SYDNEY PORTS CORPORATION ANNUAL REPORT 12

SYDNEY PORTS CORPORATION ANNUAL REPORT 12

SYDNEY PORTS CORPORATION ANNUAL REPORT 12

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

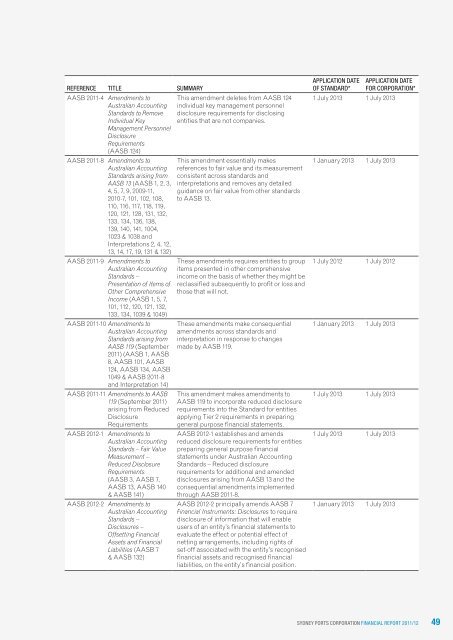

eferenCe title SUmmary<br />

AASB 2011-4 Amendments to<br />

Australian Accounting<br />

Standards to Remove<br />

Individual Key<br />

Management Personnel<br />

Disclosure<br />

Requirements<br />

(AASB <strong>12</strong>4)<br />

AASB 2011-8 Amendments to<br />

Australian Accounting<br />

Standards arising from<br />

AASB 13 (AASB 1, 2, 3,<br />

4, 5, 7, 9, 2009-11,<br />

2010-7, 101, 102, 108,<br />

110, 116, 117, 118, 119,<br />

<strong>12</strong>0, <strong>12</strong>1, <strong>12</strong>8, 131, 132,<br />

133, 134, 136, 138,<br />

139, 140, 141, 1004,<br />

1023 & 1038 and<br />

Interpretations 2, 4, <strong>12</strong>,<br />

13, 14, 17, 19, 131 & 132)<br />

AASB 2011-9 Amendments to<br />

Australian Accounting<br />

Standards –<br />

Presentation of Items of<br />

Other Comprehensive<br />

Income (AASB 1, 5, 7,<br />

101, 1<strong>12</strong>, <strong>12</strong>0, <strong>12</strong>1, 132,<br />

133, 134, 1039 & 1049)<br />

AASB 2011-10 Amendments to<br />

Australian Accounting<br />

Standards arising from<br />

AASB 119 (September<br />

2011) (AASB 1, AASB<br />

8, AASB 101, AASB<br />

<strong>12</strong>4, AASB 134, AASB<br />

1049 & AASB 2011-8<br />

and Interpretation 14)<br />

AASB 2011-11 Amendments to AASB<br />

119 (September 2011)<br />

arising from Reduced<br />

Disclosure<br />

Requirements<br />

AASB 20<strong>12</strong>-1 Amendments to<br />

Australian Accounting<br />

Standards – Fair Value<br />

Measurement –<br />

Reduced Disclosure<br />

Requirements<br />

(AASB 3, AASB 7,<br />

AASB 13, AASB 140<br />

& AASB 141)<br />

AASB 20<strong>12</strong>-2 Amendments to<br />

Australian Accounting<br />

Standards –<br />

Disclosures –<br />

Offsetting Financial<br />

Assets and Financial<br />

Liabilities (AASB 7<br />

& AASB 132)<br />

This amendment deletes from AASB <strong>12</strong>4<br />

individual key management personnel<br />

disclosure requirements for disclosing<br />

entities that are not companies.<br />

This amendment essentially makes<br />

references to fair value and its measurement<br />

consistent across standards and<br />

interpretations and removes any detailed<br />

guidance on fair value from other standards<br />

to AASB 13.<br />

These amendments requires entities to group<br />

items presented in other comprehensive<br />

income on the basis of whether they might be<br />

reclassified subsequently to profit or loss and<br />

those that will not.<br />

These amendments make consequential<br />

amendments across standards and<br />

interpretation in response to changes<br />

made by AASB 119.<br />

This amendment makes amendments to<br />

AASB 119 to incorporate reduced disclosure<br />

requirements into the Standard for entities<br />

applying Tier 2 requirements in preparing<br />

general purpose financial statements.<br />

AASB 20<strong>12</strong>-1 establishes and amends<br />

reduced disclosure requirements for entities<br />

preparing general purpose financial<br />

statements under Australian Accounting<br />

Standards – Reduced disclosure<br />

requirements for additional and amended<br />

disclosures arising from AASB 13 and the<br />

consequential amendments implemented<br />

through AASB 2011-8.<br />

AASB 20<strong>12</strong>-2 principally amends AASB 7<br />

Financial Instruments: Disclosures to require<br />

disclosure of information that will enable<br />

users of an entity’s financial statements to<br />

evaluate the effect or potential effect of<br />

netting arrangements, including rights of<br />

set-off associated with the entity’s recognised<br />

financial assets and recognised financial<br />

liabilities, on the entity’s financial position.<br />

aPPliCation date<br />

of Standard*<br />

aPPliCation date<br />

for CorPoration*<br />

1 July 2013 1 July 2013<br />

1 January 2013 1 July 2013<br />

1 July 20<strong>12</strong> 1 July 20<strong>12</strong><br />

1 January 2013 1 July 2013<br />

1 July 2013 1 July 2013<br />

1 July 2013 1 July 2013<br />

1 January 2013 1 July 2013<br />

Sydney PortS CorPoration finanCial rePort 2011/<strong>12</strong> 49