http://legacy.library.ucsf.edu/tid/deg12a00/pdf

http://legacy.library.ucsf.edu/tid/deg12a00/pdf

http://legacy.library.ucsf.edu/tid/deg12a00/pdf

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

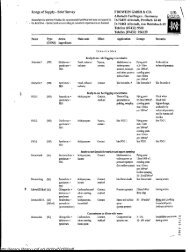

S Yeara 1972 1967<br />

Compounded Average<br />

Annual Growth<br />

Rate<br />

: Operatin g<br />

Revenues 52,131,224 $904,841 18 .746<br />

Pre-Tax<br />

Income 229,634 81,317 23 .19<br />

s<br />

6 Earning<br />

pershare<br />

Primary 4.67 1.9718 :9% .<br />

Fully<br />

Dt7uted 4.37 1 .94 17 .6 %<br />

10 Years 1972196<br />

2Compounded Average<br />

Annual Growt h<br />

Rate<br />

Operaling<br />

Revenues S2,131y24 $550,624 14 .5 %<br />

Pre-Tax<br />

Income 229,634 47,464 1115.<br />

Earnings<br />

per Share<br />

Primary 4.67 0.98 16 .9%<br />

Full y<br />

DilJtted 4.37 0.9816 :1°0<br />

15 Years<br />

Operating<br />

Revenues<br />

fre-Tax<br />

Income<br />

Earnings<br />

per 3hare<br />

Primary<br />

Fully<br />

Diluted<br />

1972 1957<br />

Compounded Average<br />

Annual Growth<br />

Rate<br />

$2,131,734 $439,920 : 11 .11.<br />

229,634 35,740 132 %<br />

4.67 0,76 12.996<br />

437, 0.76 12:4 %<br />

The year 1972 was one of significant<br />

achievement for Philip Morris<br />

Incorporated in terms of unit sales ,<br />

revenues, profits and continue d<br />

strengthening of its financial position .<br />

The above table highlights the recor d<br />

of our growth during the last 5-, 10- ,<br />

and 15-year periods . This<br />

performance establishes Phili p<br />

Morris as one of the leading growth<br />

companies in U.S. industry .<br />

The improving trend lnpre-tax profi t<br />

margin which commenced in 1965<br />

continued during 1972, as may be<br />

noted in Chart 1 . This improvement<br />

<strong>http</strong>://<strong>legacy</strong>.<strong>library</strong>.<strong>ucsf</strong>.<strong>edu</strong>/<strong>tid</strong>/<strong>deg12a00</strong>/<strong>pdf</strong><br />

was particularly gratifying in view<br />

of the increased cost of tobacco leaf .<br />

labor, and other raw materials, and<br />

the absence of any opportunity to<br />

increase prices due to government<br />

controls . This improvement was<br />

primarily the result of the significantly<br />

greater unit volume and a n<br />

effective cost control program<br />

throughout the company .<br />

Record levels of capital expenditures<br />

were recordedduring 1972 in<br />

the amount of S 120 million,<br />

However, our expanding funds from<br />

operations provided the majority-<br />

97 percentin 1972-of our capital<br />

expenditure requirements, as<br />

illustrated in Chart 2 and further<br />

amplified in the Financial Statements .<br />

We anticipate thatthis high leveliof,<br />

capital spending will continue for at<br />

least the next five years and that<br />

during that time these requirements<br />

will be exceeded by internally<br />

generated funds from operations.<br />

For the fifth consecutive year, the<br />

company increased the dividend on<br />

its common stock . As a result of the<br />

Phase Ii restrictions, this increase<br />

was limited to 4% for1972 : As<br />

illustrated in Chart3 ; our dividend<br />

payoutcontinues to be conservative<br />

and we believe represents sound<br />

financial policy in view of the high<br />

level of capital expenditures<br />

anticipated for the nextseveral years.<br />

This conservative dividendpoliey,<br />

plus conversion ofdebentures, has<br />

resulted in a rather rapid expansion<br />

of stockholders' equity (Chart 7)j<br />

Nonetheless, our pre-tax return on<br />

stockholders' equity continues to<br />

exceed'30%, which is well ahead of<br />

the return on equity of the 30 Dow<br />

Iones industrial companies (Chart 4)j<br />

The reeentaapid growth in our pe r<br />

share earnings extended into 1972.<br />

CharrS illustrates thisgtowth an d<br />

compares Philip Morris performance<br />

with that ofrthe 425 stocks used i n<br />

the Standard and Poor's industria l<br />

average .<br />

Our overall financial condition<br />

strengthened further in 1972 with a<br />

substantial increase in workin g<br />

capital as well as stockholders' equity<br />

(Chart7) . Long term debt increased<br />

from the prior year primarily as a<br />

result of converting $150 million of<br />

our short'term borrowingS to long<br />

term, However, the ratio of long term<br />

debt to equity (Chart 6) has been<br />

r<strong>edu</strong>ced from a peak in 1969 and is<br />

presently, in our opinion, at a<br />

conservative leveli There are no<br />

significant near term maturities of<br />

funded debt, and with our strong<br />

financial condition we anticipate no<br />

need for any domestic long term debt<br />

or equity financing.<br />

The continuation of the government's<br />

balance of payments program<br />

requires us to raise certain funds<br />

overseas . During the year, Philip<br />

Morris sold $31 million of 15-year<br />

Deutsche Mark debentures . We<br />

would expect that other offshore<br />

term financing will'be required from<br />

time to time for as long as the balance<br />

of payments program remains in<br />

effect .<br />

Following the Smithsonian Accord<br />

iaDecember, 1971, there were no<br />

major currency realignments that<br />

affected earnings in a material<br />

manner . The net result of such<br />

realignments that did occur in 1972<br />

was reflected by an increase in the<br />

reserve applicable to international<br />

operations of$3 :8 million.<br />

During the year, the company was<br />

advised by the New York Stock<br />

Exchange that as a result of changes<br />

in its listing requirements our<br />

3 .90% Series Preferred was to be<br />

delisted. This would have resulted in<br />

further r<strong>edu</strong>cing its already limited<br />

marketability, Consequently, in<br />

December, 1972, the company<br />

offered to purchase all shares of the<br />

3490% Series Preferred for $70 per<br />

share and simultaneously offered to<br />

purchase all shares of the 4% Series<br />

Preferred at $75 per share . Upon the<br />

expiration of the offer, January 12,<br />

1973 ; 141,565 shares representing<br />

80.5% of the combined'outstandin g<br />

shares had been purchased and wil l<br />

be canceled . Subsequent to the offer,<br />

the 4% Series was also delisted .<br />

4 1<br />

..it'.'