Measuring the Effects of a Shock to Monetary Policy - Humboldt ...

Measuring the Effects of a Shock to Monetary Policy - Humboldt ...

Measuring the Effects of a Shock to Monetary Policy - Humboldt ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Bayesian FAVARs with Agnostic Identification 41<br />

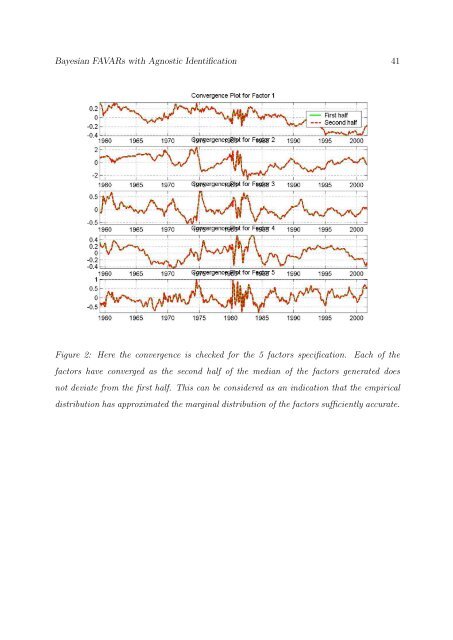

Figure 2: Here <strong>the</strong> convergence is checked for <strong>the</strong> 5 fac<strong>to</strong>rs specification. Each <strong>of</strong> <strong>the</strong><br />

fac<strong>to</strong>rs have converged as <strong>the</strong> second half <strong>of</strong> <strong>the</strong> median <strong>of</strong> <strong>the</strong> fac<strong>to</strong>rs generated does<br />

not deviate from <strong>the</strong> first half. This can be considered as an indication that <strong>the</strong> empirical<br />

distribution has approximated <strong>the</strong> marginal distribution <strong>of</strong> <strong>the</strong> fac<strong>to</strong>rs sufficiently accurate.

![[Text eingeben] [Text eingeben] Lebenslauf Anna-Maria Schneider](https://img.yumpu.com/16300391/1/184x260/text-eingeben-text-eingeben-lebenslauf-anna-maria-schneider.jpg?quality=85)