Chapter 9: Introduction to Hypothesis Testing

Chapter 9: Introduction to Hypothesis Testing

Chapter 9: Introduction to Hypothesis Testing

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

382 CHAPTER 9 • INTRODUCTION TO HYPOTHESIS TESTING<br />

Critical Value<br />

The value corresponding <strong>to</strong> a<br />

significance level that determines<br />

those test statistics that lead <strong>to</strong><br />

rejecting the null hypothesis and<br />

those that lead <strong>to</strong> a decision not <strong>to</strong><br />

reject the null hypothesis.<br />

CHAPTER OUTCOME #4<br />

Business<br />

Application<br />

The decision maker carrying out the test specifies the significance level, . The value<br />

of is determined based on the costs involved in committing a Type I error. If making a<br />

Type I error is costly, we will want the probability of a Type I error <strong>to</strong> be small. If a Type I<br />

error is less costly, then we can allow a higher probability of a Type I error.<br />

However, in determining , we must also take in<strong>to</strong> account the probability of making<br />

a Type II error, which is given the symbol (beta). The two error probabilities, and ,<br />

are inversely related. 2 That is, if we reduce , then will increase. Thus, in setting , you<br />

must consider both sides of the issue.<br />

Calculating the specific dollar costs associated with making Type I and Type II errors<br />

is often difficult and may require a subjective management decision. Therefore, any two<br />

managers might well arrive at different alpha levels. However, in the end, the choice for<br />

alpha must reflect the decision maker’s best estimate of the costs of these two errors. 3<br />

Having chosen a significance level , the decision maker then must calculate the<br />

corresponding cu<strong>to</strong>ff point, which is called a critical value.<br />

<strong>Hypothesis</strong> Test for , Known<br />

Calculating Critical Values To calculate critical values corresponding <strong>to</strong> a chosen , we<br />

need <strong>to</strong> know the sampling distribution of the sample mean x. If our sampling conditions<br />

satisfy the Central Limit Theorem requirements or if the population is normally distributed<br />

and we know the population standard deviation , then the sampling distribution of x is<br />

normal with mean equal <strong>to</strong> the population mean μ and standard deviation / n. 4 With this<br />

information we can calculate a critical z-value, called z <br />

, or a critical x-value, called x .<br />

We illustrate both calculations in the Morgan Lane Real Estate example.<br />

MORGAN LANE REAL ESTATE (CONTINUED) Suppose the managing partners decide they<br />

are willing <strong>to</strong> incur a 0.10 probability of committing a Type I error. Assume also that the<br />

population standard deviation, , for closing is 3 days and the sample size is 64 homes.<br />

Given that the sample size is large (n 30) and that the population standard deviation is<br />

known (3 days), we can state the critical value in two ways. First, we can establish the<br />

critical value as a z-value.<br />

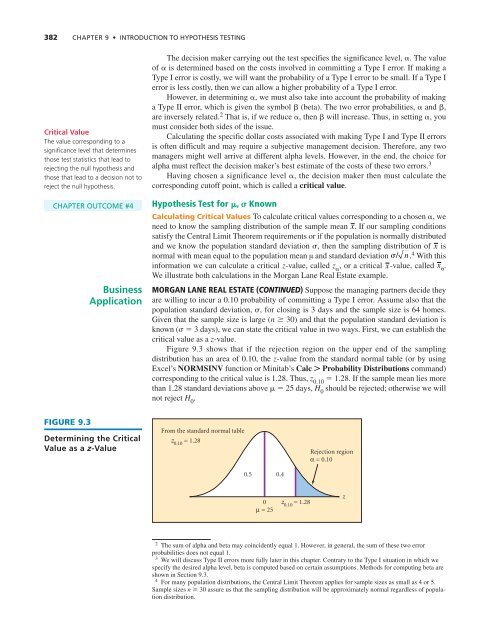

Figure 9.3 shows that if the rejection region on the upper end of the sampling<br />

distribution has an area of 0.10, the z-value from the standard normal table (or by using<br />

Excel’s NORMSINV function or Minitab’s Calc Probability Distributions command)<br />

corresponding <strong>to</strong> the critical value is 1.28. Thus, z 0.10<br />

1.28. If the sample mean lies more<br />

than 1.28 standard deviations above 25 days, H 0<br />

should be rejected; otherwise we will<br />

not reject H 0<br />

.<br />

FIGURE 9.3<br />

Determining the Critical<br />

Value as a z-Value<br />

From the standard normal table<br />

z 0.10 = 1.28<br />

0.5 0.4<br />

Rejection region<br />

α = 0.10<br />

0<br />

μ = 25<br />

z 0.10 = 1.28<br />

z<br />

2 The sum of alpha and beta may coincidently equal 1. However, in general, the sum of these two error<br />

probabilities does not equal 1.<br />

3 We will discuss Type II errors more fully later in this chapter. Contrary <strong>to</strong> the Type I situation in which we<br />

specify the desired alpha level, beta is computed based on certain assumptions. Methods for computing beta are<br />

shown in Section 9.3.<br />

4 For many population distributions, the Central Limit Theorem applies for sample sizes as small as 4 or 5.<br />

Sample sizes n 30 assure us that the sampling distribution will be approximately normal regardless of population<br />

distribution.