br />

written reports on <strong>the</strong> costs <strong>of</strong> <strong>the</strong><br />

<strong>project</strong> to <strong>the</strong> Progress Group and<br />

<strong>the</strong> Corporate Body on an exception<br />

basis only, which was relatively rare.<br />

5.26 There was no regular or detailed<br />

reporting <strong>of</strong> <strong>the</strong> significant<br />

expenditure on <strong>the</strong> consultants’ fees