The Case for Emerging Market Corporates - IndexUniverse.com

The Case for Emerging Market Corporates - IndexUniverse.com

The Case for Emerging Market Corporates - IndexUniverse.com

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Over the last decade, emerging market (EM) economies<br />

have benefited greatly from macroeconomic<br />

stabilization and the liberalization of trade and<br />

financial markets. Most of these countries have enjoyed<br />

robust gross domestic product (GDP) growth both on an<br />

absolute basis and relative to more developed economies.<br />

As a result, they have experienced dramatic economic<br />

trans<strong>for</strong>mations and accelerated public sector deleveraging.<br />

Gradually, local regulators have improved bankruptcy<br />

regimes, market transparency and investor rights. This<br />

has resulted in higher levels of <strong>for</strong>eign direct investment<br />

and capital markets activity, which has greatly benefited<br />

the growth of local corporations.<br />

Given this positive macro backdrop, improved legal<br />

environment and supportive demographics, <strong>com</strong>panies<br />

from many of these EM countries have been able to<br />

increase their access to the international markets <strong>for</strong> both<br />

debt and equity, broaden their investor base and extend<br />

their maturity profiles. In several instances, EM corporates<br />

have grown into global leaders in their respective sectors.<br />

Since early 2000, EM corporate debt has evolved from<br />

a marginal market with $20 billion in annual issuance<br />

volume (mostly from Latin American issuers) to a global<br />

market with average annual issuance in excess of $100<br />

billion with representation from all four major regions<br />

(Asia, Latin America, Central and Eastern Europe, and<br />

the Middle East/Africa). 1 EM corporate fixed in<strong>com</strong>e has<br />

effectively be<strong>com</strong>e an asset class in its own right, with<br />

projections that outstanding corporate debt will exceed<br />

$1 trillion in the next several years.<br />

As valuations <strong>for</strong> EM external sovereign debt reach alltime<br />

highs, fueled by record inflows and reduced sovereign<br />

issuance, traditional EM investors are selectively increasing<br />

their allocations to EM corporate debt. Furthermore,<br />

global high-yield and investment-grade fixed-in<strong>com</strong>e<br />

investors—or “crossover” investors—are also be<strong>com</strong>ing<br />

more actively involved in the asset class. An additional catalyst<br />

to interest in the sector is the recent development of<br />

the Corporate <strong>Emerging</strong> <strong>Market</strong>s Bond Index, 2 or CEMBI,<br />

<strong>for</strong> external hard-currency debt obligations. Today there<br />

are approximately $10 billion in assets under management<br />

benchmarked against various CEMBI indexes, with expectations<br />

that this will double by the end of 2011.<br />

We believe that an allocation to EM corporate debt<br />

could be an attractive option <strong>for</strong> investors seeking an<br />

opportunity to diversify away from other traditional<br />

fixed-in<strong>com</strong>e asset classes and add potential excess riskadjusted<br />

returns. In most instances, EM corporate debt<br />

investments still offer a positive basis over both sovereign<br />

benchmark bonds and <strong>com</strong>parable developed-market<br />

high-yield and investment-grade corporate fixedin<strong>com</strong>e<br />

securities—which is particularly <strong>com</strong>pelling in<br />

the current low-interest-rate U.S. Treasury environment.<br />

When <strong>com</strong>paring potential returns—taking into account<br />

historical default levels of high-yield EM corporates versus<br />

those of U.S. high-yield indexes—the argument <strong>for</strong><br />

allocating assets to EM corporates be<strong>com</strong>es, in our view,<br />

even more <strong>com</strong>pelling.<br />

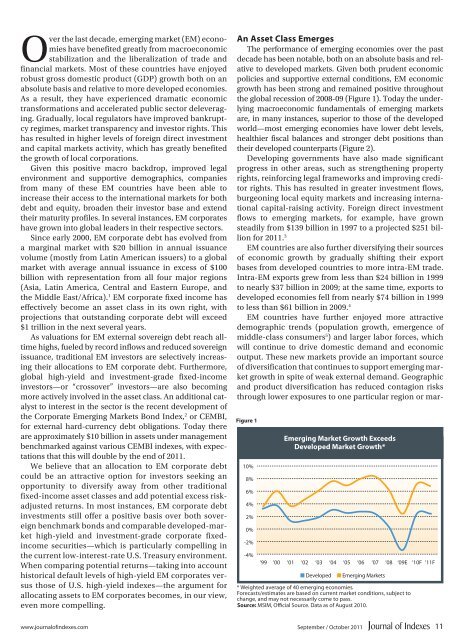

An Asset Class Emerges<br />

<strong>The</strong> per<strong>for</strong>mance of emerging economies over the past<br />

decade has been notable, both on an absolute basis and relative<br />

to developed markets. Given both prudent economic<br />

policies and supportive external conditions, EM economic<br />

growth has been strong and remained positive throughout<br />

the global recession of 2008-09 (Figure 1). Today the underlying<br />

macroeconomic fundamentals of emerging markets<br />

are, in many instances, superior to those of the developed<br />

world—most emerging economies have lower debt levels,<br />

healthier fiscal balances and stronger debt positions than<br />

their developed counterparts (Figure 2).<br />

Developing governments have also made significant<br />

progress in other areas, such as strengthening property<br />

rights, rein<strong>for</strong>cing legal frameworks and improving creditor<br />

rights. This has resulted in greater investment flows,<br />

burgeoning local equity markets and increasing international<br />

capital-raising activity. Foreign direct investment<br />

flows to emerging markets, <strong>for</strong> example, have grown<br />

steadily from $139 billion in 1997 to a projected $251 billion<br />

<strong>for</strong> 2011. 3<br />

EM countries are also further diversifying their sources<br />

of economic growth by gradually shifting their export<br />

bases from developed countries to more intra-EM trade.<br />

Intra-EM exports grew from less than $24 billion in 1999<br />

to nearly $37 billion in 2009; at the same time, exports to<br />

developed economies fell from nearly $74 billion in 1999<br />

to less than $61 billion in 2009. 4<br />

EM countries have further enjoyed more attractive<br />

demographic trends (population growth, emergence of<br />

middle-class consumers 5 ) and larger labor <strong>for</strong>ces, which<br />

will continue to drive domestic demand and economic<br />

output. <strong>The</strong>se new markets provide an important source<br />

of diversification that continues to support emerging market<br />

growth in spite of weak external demand. Geographic<br />

and product diversification has reduced contagion risks<br />

through lower exposures to one particular region or mar-<br />

Figure 1<br />

10%<br />

8%<br />

6%<br />

4%<br />

2%<br />

0%<br />

-2%<br />

-4%<br />

<strong>Emerging</strong> <strong>Market</strong> Growth Exceeds<br />

Developed <strong>Market</strong> Growth*<br />

‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09E ‘10F ‘11F<br />

N Developed<br />

N <strong>Emerging</strong> <strong>Market</strong>s<br />

* Weighted average of 40 emerging economies.<br />

Forecasts/estimates are based on current market conditions, subject to<br />

change, and may not necessarily <strong>com</strong>e to pass.<br />

Source: MSIM, Official Source. Data as of August 2010.<br />

www.journalofindexes.<strong>com</strong> September / October 2011<br />

11