HII Ingalls Shipbuilding Inc. Hourly Employees ... - Benefits Connect

HII Ingalls Shipbuilding Inc. Hourly Employees ... - Benefits Connect

HII Ingalls Shipbuilding Inc. Hourly Employees ... - Benefits Connect

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>HII</strong> <strong>Ingalls</strong> <strong>Shipbuilding</strong> <strong>Inc</strong>. <strong>Hourly</strong> <strong>Employees</strong>’ Retirement Plan<br />

Summary Plan Description<br />

March 2011<br />

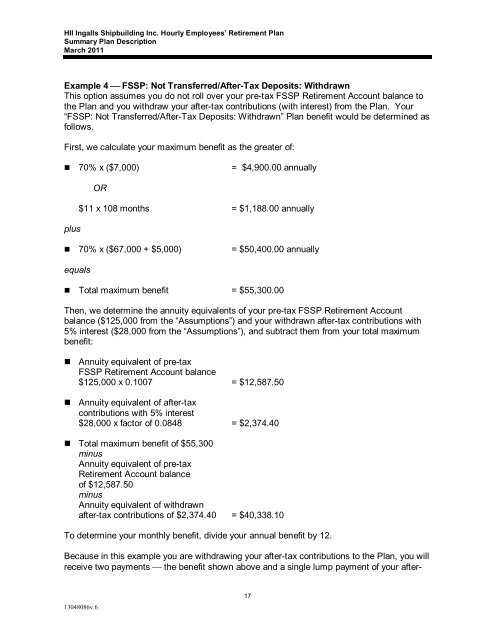

Example 4 ⎯ FSSP: Not Transferred/After-Tax Deposits: Withdrawn<br />

This option assumes you do not roll over your pre-tax FSSP Retirement Account balance to<br />

the Plan and you withdraw your after-tax contributions (with interest) from the Plan. Your<br />

“FSSP: Not Transferred/After-Tax Deposits: Withdrawn” Plan benefit would be determined as<br />

follows.<br />

First, we calculate your maximum benefit as the greater of:<br />

• 70% x ($7,000) = $4,900.00 annually<br />

plus<br />

OR<br />

$11 x 108 months = $1,188.00 annually<br />

• 70% x ($67,000 + $5,000) = $50,400.00 annually<br />

equals<br />

• Total maximum benefit = $55,300.00<br />

Then, we determine the annuity equivalents of your pre-tax FSSP Retirement Account<br />

balance ($125,000 from the “Assumptions”) and your withdrawn after-tax contributions with<br />

5% interest ($28,000 from the “Assumptions”), and subtract them from your total maximum<br />

benefit:<br />

• Annuity equivalent of pre-tax<br />

FSSP Retirement Account balance<br />

$125,000 x 0.1007 = $12,587.50<br />

• Annuity equivalent of after-tax<br />

contributions with 5% interest<br />

$28,000 x factor of 0.0848 = $2,374.40<br />

• Total maximum benefit of $55,300<br />

minus<br />

Annuity equivalent of pre-tax<br />

Retirement Account balance<br />

of $12,587.50<br />

minus<br />

Annuity equivalent of withdrawn<br />

after-tax contributions of $2,374.40 = $40,338.10<br />

To determine your monthly benefit, divide your annual benefit by 12.<br />

Because in this example you are withdrawing your after-tax contributions to the Plan, you will<br />

receive two payments ⎯ the benefit shown above and a single lump payment of your after-<br />

13048086v.6<br />

17