Strategic responses to Performance Measurement in Nonprofit ...

Strategic responses to Performance Measurement in Nonprofit ...

Strategic responses to Performance Measurement in Nonprofit ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

22<br />

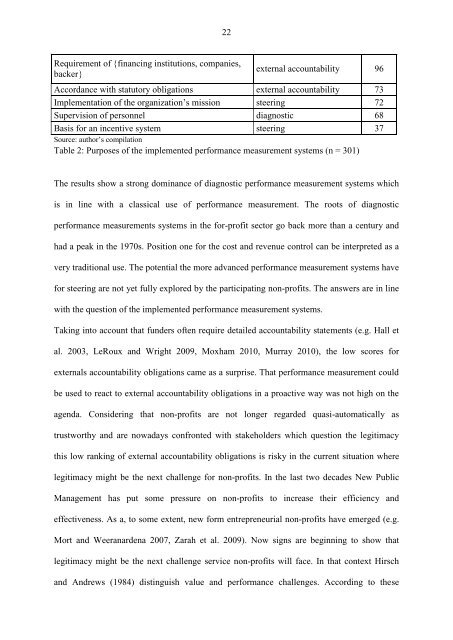

Requirement of {f<strong>in</strong>anc<strong>in</strong>g <strong>in</strong>stitutions, companies,<br />

backer}<br />

external accountability 96<br />

Accordance with statu<strong>to</strong>ry obligations external accountability 73<br />

Implementation of the organization‟s mission steer<strong>in</strong>g 72<br />

Supervision of personnel diagnostic 68<br />

Basis for an <strong>in</strong>centive system steer<strong>in</strong>g 37<br />

Source: author‟s compilation<br />

Table 2: Purposes of the implemented performance measurement systems (n = 301)<br />

The results show a strong dom<strong>in</strong>ance of diagnostic performance measurement systems which<br />

is <strong>in</strong> l<strong>in</strong>e with a classical use of performance measurement. The roots of diagnostic<br />

performance measurements systems <strong>in</strong> the for-profit sec<strong>to</strong>r go back more than a century and<br />

had a peak <strong>in</strong> the 1970s. Position one for the cost and revenue control can be <strong>in</strong>terpreted as a<br />

very traditional use. The potential the more advanced performance measurement systems have<br />

for steer<strong>in</strong>g are not yet fully explored by the participat<strong>in</strong>g non-profits. The answers are <strong>in</strong> l<strong>in</strong>e<br />

with the question of the implemented performance measurement systems.<br />

Tak<strong>in</strong>g <strong>in</strong><strong>to</strong> account that funders often require detailed accountability statements (e.g. Hall et<br />

al. 2003, LeRoux and Wright 2009, Moxham 2010, Murray 2010), the low scores for<br />

externals accountability obligations came as a surprise. That performance measurement could<br />

be used <strong>to</strong> react <strong>to</strong> external accountability obligations <strong>in</strong> a proactive way was not high on the<br />

agenda. Consider<strong>in</strong>g that non-profits are not longer regarded quasi-au<strong>to</strong>matically as<br />

trustworthy and are nowadays confronted with stakeholders which question the legitimacy<br />

this low rank<strong>in</strong>g of external accountability obligations is risky <strong>in</strong> the current situation where<br />

legitimacy might be the next challenge for non-profits. In the last two decades New Public<br />

Management has put some pressure on non-profits <strong>to</strong> <strong>in</strong>crease their efficiency and<br />

effectiveness. As a, <strong>to</strong> some extent, new form entrepreneurial non-profits have emerged (e.g.<br />

Mort and Weeranardena 2007, Zarah et al. 2009). Now signs are beg<strong>in</strong>n<strong>in</strong>g <strong>to</strong> show that<br />

legitimacy might be the next challenge service non-profits will face. In that context Hirsch<br />

and Andrews (1984) dist<strong>in</strong>guish value and performance challenges. Accord<strong>in</strong>g <strong>to</strong> these