Strategic responses to Performance Measurement in Nonprofit ...

Strategic responses to Performance Measurement in Nonprofit ...

Strategic responses to Performance Measurement in Nonprofit ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

36<br />

resource mobilisations for nonprofits, political or calculative <strong>in</strong>terests, efforts <strong>to</strong> control<br />

external criteria as well as the option of non-compliance (Oliver 1991: 147).<br />

In l<strong>in</strong>e with the above presented three options of performance measurement (external<br />

accountability, <strong>in</strong>ternal steer<strong>in</strong>g and <strong>in</strong>ternal diagnostic use) various reactions are identified<br />

for nonprofits which they can choose as a strategy <strong>to</strong>wards performance measurement. As<br />

decoupl<strong>in</strong>g plays a role with respect <strong>to</strong> the implementation of performance measurement <strong>in</strong><br />

organizations which are not driven by the profit motive (e.g. Modell 2009 for the public<br />

sec<strong>to</strong>r), also predictions are made how likely such a behaviour will be. As we have seen above<br />

that nonprofits might not adjust the performance measurement systems <strong>to</strong> the specific<br />

<strong>in</strong>stitutional orientation of the nonprofit sec<strong>to</strong>r that will also be variable <strong>to</strong> be considered with<br />

respect <strong>to</strong> the accountability motive. Another f<strong>in</strong>d<strong>in</strong>g was that one f<strong>in</strong>ds somehow partially<br />

implemented performance measurement systems. Therefore it is appropriate <strong>to</strong> take this also<br />

<strong>in</strong><strong>to</strong> account if a fully developed performance measurement system or only a rudimentary one.<br />

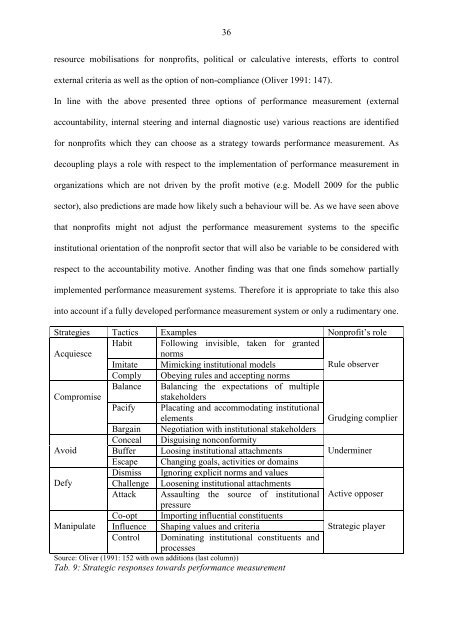

Strategies Tactics Examples <strong>Nonprofit</strong>‟s role<br />

Habit Follow<strong>in</strong>g <strong>in</strong>visible, taken for granted<br />

Acquiesce<br />

norms<br />

Imitate Mimick<strong>in</strong>g <strong>in</strong>stitutional models<br />

Rule observer<br />

Comply Obey<strong>in</strong>g rules and accept<strong>in</strong>g norms<br />

Balance Balanc<strong>in</strong>g the expectations of multiple<br />

Compromise<br />

stakeholders<br />

Pacify Placat<strong>in</strong>g and accommodat<strong>in</strong>g <strong>in</strong>stitutional<br />

elements<br />

Grudg<strong>in</strong>g complier<br />

Barga<strong>in</strong> Negotiation with <strong>in</strong>stitutional stakeholders<br />

Conceal Disguis<strong>in</strong>g nonconformity<br />

Avoid Buffer Loos<strong>in</strong>g <strong>in</strong>stitutional attachments Underm<strong>in</strong>er<br />

Escape Chang<strong>in</strong>g goals, activities or doma<strong>in</strong>s<br />

Dismiss Ignor<strong>in</strong>g explicit norms and values<br />

Defy Challenge Loosen<strong>in</strong>g <strong>in</strong>stitutional attachments<br />

Attack Assault<strong>in</strong>g the source of <strong>in</strong>stitutional<br />

pressure<br />

Active opposer<br />

Co-opt Import<strong>in</strong>g <strong>in</strong>fluential constituents<br />

Manipulate Influence Shap<strong>in</strong>g values and criteria<br />

<strong>Strategic</strong> player<br />

Control Dom<strong>in</strong>at<strong>in</strong>g <strong>in</strong>stitutional constituents and<br />

processes<br />

Source: Oliver (1991: 152 with own additions (last column))<br />

Tab. 9: <strong>Strategic</strong> <strong>responses</strong> <strong>to</strong>wards performance measurement