BEREC REPORT ON IMPACT OF FIXED-MOBILE ... - berec - Europa

BEREC REPORT ON IMPACT OF FIXED-MOBILE ... - berec - Europa

BEREC REPORT ON IMPACT OF FIXED-MOBILE ... - berec - Europa

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

BoR (11) 54<br />

Based on these general figures, one may conclude that fixed and mobile access are<br />

generally regarded as complementary (and not as substitutes). Once again, other<br />

factors nonetheless need to be considered and an analysis based on detailed national<br />

data would generally be necessary to reach a conclusion.<br />

4.1.2. A highly heterogeneous picture<br />

Looking at each country separately, the general picture is highly heterogeneous.<br />

Calls<br />

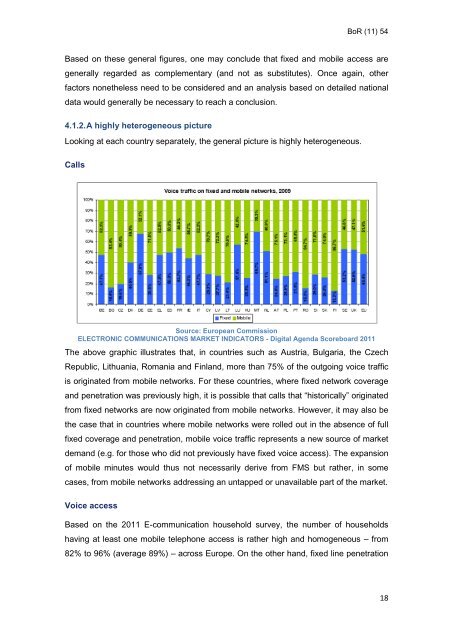

Source: European Commission<br />

ELECTR<strong>ON</strong>IC COMMUNICATI<strong>ON</strong>S MARKET INDICATORS - Digital Agenda Scoreboard 2011<br />

The above graphic illustrates that, in countries such as Austria, Bulgaria, the Czech<br />

Republic, Lithuania, Romania and Finland, more than 75% of the outgoing voice traffic<br />

is originated from mobile networks. For these countries, where fixed network coverage<br />

and penetration was previously high, it is possible that calls that “historically” originated<br />

from fixed networks are now originated from mobile networks. However, it may also be<br />

the case that in countries where mobile networks were rolled out in the absence of full<br />

fixed coverage and penetration, mobile voice traffic represents a new source of market<br />

demand (e.g. for those who did not previously have fixed voice access). The expansion<br />

of mobile minutes would thus not necessarily derive from FMS but rather, in some<br />

cases, from mobile networks addressing an untapped or unavailable part of the market.<br />

Voice access<br />

Based on the 2011 E-communication household survey, the number of households<br />

having at least one mobile telephone access is rather high and homogeneous – from<br />

82% to 96% (average 89%) – across Europe. On the other hand, fixed line penetration<br />

18