Dataline A look at current financial reporting issues - PwC

Dataline A look at current financial reporting issues - PwC

Dataline A look at current financial reporting issues - PwC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

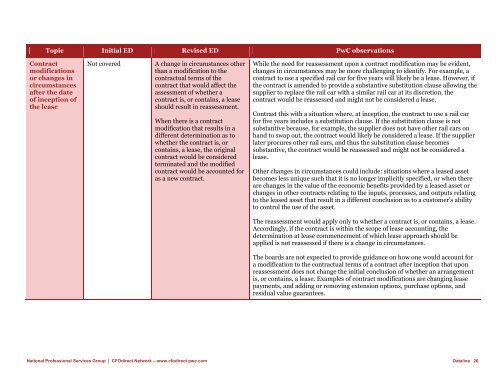

Topic Initial ED Revised ED <strong>PwC</strong> observ<strong>at</strong>ions<br />

Contract<br />

modific<strong>at</strong>ions<br />

or changes in<br />

circumstances<br />

after the d<strong>at</strong>e<br />

of inception of<br />

the lease<br />

Not covered<br />

A change in circumstances other<br />

than a modific<strong>at</strong>ion to the<br />

contractual terms of the<br />

contract th<strong>at</strong> would affect the<br />

assessment of whether a<br />

contract is, or contains, a lease<br />

should result in reassessment.<br />

When there is a contract<br />

modific<strong>at</strong>ion th<strong>at</strong> results in a<br />

different determin<strong>at</strong>ion as to<br />

whether the contract is, or<br />

contains, a lease, the original<br />

contract would be considered<br />

termin<strong>at</strong>ed and the modified<br />

contract would be accounted for<br />

as a new contract.<br />

While the need for reassessment upon a contract modific<strong>at</strong>ion may be evident,<br />

changes in circumstances may be more challenging to identify. For example, a<br />

contract to use a specified rail car for five years will likely be a lease. However, if<br />

the contract is amended to provide a substantive substitution clause allowing the<br />

supplier to replace the rail car with a similar rail car <strong>at</strong> its discretion, the<br />

contract would be reassessed and might not be considered a lease.<br />

Contrast this with a situ<strong>at</strong>ion where, <strong>at</strong> inception, the contract to use a rail car<br />

for five years includes a substitution clause. If the substitution clause is not<br />

substantive because, for example, the supplier does not have other rail cars on<br />

hand to swap out, the contract would likely be considered a lease. If the supplier<br />

l<strong>at</strong>er procures other rail cars, and thus the substitution clause becomes<br />

substantive, the contract would be reassessed and might not be considered a<br />

lease.<br />

Other changes in circumstances could include: situ<strong>at</strong>ions where a leased asset<br />

becomes less unique such th<strong>at</strong> it is no longer implicitly specified, or when there<br />

are changes in the value of the economic benefits provided by a leased asset or<br />

changes in other contracts rel<strong>at</strong>ing to the inputs, processes, and outputs rel<strong>at</strong>ing<br />

to the leased asset th<strong>at</strong> result in a different conclusion as to a customer's ability<br />

to control the use of the asset.<br />

The reassessment would apply only to whether a contract is, or contains, a lease.<br />

Accordingly, if the contract is within the scope of lease accounting, the<br />

determin<strong>at</strong>ion <strong>at</strong> lease commencement of which lease approach should be<br />

applied is not reassessed if there is a change in circumstances.<br />

The boards are not expected to provide guidance on how one would account for<br />

a modific<strong>at</strong>ion to the contractual terms of a contract after inception th<strong>at</strong> upon<br />

reassessment does not change the initial conclusion of whether an arrangement<br />

is, or contains, a lease. Examples of contract modific<strong>at</strong>ions are changing lease<br />

payments, and adding or removing extension options, purchase options, and<br />

residual value guarantees.<br />

N<strong>at</strong>ional Professional Services Group | CFOdirect Network – www.cfodirect.pwc.com <strong>D<strong>at</strong>aline</strong> 26